What every founder needs to understand about AI economics? | What’s driving the surprising decline in founder dilution?

Does Anthropic winning enterprise race? & LPs fighting for access to co-investment in the most valuable AI deals.

The AI Strategy Summit 2026 – June 4 | Free Virtual Event

On June 4, from 12 - 4 PM ET, join Scott Galloway and Section to learn everything you need to scale from individual productivity gains to enterprise-wide AI orchestration.

Join 6 AI leaders from the enterprise for an afternoon of strategy sharing to gain the tactics for scaling siloed AI use into organisation-wide impact. You’ll walk away with the playbook to turn data, processes, and people into connected, augmented, AI powerhouses.

👋 Hey, here’s today at a glance -

Big idea + report of the week :

Why are LPs fighting for access to the most valuable AI deals?

Did OpenAI win attention while Anthropic built a better company?

Frameworks & insightful posts :

What every founder needs to understand about AI economics?

Where AI seed investors are most likely to find outliers.

What’s driving the surprising decline in founder dilution?

START WITH

🧠 Big idea + report of the week

Why are LPs fighting for access to the most valuable AI deals?

For years, co-investments were treated as a useful side benefit of backing top venture funds.

Today, they have become one of the most important battlegrounds in private markets.

A recent PitchBook analysis by Jessica Hamlin explains why. As companies like OpenAI, Anthropic, and xAI race toward valuations that could eventually justify trillion-dollar outcomes, limited partners are fighting aggressively for direct exposure alongside their GPs.

The logic is simple: if a handful of frontier AI companies end up becoming the defining businesses of this decade, even a relatively small ownership stake could materially improve an LP’s overall portfolio returns.

That possibility is creating a new divide between institutions with the relationships, resources, and underwriting capabilities to access these deals and those that do not.

The biggest AI companies are attracting unprecedented amounts of capital

The scale of valuation growth in late-stage AI is unlike anything venture investors have seen in recent memory.

According to PitchBook, U.S.-based AI and machine learning startups raising Series D rounds and beyond reached a median pre-money valuation of $4.7 billion in Q1 2026. That is nearly four times higher than comparable non-AI companies and represents a 447.8% increase from 2024.

These numbers explain why LPs are so eager to participate.

If companies like Anthropic and OpenAI eventually grow into multi-trillion-dollar public businesses, direct co-investments made today could become some of the highest-returning allocations in an institution’s portfolio.

The market has shifted from capital scarcity to access scarcity

One of the most interesting insights in the report is how quickly the fundraising environment has changed. In early 2024, startups were competing intensely for capital. By 2026, the opposite is true.

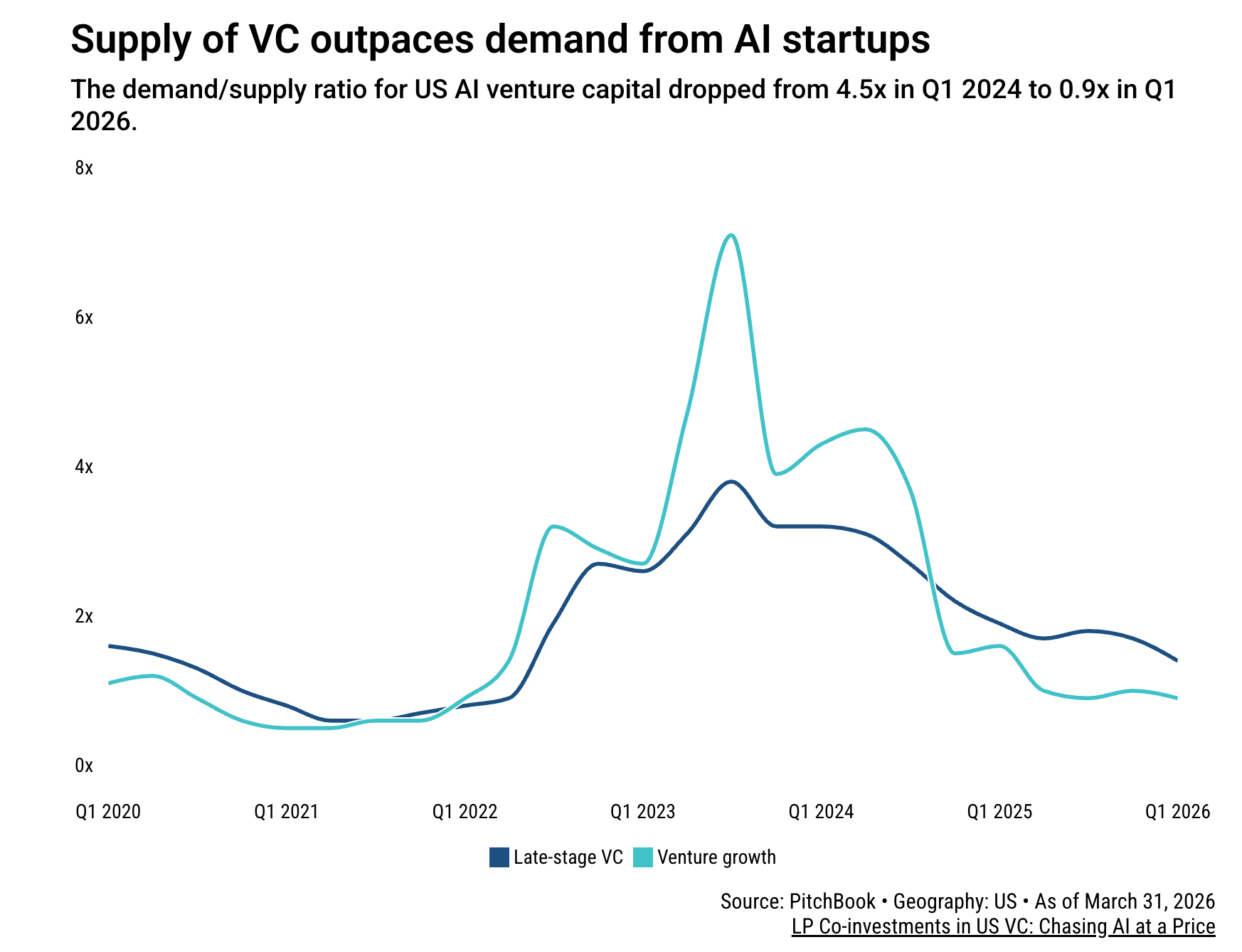

PitchBook’s data shows that the demand-to-supply ratio for U.S. AI venture capital fell from 4.5x in Q1 2024 to just 0.9x in Q1 2026.

In practical terms, investors now have more money available than high-quality AI startups need to raise. That means the challenge is no longer finding capital.

The challenge is gaining access to the very small number of companies attracting extraordinary investor interest.

Fundraising cycles are accelerating

AI companies are also raising capital at a much faster pace than traditional startups. The median time between rounds for AI startups fell to 1.3 years in Q1 2026, compared with 1.9 years for non-AI companies.

This compressed timeline favors LPs with sophisticated co-investment programs that can evaluate opportunities quickly and commit large amounts of capital on short notice.

For smaller institutions, this creates a structural disadvantage.

Without dedicated internal teams and strong GP relationships, it becomes much harder to participate in the most competitive transactions.

Why co-investments matter so much

Co-investments are particularly attractive because they often come with little or no additional management fees and carried interest.

That allows LPs to increase exposure to their highest-conviction opportunities while reducing the overall fee burden on their portfolios.

A survey from Coller Capital found that:

44% of LPs said co-investments are becoming more important in their private markets strategy.

Nearly 20% said they still do not have access to attractive opportunities.

In a market where a small number of AI companies may drive outsized returns, access to co-investments is increasingly becoming a competitive necessity rather than a nice-to-have.

The largest institutions are already positioned

Many of the world’s most sophisticated allocators have moved aggressively to secure exposure.

Examples include:

Qatar Investment Authority participating in xAI’s $20 billion financing.

GIC helping lead Anthropic’s $30 billion round.

UC Investments joining OpenAI’s $122 billion financing.

UC Investments is particularly notable. Over the past decade, it reduced its manager relationships from 280 to just 28, reflecting a deliberate strategy of concentrating capital and increasing direct investment activity.

So - the AI boom is reshaping how LPs think about portfolio construction.

Historically, superior returns came primarily from selecting the right venture managers.

Increasingly, the greatest source of alpha may come from gaining direct exposure to the small number of companies building the foundational infrastructure of the AI economy.

That is why competition for OpenAI and Anthropic allocations has become so intense.

If these companies ultimately fulfill their potential, access to a single co-investment could meaningfully influence an institution’s long-term returns.

And for LPs without the necessary relationships and internal capabilities, the most important investment opportunity of the decade may remain frustratingly out of reach.

Did OpenAI win attention while Anthropic built a better company?

For most people, OpenAI still feels like the default winner of the AI era. It has the consumer brand, ChatGPT, massive usage, and the kind of mindshare very few startups ever reach.

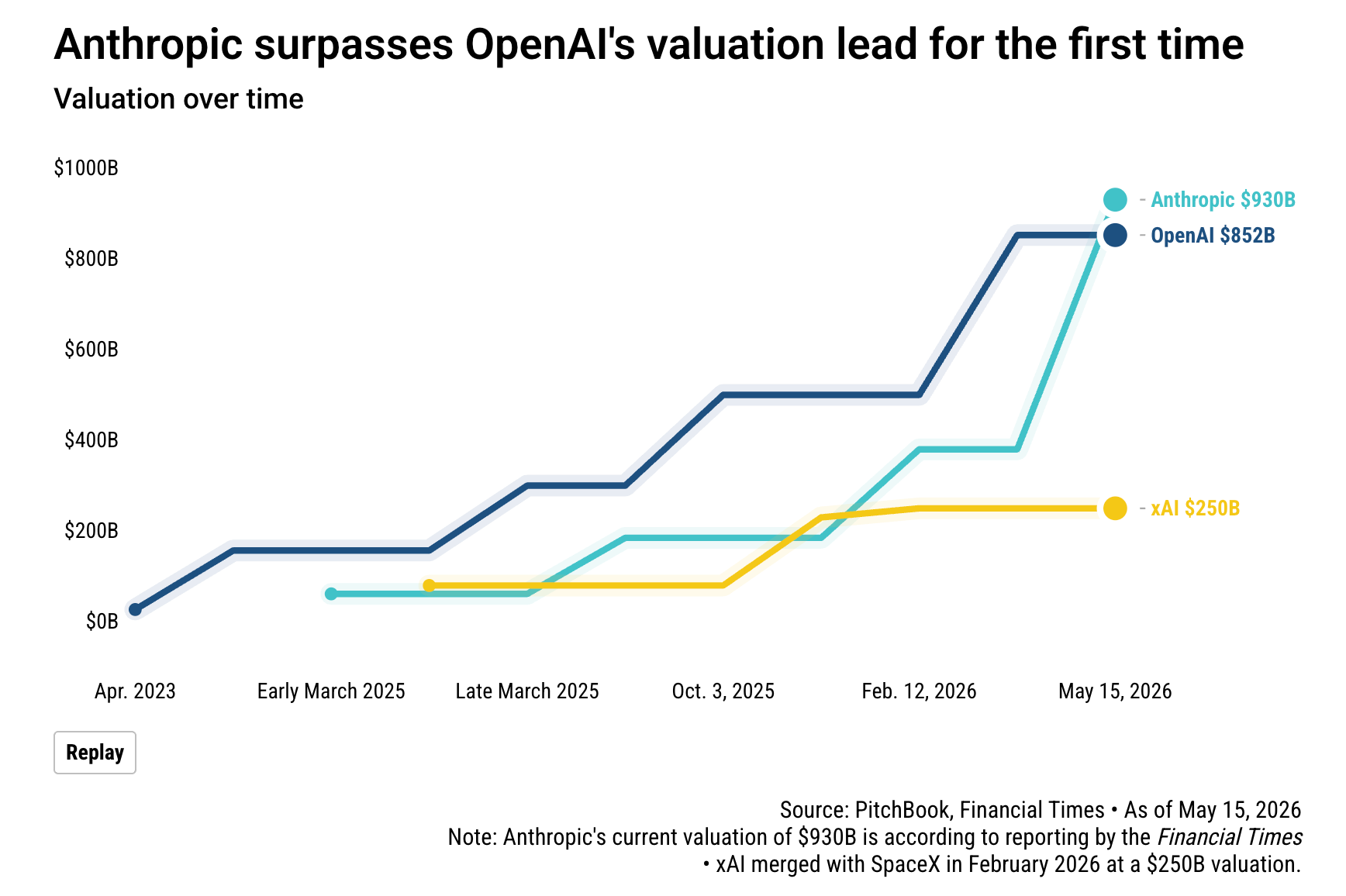

But new PitchBook and Financial Times reporting shows the race is no longer that simple. Anthropic has reportedly signed a term sheet that would value it at $930B, ahead of OpenAI’s $852B valuation for the first time.

The bigger story is not just the valuation flip. It is what investors are choosing to reward.

OpenAI still has unmatched consumer reach, with reported weekly active users near 900M. But much of that usage remains free. Anthropic, on the other hand, is gaining ground inside enterprises, where contracts are stickier and margins matter more.

Ramp’s AI Index showed 34.4% of U.S. businesses using Anthropic versus 32.3% using OpenAI, a major shift from a year ago when Anthropic was below 10%.

That enterprise momentum is why investors may be underwriting Anthropic differently.

Claude Code has helped pull developers into workflows that can expand into broader company-wide contracts. If those accounts retain and expand, Anthropic starts to look less like a chatbot company and more like a high-quality enterprise software platform.

There’s also a capital efficiency angle. PitchBook notes that Anthropic’s expected $930B valuation comes on roughly $103B of equity raised, compared with OpenAI reaching $852B on about $173B.

That implies investors are paying more per equity dollar deployed into Anthropic, because they believe the path to public-market quality may be cleaner.

A few things seem to be driving that confidence:

Strong enterprise adoption

Reported gross margins above 70%

Less dependence on a single strategic partner

Cleaner corporate structure compared with OpenAI

Developer-led adoption through Claude Code

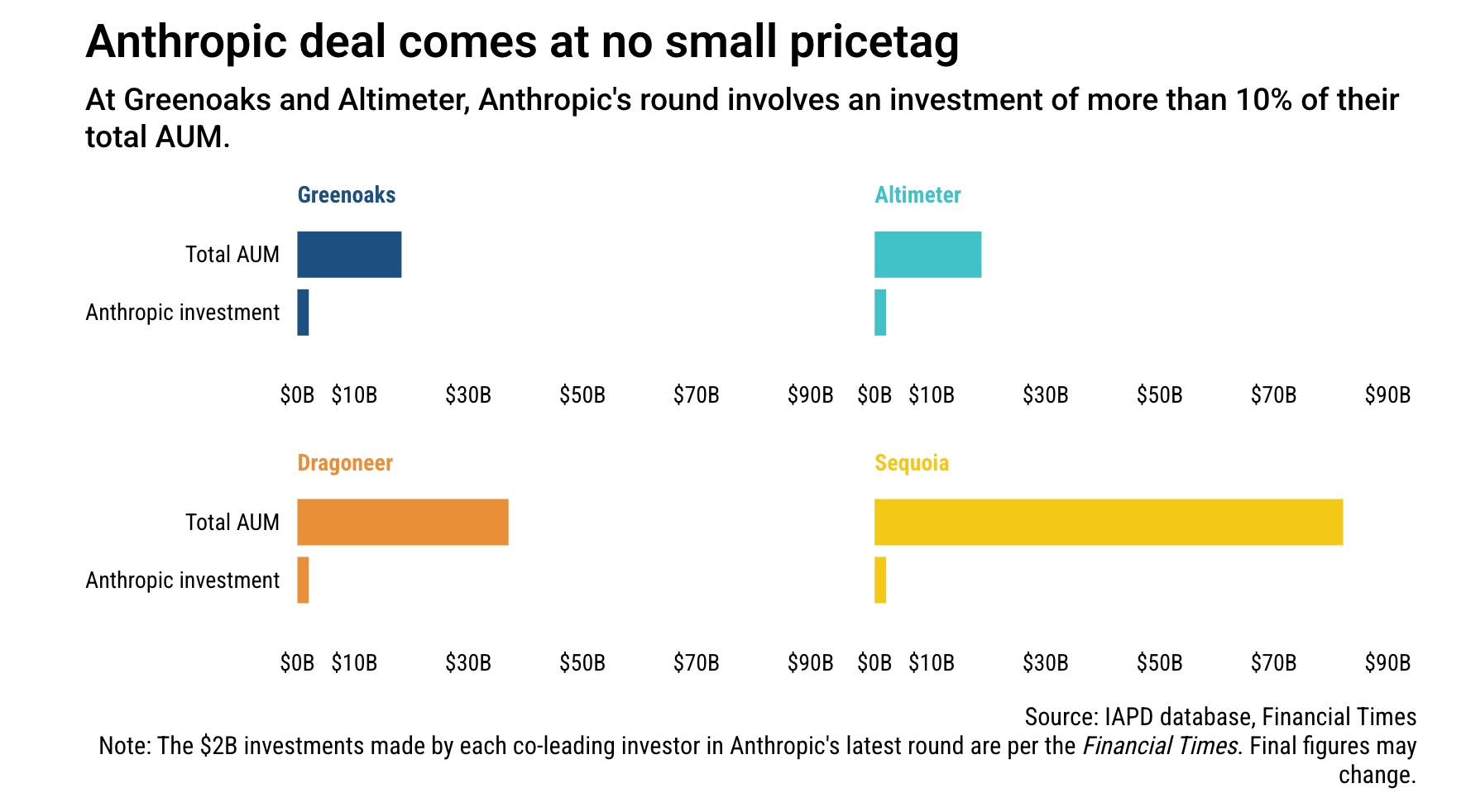

The round itself also shows how concentrated late-stage AI investing has become. Greenoaks, Altimeter, Dragoneer, and Sequoia are reportedly leading the deal, each expected to commit at least $2B.

For Greenoaks and Altimeter, that would represent more than 10% of their AUM - a huge concentration bet even by growth-stage standards.

This is where the story gets bigger than Anthropic vs. OpenAI.

The AI frontier labs are now being valued like future public-market anchors. Whoever goes public first at a higher multiple could set the benchmark for the entire category.

That will influence how investors price model labs, AI infrastructure, enterprise copilots, and every company claiming to sit near the AI value chain.

For founders: attention is not the same as enterprise value. OpenAI won the first wave of consumer mindshare, but Anthropic is showing that enterprise adoption, margins, retention, and governance can matter just as much - maybe more when investors start thinking about IPO readiness.

The AI race is no longer just about who has the most users. It is about who can become the highest-quality business.

🤝 PARTNERSHIP WITH US

Get your product in front of over 120,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

SOMETHING MORE

🧩 Frameworks & insightful posts

What every founder needs to understand about AI economics?

For the past two decades, software has been one of the best businesses in the world.

Once you built the product, the cost of serving each additional customer was tiny. That’s what made SaaS so attractive. Companies could spend heavily upfront on engineering and go-to-market, then enjoy exceptionally high margins as they scale.

Domen Jemec recently shared an analysis explaining why AI may fundamentally change this equation.

His core argument is: AI makes software cheaper to build, but potentially much more expensive to operate.

That distinction matters more than most founders realise.

Why traditional SaaS became such a powerful business model

In classic SaaS, most of the cost is fixed.

You invest millions of dollars building the product, hiring engineers, and acquiring initial customers. But once the software is live, each additional user costs very little to support.

That creates a beautiful economic model:

Revenue grows linearly as customers increase

Cost per user declines over time

Gross margins often exceed 70–80%

Mature companies can reach 20–30% net margins

This dynamic is what made strategies like blitzscaling possible.

A company could lose money early, knowing that each new customer would become increasingly profitable as scale improved.

AI flips the cost structure

AI changes this because every meaningful interaction carries a real variable cost. Each prompt, agent workflow, reasoning step, and API call consumes tokens and infrastructure.

Unlike traditional software, where features become cheaper per user over time, AI-heavy features often remain usage-based and personalised.

That means costs scale much more directly with customer activity. In practical terms:

More users generate more inference costs

More complex workflows consume more tokens

Personalised outputs reduce caching opportunities

Heavy users can materially impact margins

The result is that software begins to look less like pure SaaS and more like a hybrid of software and services.

A simple way to think about it

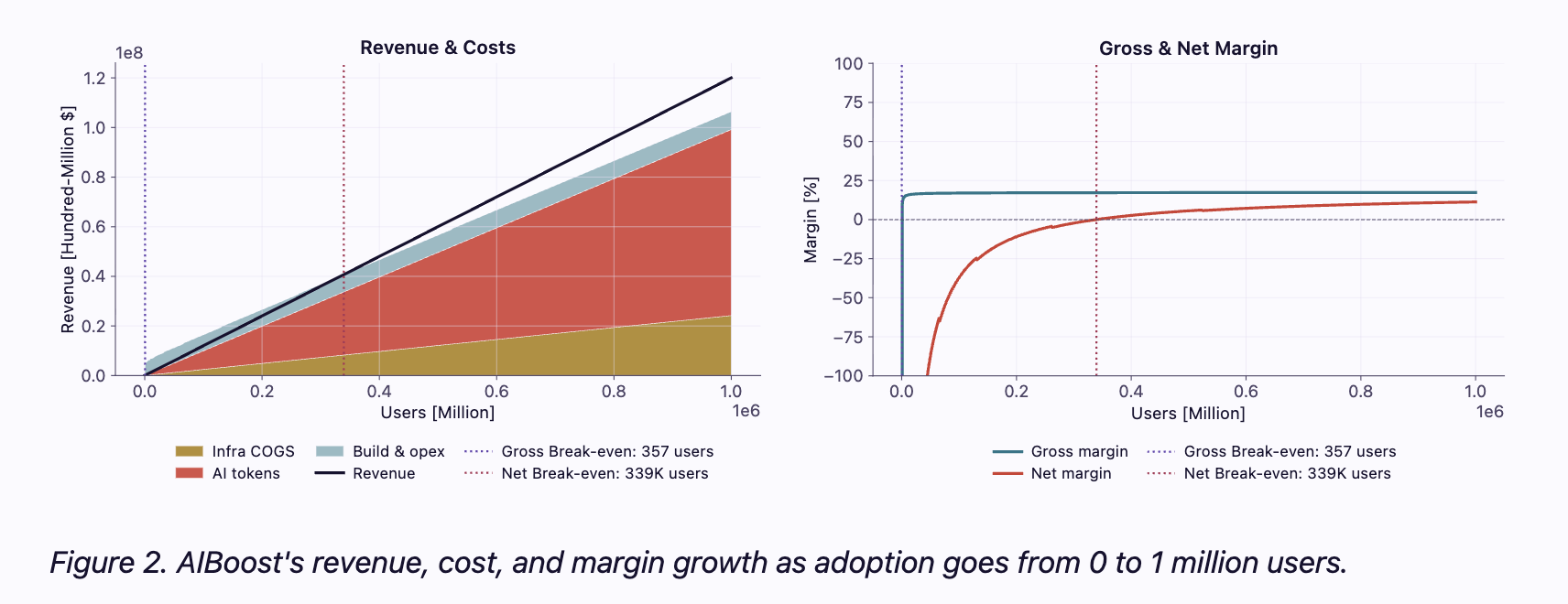

Imagine two companies that both charge $10 per user per month.

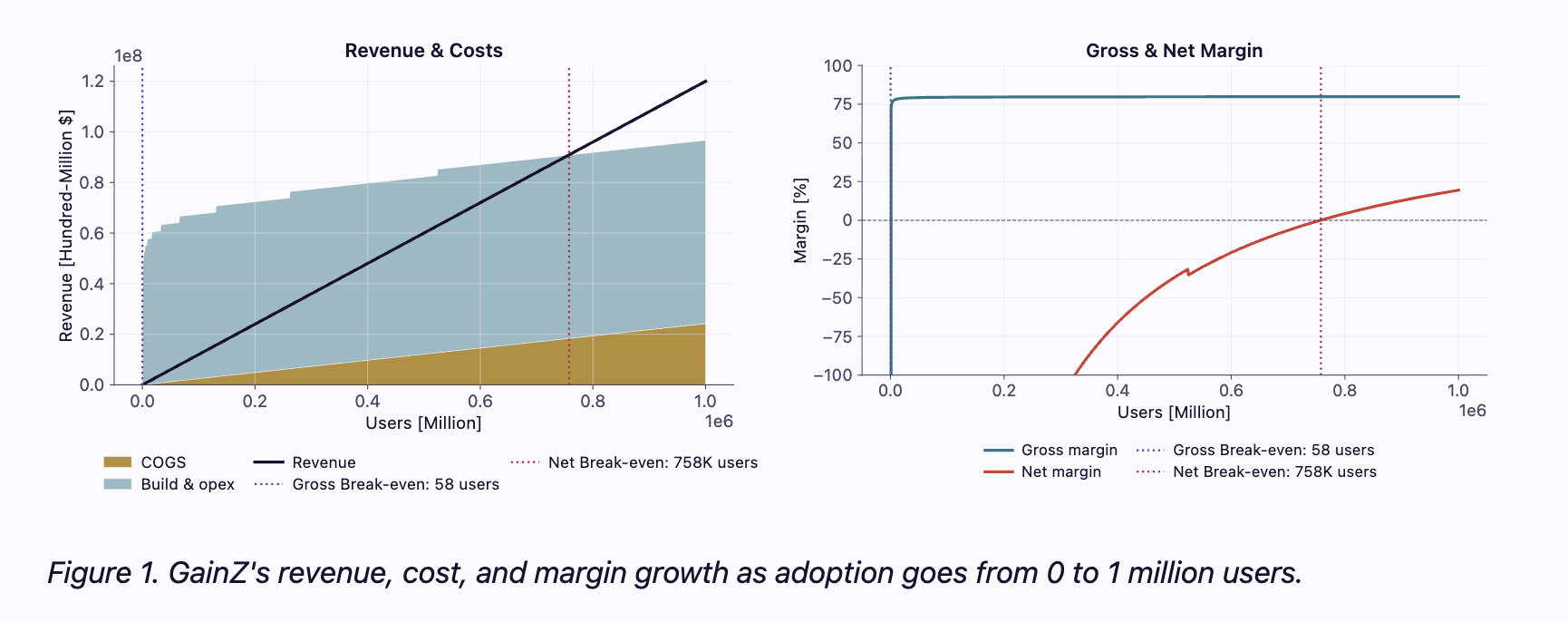

The first is a traditional SaaS company named, GainZ.

It spends heavily upfront to build the product, but by the time it reaches scale, gross margins stabilise around 80%. At 1 million users, net margins can approach 20%.

The second is an AI-native company named AIBoosts.

It may cost far less to build because a smaller team can move faster with AI tools. But every user interaction incurs ongoing inference costs.

The company becomes profitable earlier because development costs are lower, yet long-term margins remain significantly lower because AI costs continue to grow with usage.

In Domen’s example, an AI-heavy product reaches only about 11% net margin at 1 million users, versus roughly 19% for traditional SaaS.

That difference has major implications for valuation and strategy.

The hidden shift founders need to understand

Many founders focus on how AI reduces engineering costs. That is real and important. Small teams can now build products that once required dozens of engineers.

But lower build costs do not automatically translate into better businesses.

In many cases, the true constraint moves from development cost to operating cost.

The new question becomes: Can you monetise the value of AI faster than your inference costs grow?

That is the central challenge of AI-native software.

Why this matters for valuations

Software historically commanded premium valuations because investors believed margins would expand dramatically over time. If AI compresses those margins, valuation frameworks may evolve as well.

Companies with structurally lower gross margins may be valued more like operational businesses than pure software companies. This does not make them unattractive.

It simply means investors will place greater emphasis on:

Pricing power

Proprietary data

Distribution advantages

Brand trust

Operational efficiency

The best AI companies will still be extremely valuable, but the economics may look different from the SaaS playbook of the last decade.

How founders can respond

There are several ways to build durable AI businesses despite lower margins.

Align pricing with usage. If costs scale with activity, pricing should reflect that reality through tiers, overages, or premium plans.

Focus on high-value workflows. AI works best when it solves problems customers are willing to pay significantly more to address.

Build defensible moats. Proprietary data, network effects, and workflow integration matter more than ever.

Expand beyond software. Many of the strongest businesses will bundle software with services, compliance, operations, or real-world execution.

The emerging opportunities

Domen highlights several categories that become especially interesting in this new environment:

Ultra-niche products that were previously too small to justify development costs

Lower-cost challengers to established SaaS incumbents

“Luxury software” with strong brand positioning and premium pricing

Vertical businesses that combine software with real-world services

One of the most compelling implications is that smaller teams can now build profitable lifestyle businesses serving specialised markets that were once uneconomical.

So - AI is lowering the cost to create software, but it is also reshaping the economics of delivering it.

For years, software enjoyed a rare combination of high gross margins and near-zero marginal costs. That assumption no longer holds for many AI-native products.

The winners of the next decade will not simply build impressive AI features.

They will understand how those features affect the P&L, design pricing around real usage, and build businesses that remain profitable as inference becomes a core operating cost.

In other words: The future of software belongs not just to teams that ship AI fastest, but to those that understand the economics deeply enough to scale it sustainably.

Where AI seed investors are most likely to find outliers.

Every AI cycle produces noise. What matters is where outcomes compound, not just where capital is flowing. A recent PitchBook analysis looked at AI subsectors through one narrow but revealing lens: IPO exit predictor scores, a signal for where venture-scale outcomes are statistically more likely.

A few patterns stand out.

First, agentic commerce infrastructure is quietly emerging as the strongest outlier candidate.

Commerce has historically been the on-ramp for every major platform shift, internet, mobile, cloud, and AI are following the same script. What changes this time is autonomy.

Payments, identity, fraud, loyalty, and inventory systems are being rebuilt so software can transact without humans in the loop. That makes the infrastructure layer, not consumer apps, the long-term value capture point.

Second, AI-driven drug discovery is moving from promise to economic inevitability.

As AI improves trial design and success rates, the bottleneck shifts downstream. More trials mean more demand for tooling, data infrastructure, and clinical operations software.

Analysts expect this to expand the total addressable market aggressively through the decade, not because drugs get cheaper, but because more drugs actually make it to market.

Third, AI protection and defence-adjacent systems are benefiting from a similar dynamic: Autonomy replaces humans in high-stakes environments.

Edge computing and real-time decisioning are enabling faster response systems, whether in cybersecurity or physical defence.

The complexity here is not a bug; it’s the moat.

Finally, autonomous drones and swarms represent a classic early-cycle opportunity.

Fully coordinated land, sea, and air swarms are still hard to execute, but that difficulty creates asymmetry. As AI-first players replace human-piloted systems, legacy hardware and sensor providers face margin and relevance pressure.

Taken together, the signal is consistent:

Outlier returns are clustering below the application layer

Infrastructure that enables autonomy, not just intelligence, is where durability lives

Complexity and regulation are acting as filters, not deterrents

For seed investors, the takeaway isn’t to chase what’s loud. It’s to focus on where AI changes system behaviour, not just user experience. That’s where platform-scale outcomes tend to form.

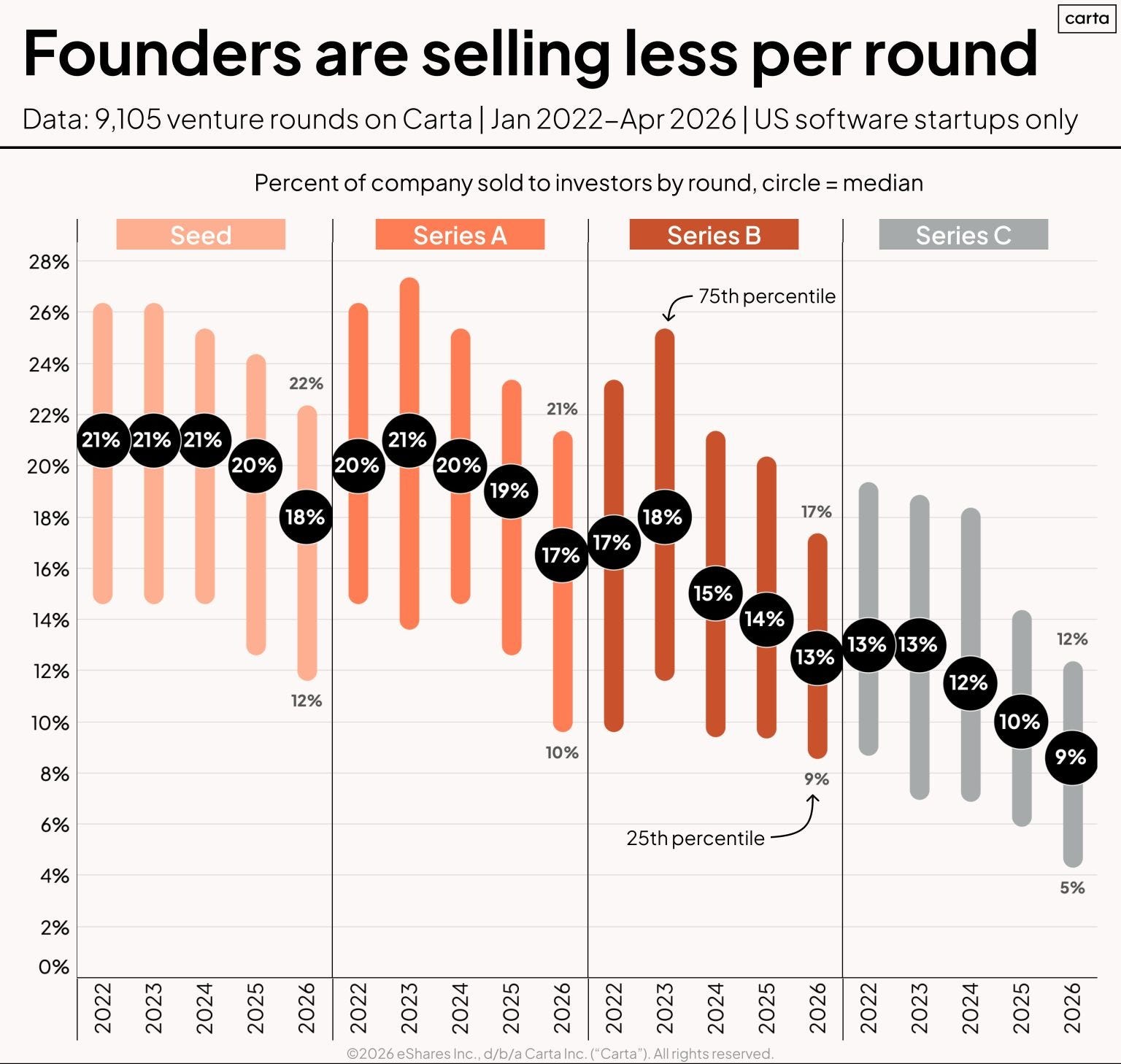

What’s driving the surprising decline in founder dilution?

One of the most interesting trends in venture right now is hiding behind a simple chart from Carta. Despite all the headlines about startups raising massive rounds, founders are actually giving up less equity than they did a few years ago.

Peter Walker, Head of Insights at Carta, recently shared data from more than 9,000 U.S. software financing rounds, and the numbers tell a fascinating story.

In 2022, the median seed round required founders to sell about 21% of their company. In 2026, that figure has dropped to 18%. The same trend is visible across every stage:

Series A dilution fell from 20% to 17%

Series B dilution declined from 17–18% to 13%

Series C dilution dropped from 13% to 9%

At first glance, this seems counterintuitive. Round sizes are getting larger, especially in AI. Yet founders are keeping more ownership.

So what’s going on?

The fundraising bar has gone up

The most obvious explanation is that fundraising has become much harder.

While social media is filled with announcements of startups raising $40 million or $100 million rounds, those stories represent a very small subset of companies.

Behind the scenes, venture firms are more selective than they have been in years. That means only a small percentage of startups are able to raise institutional capital. But the ones that do often have much stronger leverage.

They may have:

Exceptional growth

Breakthrough AI products

Strong revenue traction

Elite founding teams

Multiple term sheets competing for allocation

When investors compete aggressively for a company, valuations rise faster than the amount of money being raised. As a result, founders can raise larger rounds while selling fewer shares.

Venture is becoming more concentrated

This trend reflects a broader shift in venture capital. Investors are increasingly concentrating capital into fewer companies that appear capable of becoming category leaders.

Instead of spreading bets across hundreds of “good” startups, firms are doubling down on a smaller set of “must-own” opportunities.

This creates a barbell dynamic.

At one end are startups that struggle to raise at all. At the other end are standout companies that command premium valuations and highly founder-friendly terms.

There is less middle ground than before.

Founders are staying private longer

Another reason dilution is declining is that companies are spending more years as private businesses.

A startup may now raise Seed, Series A, B, C, D, E, and sometimes even F or G before going public. If founders sell too much equity in the early rounds, they risk becoming overly diluted long before reaching scale.

The market has adapted accordingly.

Early rounds now leave more ownership on the cap table so founders and employees still have meaningful stakes after multiple financings.

This is one of the most practical lessons for founders: financing decisions today need to account not just for the next 12 months, but for the entire multi-stage journey ahead.

Bigger rounds no longer mean bigger dilution

Traditionally, raising more capital meant giving up more of the company. That relationship is weakening.

Today, the best startups can raise substantial amounts of capital while preserving ownership because investors are underwriting future potential more aggressively than ever.

In other words, valuation growth is outpacing check size growth.

That is especially true in sectors like AI, where investors believe a small number of companies could become extremely valuable.

What this means for founders

The decline in dilution is encouraging, but it should not become an obsession.

Ownership matters. But survival matters more.

A founder who preserves two extra percentage points of equity but runs out of cash gains nothing.

The better approach is to optimize for three things:

Enough capital to reach the next major milestone

Reasonable dilution

Flexibility for future rounds

The strongest founders think in terms of long-term ownership, not just the immediate financing event.

So - the fundraising environment is harder than ever, but for exceptional companies, it is arguably better than ever.

Capital is becoming more selective, more concentrated, and more conviction-driven.

If your company demonstrates real traction and strategic importance, investors may be willing to pay dramatically higher prices to participate.

And when that happens, founders retain more ownership while accessing more capital.

That is an incredibly powerful combination.

The venture market may feel tougher on the surface, but the underlying message is optimistic: The best companies are becoming more valuable faster than the dilution required to fund them.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Meridian Ventures, a U.S.-based venture firm founded by Harvard Business School graduates Devon Gethers and Karlton Haney, has launched a $35 million debut fund. (Link)

Haun Ventures, a Menlo Park, CA-based venture capital firm, closed Fund II, at over $1 billion. (Link)

New Startup Deals

Chromie Health, a NYC-based AI platform for hospital scheduling and operations, raised $2M in Pre-Seed funding. (Link)

Saile, a NYC-based healthcare staffing and credentialing platform, raised $2.2M in Pre-Seed funding. (Link)

Flick, a San Francisco-based AI-native filmmaking platform, raised $6M in Seed funding. (Link)

Graphon AI, a San Francisco-based enterprise AI intelligence platform, raised $8.3M in Seed funding. (Link)

Ranger AI, a San Francisco-based revenue operations platform for industrial tendering, raised $8.4M in Seed funding. (Link)

Recursive Superintelligence, a London and San Francisco-based self-improving AI company, raised $650M in funding at a $4.65B valuation. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Head of Operations - Allocator One | USA - Apply Here

Vice President, Investor Services - StepStone Group | USA - Apply Here

Associate / Senior Associate - Stepstone Group | Italy - Apply Here

Investment Operations Analyst - Polymath Venture | Mexico - Apply Here

Partner 16, Software Engineer - a16z | USA - Apply Here

Investment Analyst - Lunicorn Venture | UK - Apply Here

Investment Associate - Struck Capital | USA - Apply Here

Visiting Engineer - AI Fund | USA - Apply Here

Finance & Operations Manager - Antler | Singapore - Apply Here

Investment Team - Antler | Germany - Apply Here

Investor (Senior Associate/Principal) - Square Peg | USA - Apply Here

Senior Analyst - ICONIQUE Capital | USA - Apply Here

Program Manager - a16z | USA - Apply Here

Senior Associate - ICONIQUE CAPITAL | USA - Apply Here

Venture Capital Analyst - MicroVentures | USA - Apply Here

PARTNERSHIP WITH US

Get your product in front of over 120,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

was talking to a founder yesterday who's got his whole unit econ built wrong because he didn't realize this change. we've been tracking what 600+ vcs are actually saying about this and it's wild how fast the narrative moved from "ai-native = smaller team" to "yeah but what's your inference cost look like"