The truth behind OpenAI’s $852 billion price tag (What you need to know before the IPO). | Anthropic reveals how close AI is to building itself?

Hundreds of founders revealed about horror VC stories? - A must read thread. & More.

👋 Hey, Sahil here - welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

Why are billion-dollar VC funds racing into seed deals?

The truth behind OpenAI’s $852 billion price tag (What you need to know before the IPO).

Frameworks & insightful posts :

Where is Consumer AI actually headed and who gets to win?

Anthropic reveals how close AI is to building itself?

What did hundreds of founders reveal about VCs? - A must-read thread.

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

FROM OUR PARTNER - CONTENTMONK

🔎 When buyers ask AI for a recommendation, do you show up?

Your buyers don’t only Google anymore. They ask ChatGPT, Perplexity, and Google’s AI what to buy.

ContentMonk shows you where your brand stands across every AI engine, then helps you fix the gaps and be recommended by AI assistants.

See which competitors currently influence AI answers.

Get recommendations for improvement.

Create the content that gets you mentioned.

Most AEO tools stop at analytics. ContentMonk takes you from tracking to being mentioned in one workflow.

Run a free 2-minute AI Visibility audit to see where you stand →

START WITH

🧠 Big idea + report of the week

Why are billion-dollar VC funds racing into seed deals?

One of the most common beliefs in venture capital is that seed investing is still protected territory.

The logic sounds reasonable.

Mega-funds manage billions of dollars. They should be spending their time writing large Series B, C, and growth checks, while emerging managers compete for the earliest deals.

But new research from Pavel Prata at Murph Capital, using Harmonic data, suggests the market has already changed.

The analysis tracked the early-stage investing activity of 10 mega-funds ($10B+ AUM) across three distinct eras: the SaaS era (2015-2019), the ZIRP era (2020-2022), and the AI era (2023-2026).

The conclusion is difficult to ignore:

Mega-funds are doing far more seed investing today than they ever have before.

Some of the numbers are staggering.

Andreessen Horowitz increased from 16.6 early-stage deals per year during the SaaS era to 75.3 deals per year in the AI era. That’s a 4.5x increase.

General Catalyst grew from 15.2 deals per year to 61.5 deals per year, a 4x increase.

Sequoia moved from 19.6 deals per year to 50.6 deals per year.

Lightspeed increased from 11.6 deals per year to 32.1 deals per year.

What’s most interesting is that this wasn’t supposed to happen.

Many investors assumed the explosion in seed activity during 2020-2022 was simply a consequence of free money and zero interest rates.

The expectation was that once capital became more expensive, activity would normalise.

Instead, the opposite happened. a16z and General Catalyst are now investing at levels that exceed their ZIRP peaks.

In other words, this isn’t a temporary distortion. It’s a new baseline.

The research identifies three distinct fund behaviours emerging:

Accelerators: a16z, General Catalyst, and Khosla Ventures are investing in more seed deals today than ever before. They didn’t pull back after ZIRP ended. They accelerated.

Stabilisers: Sequoia, Accel, and Lightspeed have moderated from peak activity levels, but still operate at roughly 2-3x their SaaS-era pace.

Disciplined operators: Bessemer, Index Ventures, and Lux Capital avoided extreme spikes but still increased their seed activity materially compared to a decade ago.

The result is a dramatic shift in market structure.

During the SaaS era, these 10 firms collectively completed roughly 140-150 early-stage deals annually.

Today they complete roughly 370-400 deals per year.

That’s almost triple the volume.

For founders, this means there are more well-capitalised investors willing to write seed checks than ever before. But for emerging managers, the implications are more complicated.

The competitive landscape is no longer a handful of seed specialists competing against each other.

It’s seed specialists competing against firms with billions in capital, massive platform teams, global networks, and established brands.

The takeaway isn’t that emerging managers can’t win. It’s that they can no longer rely on “we invest earlier” as a differentiator.

The firms that succeed will be the ones that can clearly answer a harder question:

Why should a founder choose you when Sequoia, a16z, General Catalyst, and Accel are all playing the same game?

That’s becoming the defining question for the next generation of venture firms.

The truth behind OpenAI’s $852 billion price tag (What you need to know before the IPO).

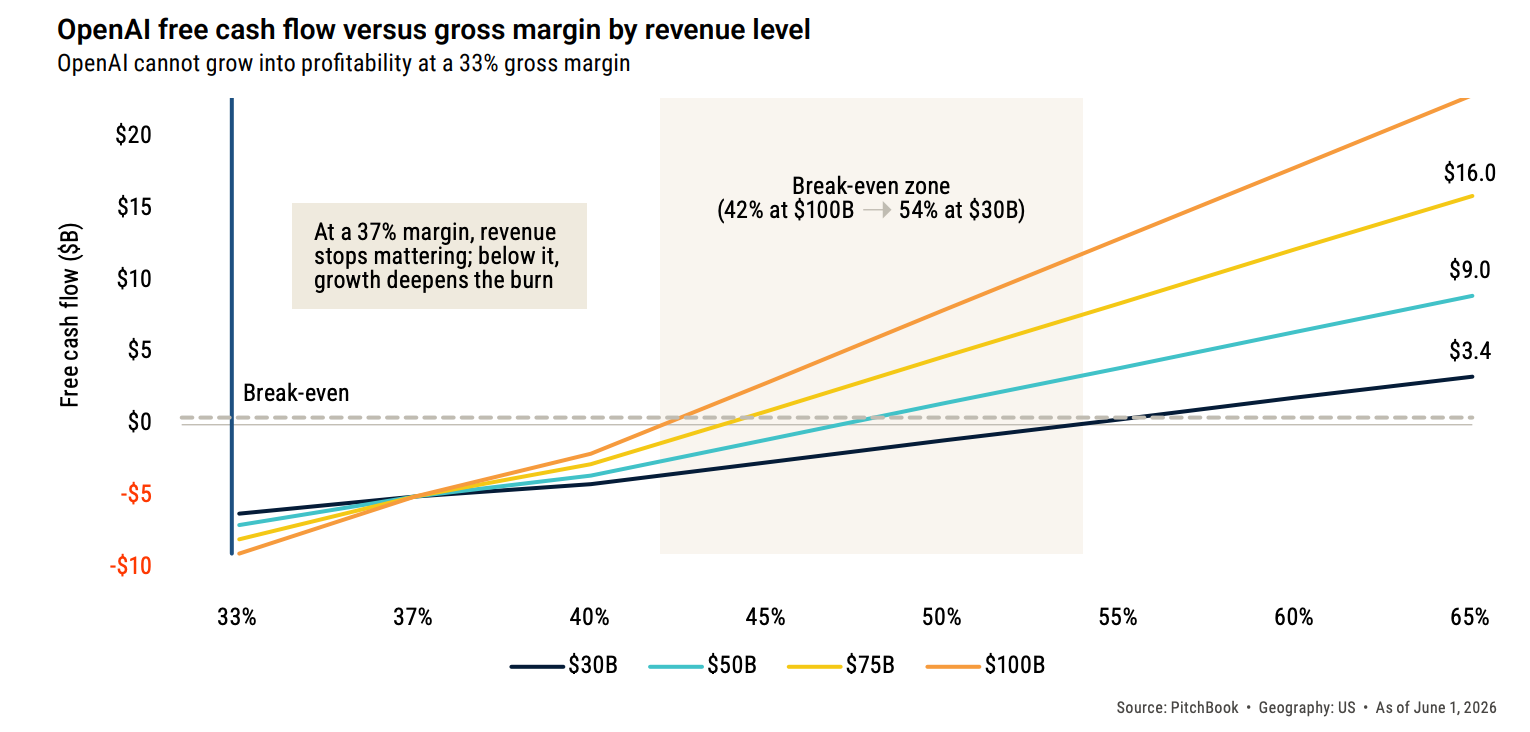

OpenAI is racing toward a $1 trillion IPO with 905 million weekly active users, 92% Fortune 500 penetration, and ~$30B in trailing ARR. On paper, it looks like the undisputed AI leader. But a fresh analyst note from PitchBook tells a different story - one where the price tag is running far ahead of the business.

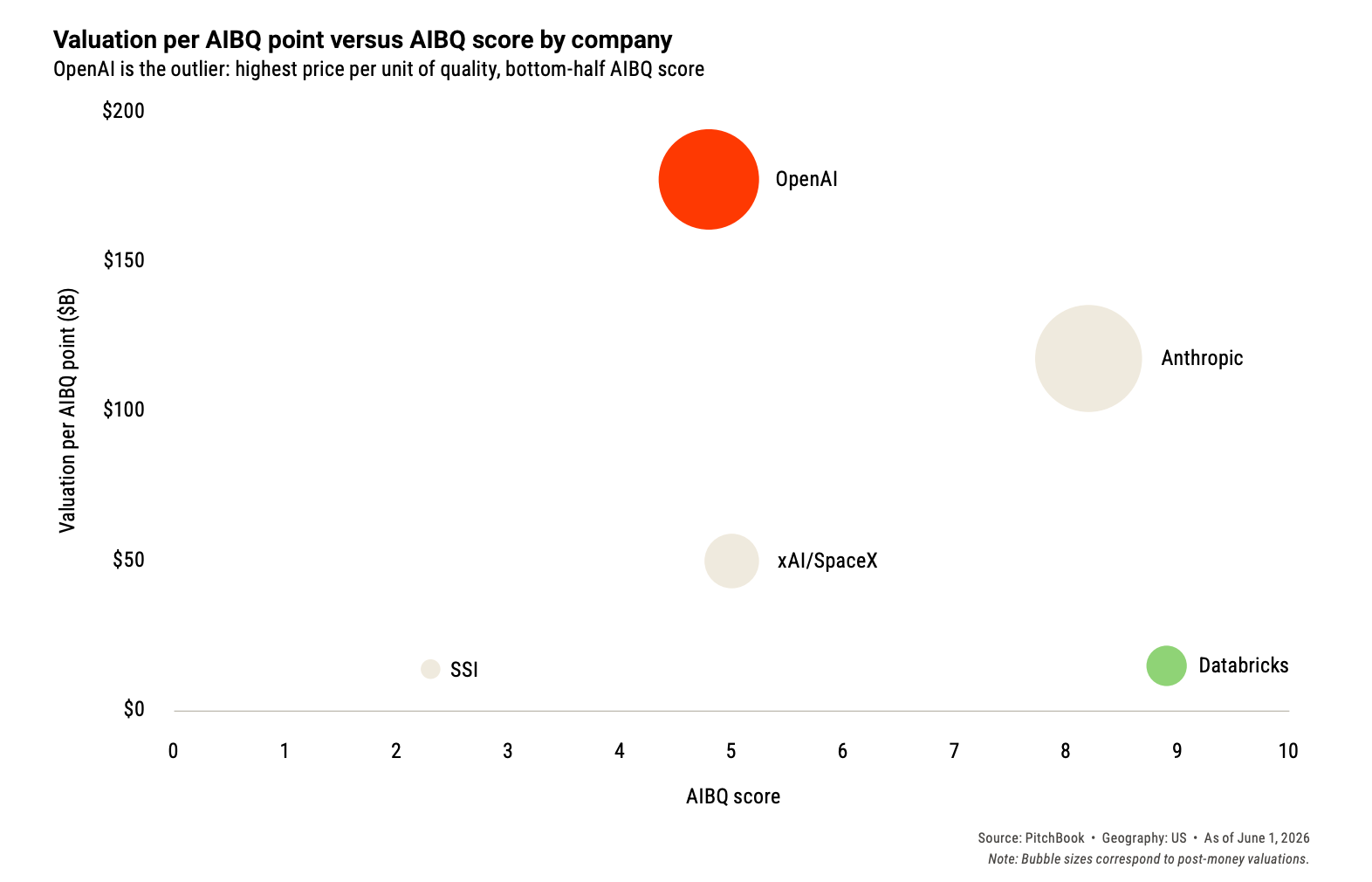

PitchBook scored OpenAI using their AI Business Quality (AIBQ) framework across five dimensions - capital efficiency, revenue quality, compute independence, governance, and moat durability.

OpenAI landed 4.8 out of 10, dead last in its peer group, while trading at $177.5B per AIBQ point - 11.7x the rate of Databricks at $15.1B per point. The brand is everywhere. The fundamentals are another conversation.

Here’s what the numbers actually show:

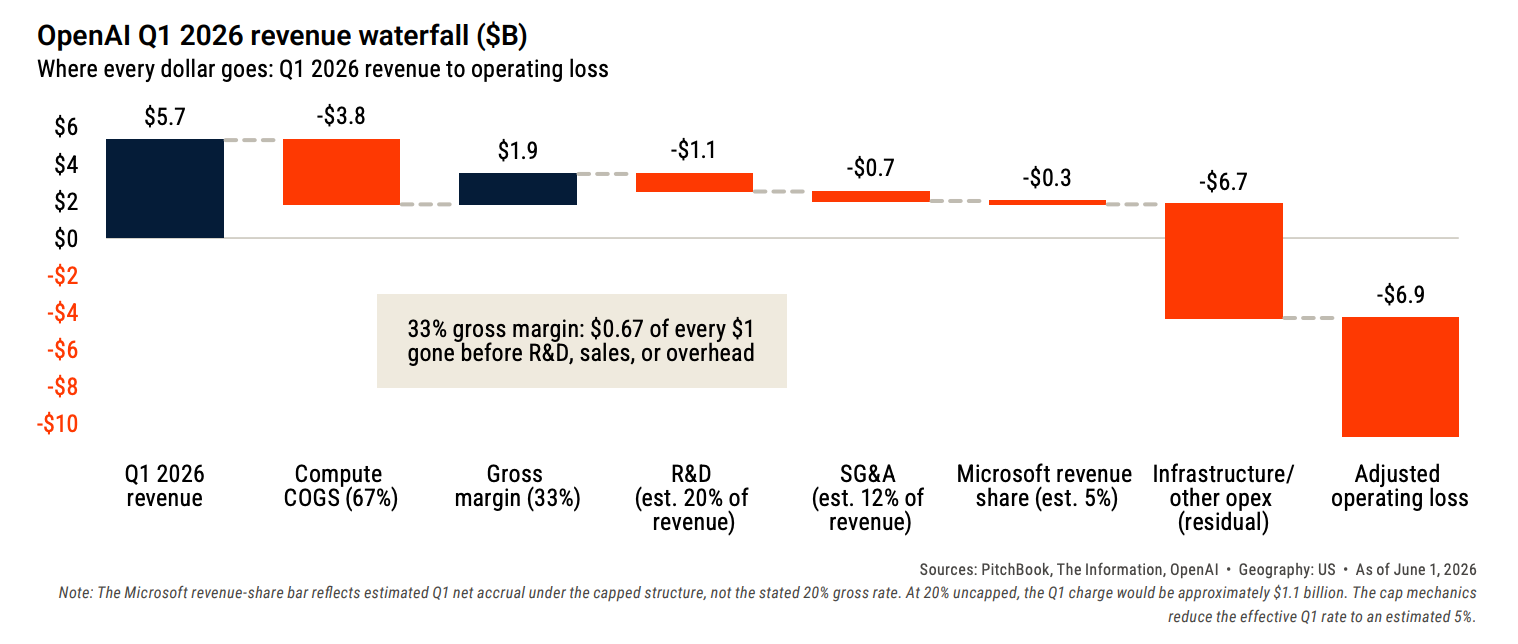

Q1 2026 revenue was $5.7B - but OpenAI burned ~$7B that same quarter, spending $2.22 for every dollar earned, with a -122% adjusted operating margin

67 cents of every revenue dollar goes to compute costs before a single dollar reaches R&D or sales - against an internal gross margin target of 46%, the actual figure sits at 33%

Break-even ARPU is ~$80/month. ChatGPT Plus costs $20. Only the $200 Pro and custom Enterprise tiers actually cover their cost of delivery

Total infrastructure commitments sit at ~$1.2 trillion across Azure, Oracle, AWS, and others - with committed compute alone ramping to $80B in 2028, which exceeds OpenAI’s projected revenue that year

Annual subscriber churn runs at 41%; nearly half the user base turns over every year, yet net revenue retention sits at 88%, well below the 120%+ benchmark institutional investors expect from SaaS businesses

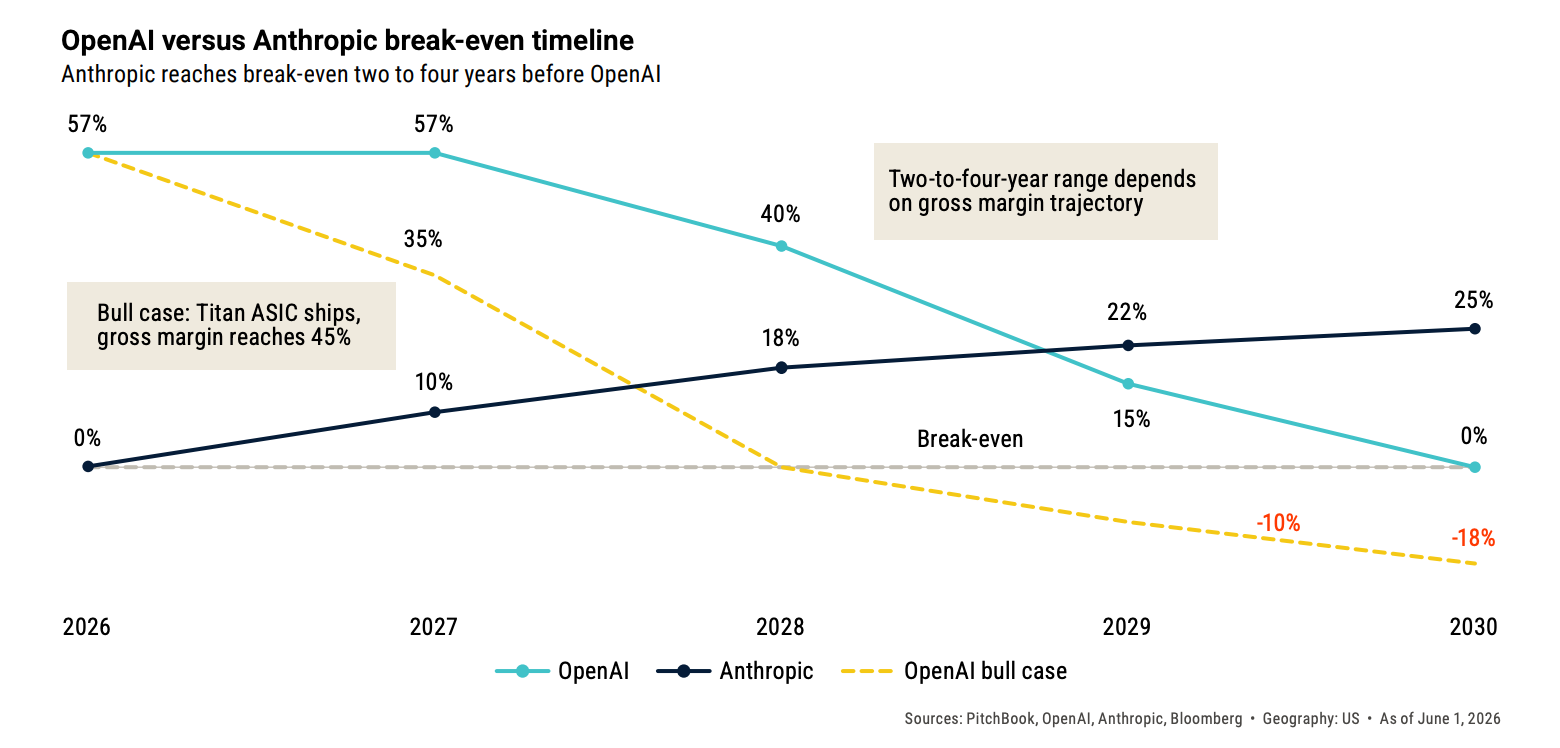

The Microsoft deal is simultaneously OpenAI’s biggest relief and its biggest unknown. A renegotiated $38B revenue-share cap saves OpenAI an estimated $70B–$97B through 2030 - without it, profitability is mathematically impossible.

But post-2030 terms are completely undisclosed, and that’s precisely when OpenAI expects first to turn cash flow positive.

The competitive picture is shifting fast too:

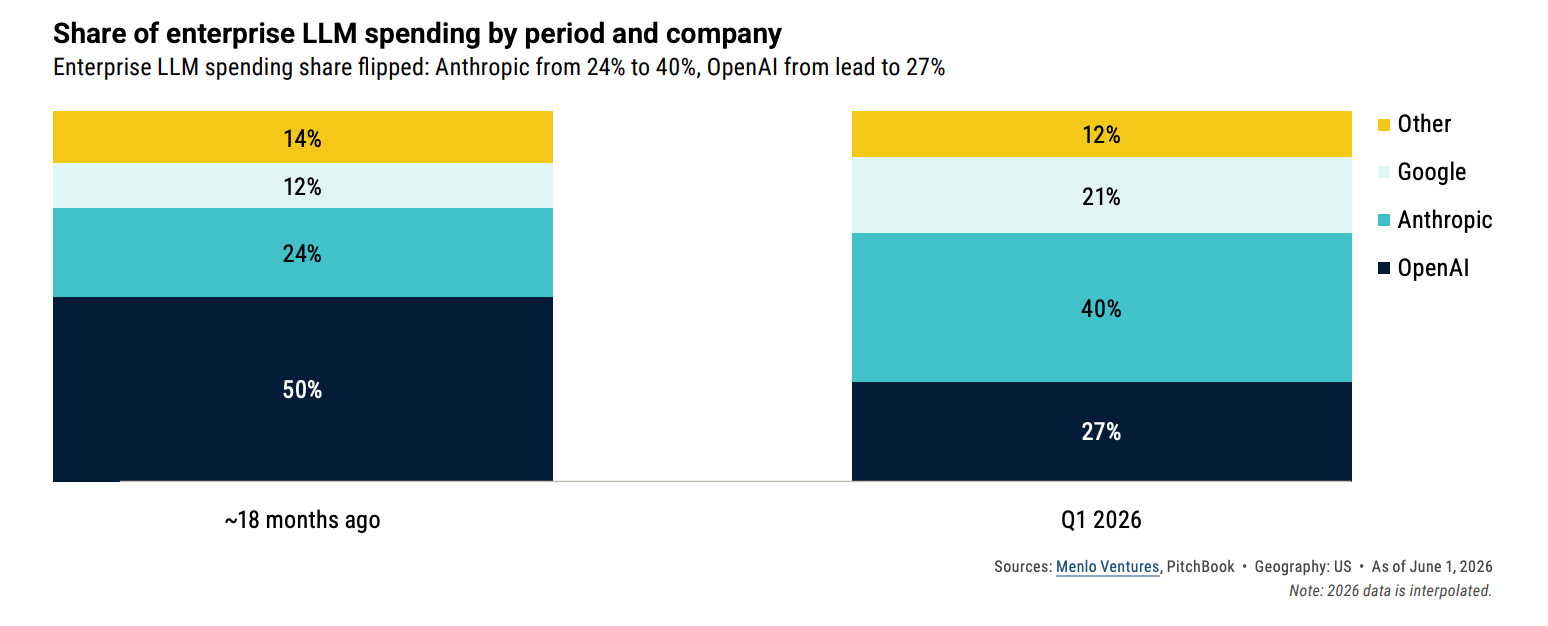

18 months ago, OpenAI led enterprise LLM spending at 50%. Today it’s at 27%, with Anthropic surging from 24% to 40%

Claude Code now holds ~54% enterprise coding market share with ~$2.5B ARR, and coding is where enterprise relationships are won

ChatGPT’s share of AI web traffic fell from 86.7% to 64.5% in just 12 months

Anthropic, now valued at $965B, just filed its confidential S-1 on June 1 and is projecting its first profitable quarter - while OpenAI projects $665B in cumulative cash burn through 2030

If Anthropic lists before OpenAI, OpenAI prices against a profitable competitor at a higher valuation and a better AIBQ score. PitchBook sees no scenario where that favours OpenAI.

Working backwards from the $852B valuation, the implied 2030 free cash flow needed is $95B–$105B. The current trajectory points to a range between -$10B and -$30B.

Closing that 3x–7x gap requires gross margins to nearly double, $1.2T in infrastructure commitments to shrink, consumer monetisation to accelerate, and a Microsoft renewal that hasn’t even been negotiated yet - all simultaneously.

The scale is real. The window to justify the price is narrowing.

FEATURED POSTS

📬 Must-read posts

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

SOMETHING MORE

🧩 Frameworks & insightful posts

Where is Consumer AI actually headed and who gets to win?

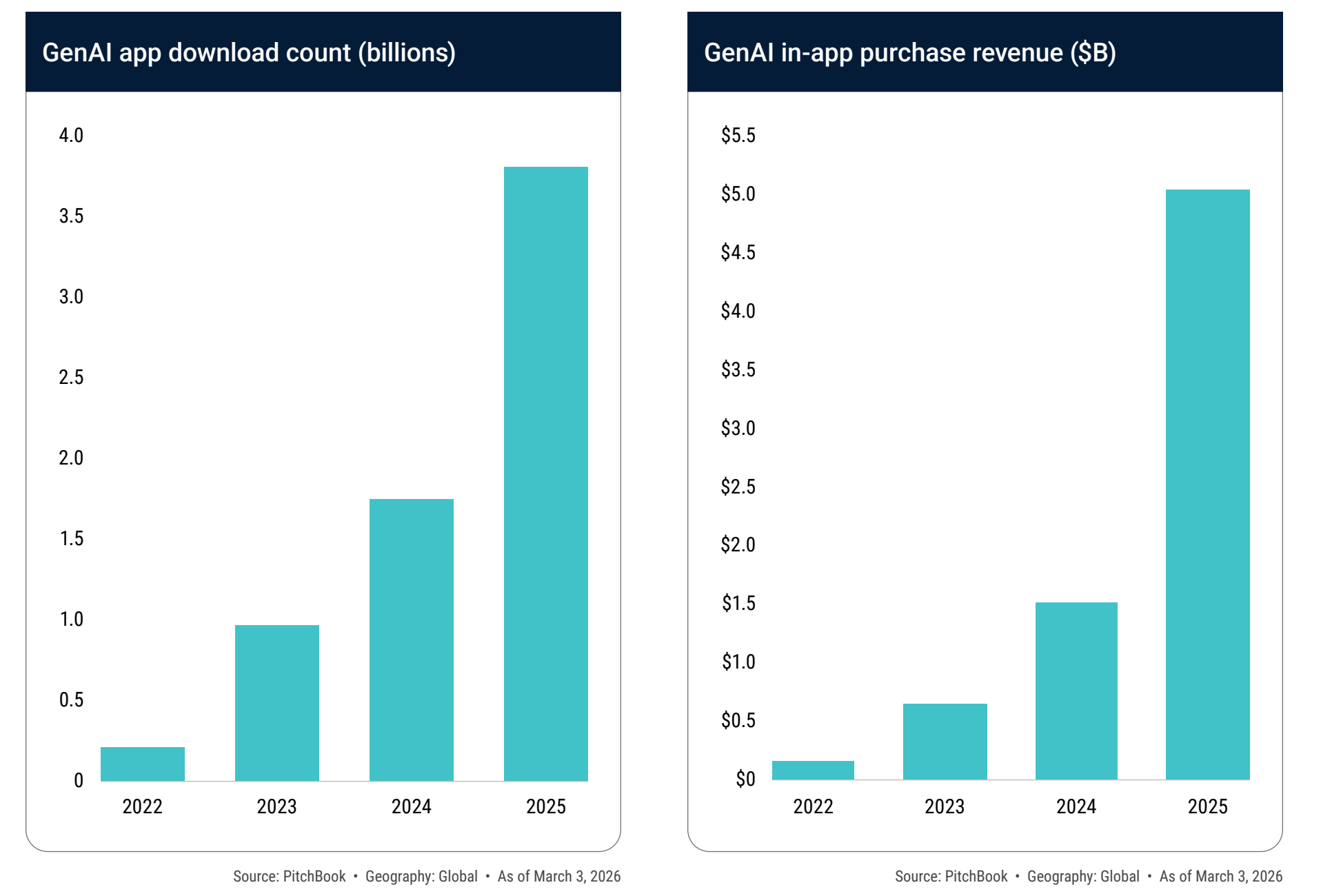

Consumer AI is growing fast. GenAI app downloads went from roughly 200 million in 2022 to 3.8 billion in 2025, and mobile in-app purchase revenue scaled from under $200 million to $5 billion over the same period.

But PitchBook’s latest State of Consumer AI report digs past the headline numbers and finds a market that is deeply concentrated, structurally bifurcated, and increasingly unforgiving for anyone outside the top tier.

The demand signal is real - but so is the monetization gap.

Content creation leads usage across both Claude (43% directive share) and ChatGPT (28% message share), with $3.8 billion in VC deal value growing 85% YoY.

Education shows the starkest disconnect: strong engagement on both platforms but VC funding down 65% YoY.

The reason is simple - OpenAI’s paid conversion rate sits at just 5%, which actively suppresses willingness to pay across the category rather than building toward it.

A few things reshaping how this market gets built and funded:

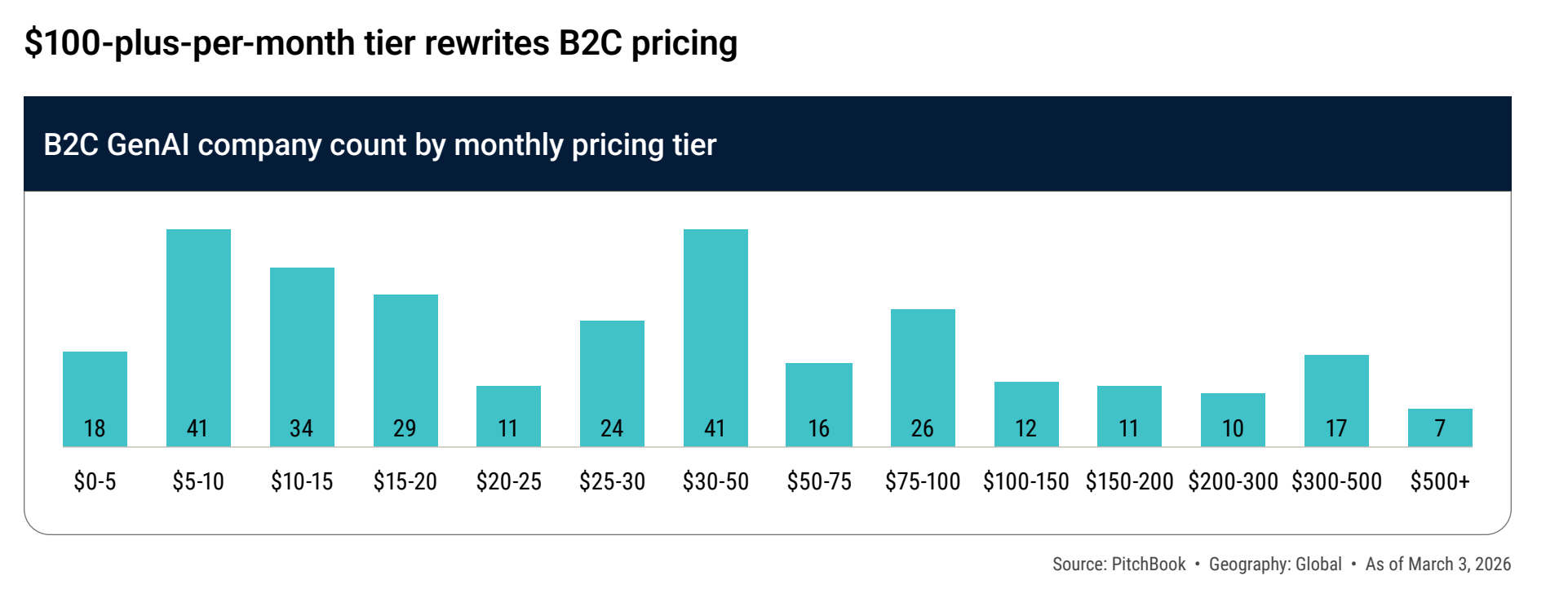

Consumer AI pricing has broken into new territory.

Before ChatGPT, $100+/month was commercially nonviable for consumer products. Now 57 startups charge above that threshold. OpenAI’s $200/month Pro tier and Perplexity’s $167/month plan both exceed what consumers pay for Amazon Prime annually ($139).

The catch: inference costs remain high, unit economics are strained, and only a narrow cohort of productivity-oriented platforms can hold those prices.

The K-shaped economy is shaping the market structure.

The top decile of US earners owns 87% of domestic equities, while 90% of households face rising debt burdens, credit card balances up ~6% YoY, and $18.8 trillion in total household debt.

This forces B2C AI to monetize at the extremes: premium productivity tools for high earners, or free-tier mass market products competing directly against labs subsidizing hundreds of millions of users indefinitely.

Late-stage return math is quietly breaking.

Median Series D+ ownership has fallen from 13.3% to 6.2% since 2016. A 6% stake in a $5 billion platform now requires a $15 billion+ exit just to 2x.

The practical implication is that growth-stage consumer AI has migrated from an ownership-driven return model to a price-appreciation-driven one - which means a lot more rides on picking the right companies early.

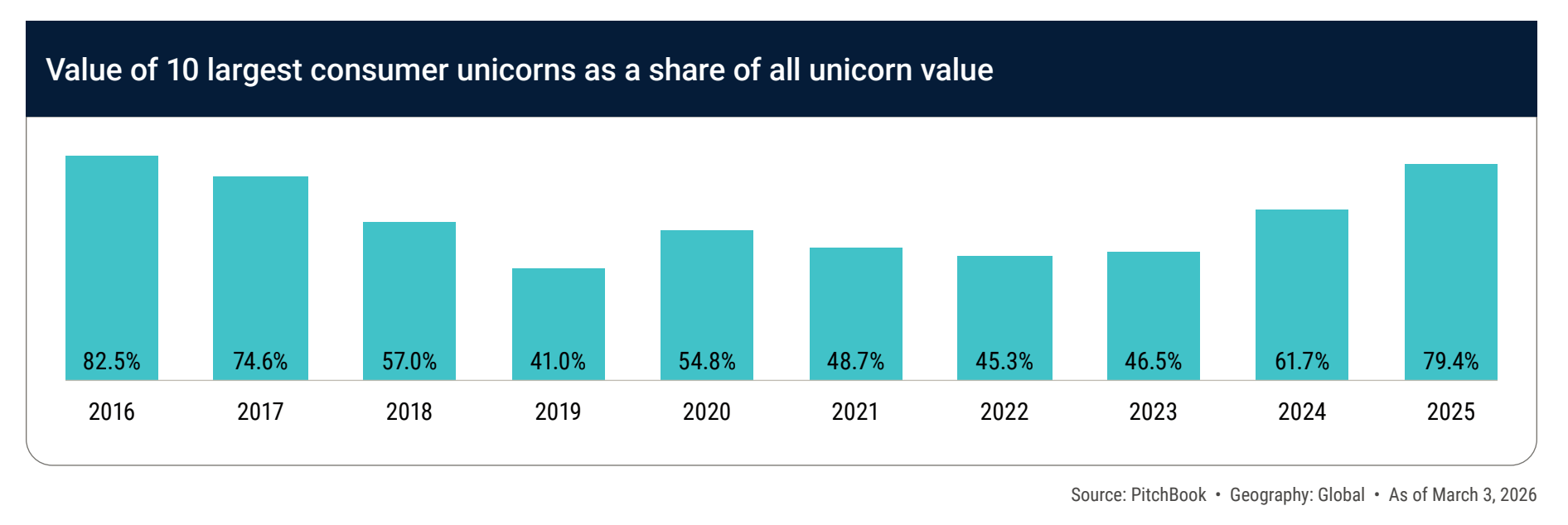

The value is extremely concentrated.

The top 10 consumer AI unicorns now represent 79.4% of total category value, up from 61.7% in 2024.

The entire “consumer unicorn” asset class is functionally a bet on 10 companies. Everything else is competing for the remaining 20%.

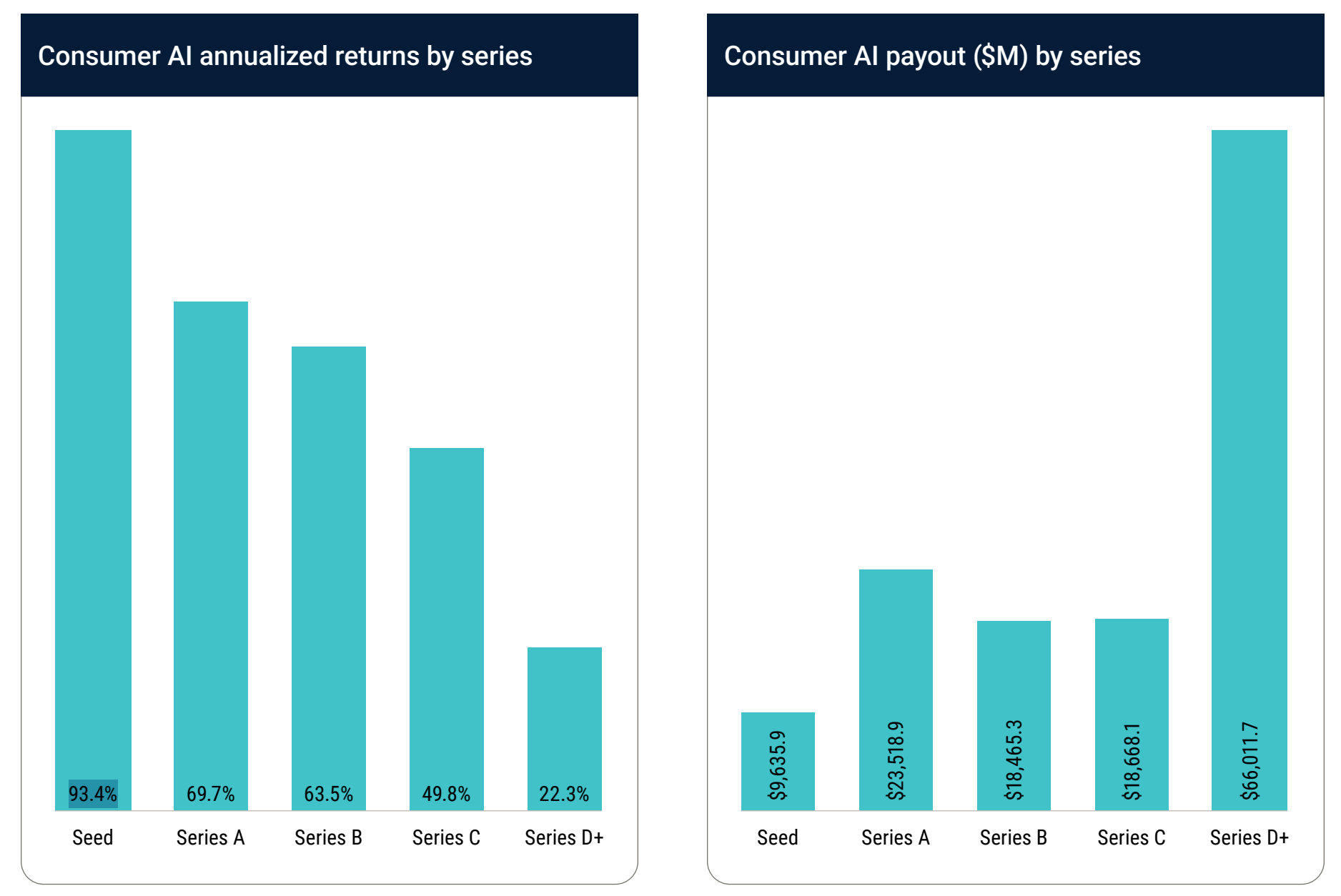

Series B is the sweet spot.

Seed posts the highest annualized returns at 93.4%, but dollar failure rates hit 34.8% driven by overfunded rounds, not failed companies.

Series B offers a better risk-adjusted profile: 97.1% company survival rate, 63.5% annualized return, and only 5.4% dollar failure rate.

PitchBook’s suggested playbook is disciplined seed checks for product-market fit, then concentrated Series B positions in the survivors.

The IPO window hasn’t opened for most B2C names. Of recent VC-backed IPOs, only -

CoreWeave has meaningfully outperformed - up 98.9% since listing.

Klarna is down 70.4%, Figma down 74.6%, StubHub down 56.5%.

The market is demanding proof of profitability before rewarding consumer platforms, and the gap between profitable and unprofitable B2C companies in public markets - now roughly 1.5x to 2x in EV/TTM multiple, is only widening.

The question isn’t whether consumer AI is growing. It clearly is. The question is whether the growth is translating into durable businesses and right now, that answer belongs to very few companies.

Anthropic reveals how close AI is to building itself?

Something quietly significant dropped this week. Not a model launch, not a valuation headline - Anthropic published an internal data dump on how much of their own work AI is already doing. And it reads less like a PR piece and more like a rare moment of honesty from one of the most important labs in the world.

The number that stops you cold: over 80% of the code merged into Anthropic’s codebase today was written by Claude.

A year ago it was low single digits. That’s not a gradual shift - that’s a flip.

The piece traces exactly how this happened and where it’s heading. The timeline is worth sitting with:

2021–2024 - Engineers write code, Claude occasionally helps with snippets

2025 - Claude Code launches, Claude starts writing and editing entire files

2026 - Claude runs autonomously for hours, delegates to other agents

20XX? - Claude potentially designs and trains its own successors

That last step is what they call recursive self-improvement. Not here yet. But the internal data points toward it more clearly than anyone outside the lab would have guessed.

A few things that matter specifically if you’re building or investing right now:

The productivity jump is real and the bottleneck keeps moving

Anthropic engineers are merging 8x as much code per quarter as they were in 2024. But the more interesting signal is what happened after.

, and Claude Mythos Preview.")

Once Claude wrote the code, human review became the constraint. Once Claude ran experiments, choosing which ones to run became the constraint.

Every time one layer gets automated, the ceiling drops to whatever humans are still doing. That loop will repeat across every knowledge-work company, not just AI labs. The teams that spot the new bottleneck fastest are the ones that pull ahead.

The task horizon is expanding faster than most people track

Early 2024 Claude handles 4-minute tasks reliably

Early 2025 - Claude Sonnet 3.7 handles 90-minute tasks

Today - Claude Opus 4.6 handles 12-hour tasks

, Mythos Preview, and Claude Opus 4.7.")

The doubling rate is every four months. Week-long tasks are in range this year. Month-long tasks by 2027. That’s not a feature update - it’s a fundamentally different category of tool arriving every few months. Products and workflows built around today’s capabilities will feel dated fast.

The research autonomy experiment is the most underreported thing in this piece

Anthropic gave Claude-powered agents an open AI safety problem - no hand-holding, just a question and compute access.

Two humans working for a week recovered 23% of the performance gap on the problem. The agents recovered 97%, designing every experiment themselves. The only thing humans did was pick the problem to work on.

The gap that still exists is judgment - knowing which problems matter, which results to trust, when an approach is a dead end. Real gap, genuinely still human. But the honest read is that this might just be the next thing on the curve.

What this actually means if you’re building

The 100-person company doing the work of a 1,000-person one isn’t a pitch deck line anymore - Anthropic is already living it internally. But the unlock isn’t just speed. It’s surface area. Things that were permanently on the backlog get done. In one example from the piece, Claude shipped over 800 fixes that reduced a class of API errors by 1,000x.

The engineer overseeing it estimated a human would have taken four years. That’s not productivity - that’s a different category of what’s possible.

What this means if you’re investing

If engineering output per person scales 8x in two years, the advantage of having more engineers shrinks fast. Distribution, taste, trust, and proprietary data start mattering more than headcount.

The companies still pricing deals around team size as a proxy for execution capacity are using the wrong model. That rerating is already underway - it just hasn’t fully shown up in how term sheets get written yet.

The governance piece at the end - whether labs can actually coordinate a slowdown, whether verification regimes for AI training are even buildable - is the part most coverage will skip. Worth not skipping.

What did hundreds of founders reveal about VCs? - A must-read thread.

For years, founders have swapped VC horror stories in private group chats, dinners, and late-night founder calls.

Rarely do they say them publicly.

That changed this week when a simple post from founder Greg Isenberg triggered hundreds of founders to share their most memorable fundraising experiences. The stories ranged from hilarious to shocking, offering a rare look into the other side of venture capital.

Here’s a quick rounded up many of the stories, and the thread quickly became one of the most talked-about conversations in startup circles.

Some of the stories stood out:

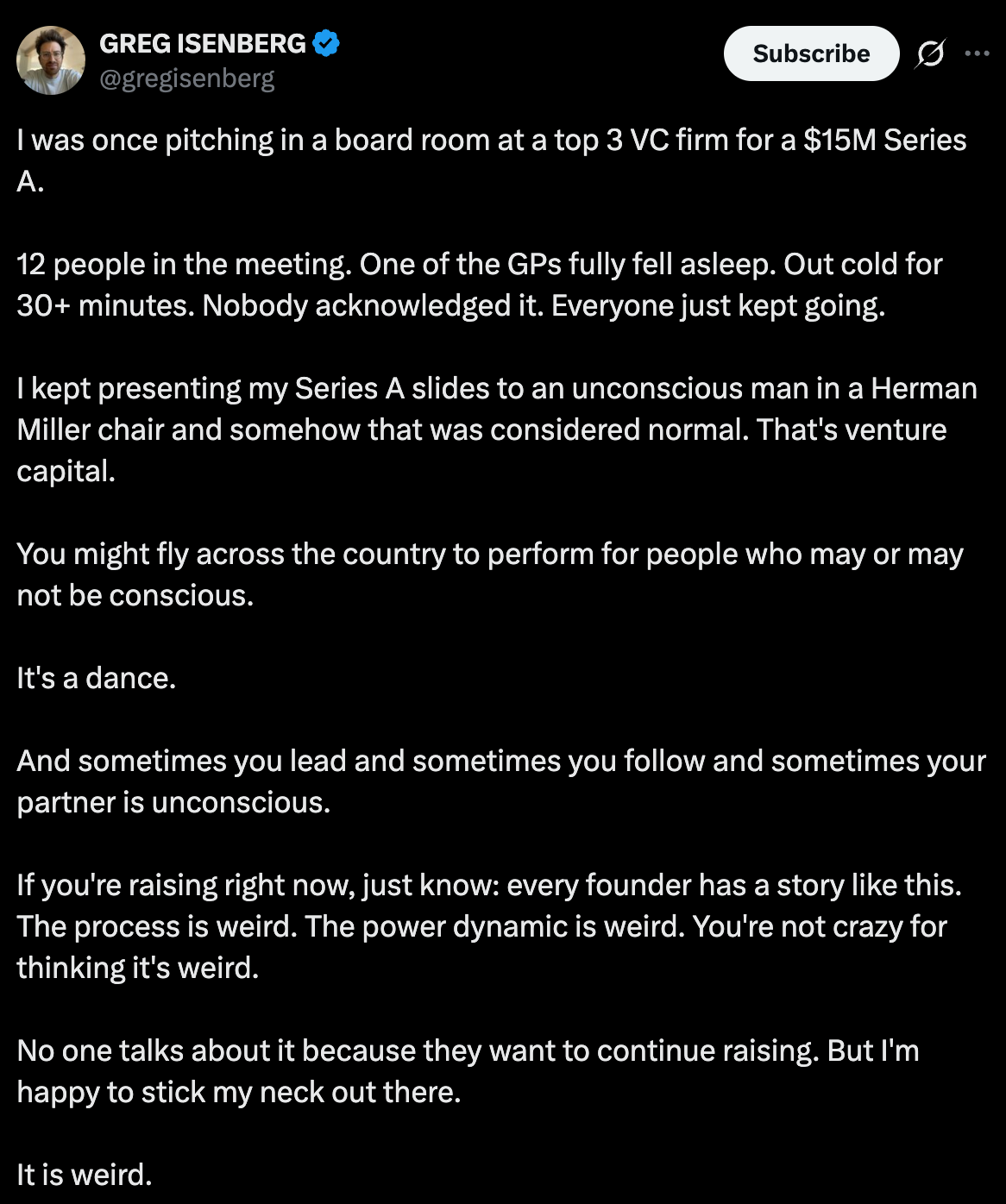

Greg Isenberg shared that while pitching a $15M Series A to one of Silicon Valley’s top VC firms, a partner fell completely asleep for more than 30 minutes. Nobody acknowledged it. Everyone just continued the meeting.

Zynga founder Mark Pincus experienced something similar. One investor slept through his pitch, and his friend encouraged him to keep presenting anyway.

Former WayUp founder Liz Wessel said a well-known investor slept during her Series A pitch, yet the firm later sent a term sheet. Her team ultimately rejected the offer.

Uber founder Travis Kalanick shared that a VC tried to quietly leave a meeting before hearing his pitch. Kalanick followed him all the way to his car and continued pitching from the passenger seat.

One founder described investors signing term sheets and later disappearing before wiring money. Some reportedly continued asking for company updates afterward as if they were investors.

The most surprising stories came from Cloudflare founder Matthew Prince.

Prince said one investor passed on Cloudflare because he allegedly believed a woman couldn’t lead a cybersecurity infrastructure company. That woman was Cloudflare co-founder Michelle Zatlyn. Today, Cloudflare is worth tens of billions of dollars.

Prince also shared another story involving legendary investor Vinod Khosla. According to Prince, after offering to invest, Khosla allegedly suggested he remove his co-founders and keep their equity for himself. Prince said the conversation ended any possibility of working together.

Not everyone joined in to criticize investors.

Several founders pointed out that many VCs are thoughtful, supportive, and genuinely helpful partners. But the sheer volume of stories revealed something important: strange fundraising experiences are far more common than most people realize.

The deeper lesson isn’t about bad investors. It’s about power.

Most founders only feel comfortable sharing these stories after they’ve built successful companies, sold businesses, or no longer need venture capital. The founders naming names today are often the ones who already have leverage.

For early-stage founders, the thread serves as a reminder that fundraising is a two-way diligence process. Investors are evaluating founders, but founders should be evaluating investors just as carefully.

The right investor can accelerate a company for a decade.

The wrong one can become a problem long after the money hits the bank account.

📬 Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Veriten, a Houston, TX-based research, strategy and investment firm, held the initial close of its second flagship energy venture fund at over $105m. (Link)

Gigascale Capital, a Palo Alto, CA-based venture capital firm focused on the physical economy, closed its first institutional fund, at $250m. (Link)

Benchmark Capital, the Silicon Valley venture firm behind early bets in eBay, Uber, Snap, and Twitter, has raised $2 billion across two new funds, including its first-ever $1.25 billion growth fund. (Link)

New Startup Deals

AethexAI, a Cambridge-based startup building localized voice AI models, raised $3M in Pre-Seed funding. (Link)

Willow, an Israel-based startup building an agentic access platform, raised $7M in Seed funding. (Link)

Ramp, the financial operations platform, raised $750M in Series F funding at a $44B valuation. (Link)

WasabiCard, a Singapore-based stablecoin payment infrastructure company, raised ~$10M in Pre-A funding. (Link)

Quobly, a France-based quantum computing startup building silicon-based quantum computers, raised €115M in Series A funding. (Link)

Terra AI, a Palo Alto-based AI platform helping solve subsurface uncertainty for mineral and energy development, raised $20M in Series A funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Investment Team - Antler | Germany - Apply Here

Chief of Staff - AlpenGlow Venture | USA - Apply Here

Associate, Venture Capital - Artha Venture Partner | USA - Apply Here

Investor (Senior Associate/Principal) - Square Peg | USA - Apply Here

Head of Entegris Ventures - Entegris Venture | USA - Apply Here

Founding Investor - Discipulus Ventures | USA - Apply Here

Investor - Starfire Venture | USA - Apply Here

Senior Analyst - ICONIQUE Capital | USA - Apply Here

Venture AI & Operations Specialist - Blum Venture | Austria - Apply Here

Senior Associate - New York Life Venture | USA - Apply Here

Senior Investment Manager - Resolution Impact Venture | USA - Apply Here

Program Manager - a16z | USA - Apply Here

Associate - Manhattan Venture | USA - Apply Here

VP — Finance & Compliance - Transition VC | India - Apply Here

Senior Associate - ICONIQUE CAPITAL | USA - Apply Here

Venture Capital Analyst - MicroVentures | USA - Apply Here

🔴 PARTNERSHIP WITH US

Get your product in front of over 120,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.