Could AI observability become the next billion-dollar category? | 80,000 AI users revealed about the next billion-dollar opportunity for founders.

AI funding boom creating a venture return problem? & AI observability become the next billion-dollar category?

👋 Hey, Sahil here - Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

Is the AI funding boom creating a venture return problem?

Why are LPs turning bullish on China’s AI market again?

Frameworks & insightful posts :

The all-in-one startup operating system for founders & investors.

Could AI observability become the next billion-dollar category?

What 80,000 AI users revealed about the next billion-dollar opportunity for founders.

FROM OUR PARTNER - ROCKET

🚀 Your Competitor's Next Move Is Already Visible

Rocket Intelligence monitors any company across 9 signal pillars - ads, hiring surges, pricing moves, exec changes, and review sentiment, all interpreted daily.

Before your competitor announces their next product, they hire for it. Before they enter your market, their website tells you. Rocket reads every signal, so you stop reacting and start anticipating.

📬 Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

START WITH

🧠 Big idea + report of the week

Is the AI funding boom creating a venture return problem?

The AI funding boom has created a strange situation in venture capital.

On one hand, many AI companies are growing faster than almost any startups in history. Investors see enormous markets, real enterprise demand, and the possibility that a handful of these companies could become trillion-dollar businesses.

On the other hand, the math behind venture returns is starting to look increasingly uncomfortable.

A new PitchBook analysis from Kyle Stanford highlights just how aggressive pricing has become across AI startups and why more investors are quietly beginning to question whether the eventual exit market can support these valuations.

AI startups are now commanding enormous premiums at every stage

The data shows the valuation gap between AI and non-AI startups widening rapidly.

In Q1 2026:

Median AI Series A pre-money valuations reached $78M, up 84% versus non-AI peers.

Median AI Series B valuations climbed to $270.8M, roughly 55% higher than non-AI companies.

Median AI Series C valuations reached $606.5M, levels not seen since the peak of the 2021 market cycle.

The key point is that this is not isolated to a few outlier companies anymore. The premium now exists across nearly every stage of the AI venture ecosystem.

And the speed of that expansion is accelerating.

The real question is not growth - it is liquidity

Most investors agree that AI is a transformational technology. The harder question is whether today’s private market pricing will eventually hold up when companies face public market scrutiny.

That concern matters because venture returns are ultimately determined by liquidity events:

IPOs

Acquisitions

Secondary transactions

And right now, the market still lacks strong evidence that public investors are willing to support the multiples being created in private AI rounds.

PitchBook notes that companies going public in 2025 often accepted meaningful valuation resets simply to complete their IPOs. The median IPO step-up was just 1.1x from the last private round, an unusually weak outcome by historical venture standards.

That creates an uncomfortable possibility: AI startups may eventually face the same valuation compression that hit SaaS companies after the 2021 peak - only at a much larger scale.

DPI data is becoming a warning sign for the entire venture market

One of the strongest signals in the report comes from venture fund performance itself.

PitchBook highlights that 2019 and 2020 vintage VC funds currently show five-year DPI levels of just:

0.13x for 2019 funds

0.12x for 2020 funds

Those are among the weakest liquidity outcomes seen at this stage since before the global financial crisis.

That matters because today’s AI investors are deploying capital into an ecosystem where the broader exit market has not yet fully recovered.

In other words, venture firms are underwriting massive AI valuations before the industry has proven that liquidity can support them.

Even the secondary market is highly concentrated

The secondary market is currently the closest thing venture has to real-time pricing discovery.

But even there, liquidity appears concentrated in a tiny group of companies.

PitchBook notes that the top 20 startups on secondary platform Hiive represented 86.4% of total trading value in Q4.

That concentration reveals something important:

Investors are still willing to aggressively buy exposure to a very small number of elite AI companies.

But confidence drops sharply outside that top tier.

The implication is that many AI startups may eventually discover that capital availability and liquidity are not nearly as broad as current fundraising conditions suggest.

So, the AI boom is creating some of the fastest-growing companies venture capital has ever seen.

But rapid growth alone does not guarantee strong investor returns. Eventually, every private valuation collides with public market reality.

And right now, nobody truly knows whether today’s AI pricing levels are justified, too high, or potentially still too low.

That uncertainty is what makes this moment so unusual. Investors are not simply betting on company growth anymore.

They are betting that future public markets will accept valuation assumptions that private markets are aggressively pricing in today.

Why are LPs turning bullish on China’s AI market again?

For the last few years, most global conversations around AI investing have centred around the U.S.

OpenAI. Anthropic. NVIDIA. Massive infrastructure spending. Trillion-dollar narratives.

Meanwhile, China’s private markets were largely viewed through a very different lens - regulatory pressure, geopolitical tension, weak domestic consumption, and declining fundraising activity.

But that narrative may be starting to shift.

A new PitchBook analysis on China’s AI market, combined with comments from investors at a Hong Kong industry event, suggests Western LP sentiment toward China is improving again - especially around AI, robotics, infrastructure, and manufacturing-driven technologies.

And the reason is not hype. It is an industrial advantage.

China’s AI advantage may come from the physical layer, not the model layer

While much of the U.S. AI ecosystem is concentrated around frontier foundation models, investors increasingly believe China’s edge may emerge from the infrastructure and hardware side of AI.

That includes:

Manufacturing scale

Robotics

Energy efficiency

Industrial automation

AI applications tied to physical systems

One of the more interesting comments came from Gaocheng Capital’s Jing Hong, who argued that China is effectively “exporting low-cost electricity in the form of tokens.”

The point sounds abstract, but the implication is important. Large language models ultimately depend on:

Chips

Compute infrastructure

Electricity

Low-cost inference

And China appears structurally competitive in several of those layers.

According to Hong, China has roughly double the electricity productivity of the U.S. at nearly half the cost per kilowatt. If inference costs become one of the defining economic bottlenecks in AI, energy efficiency itself becomes a strategic advantage.

Capital is already flowing back into Chinese AI

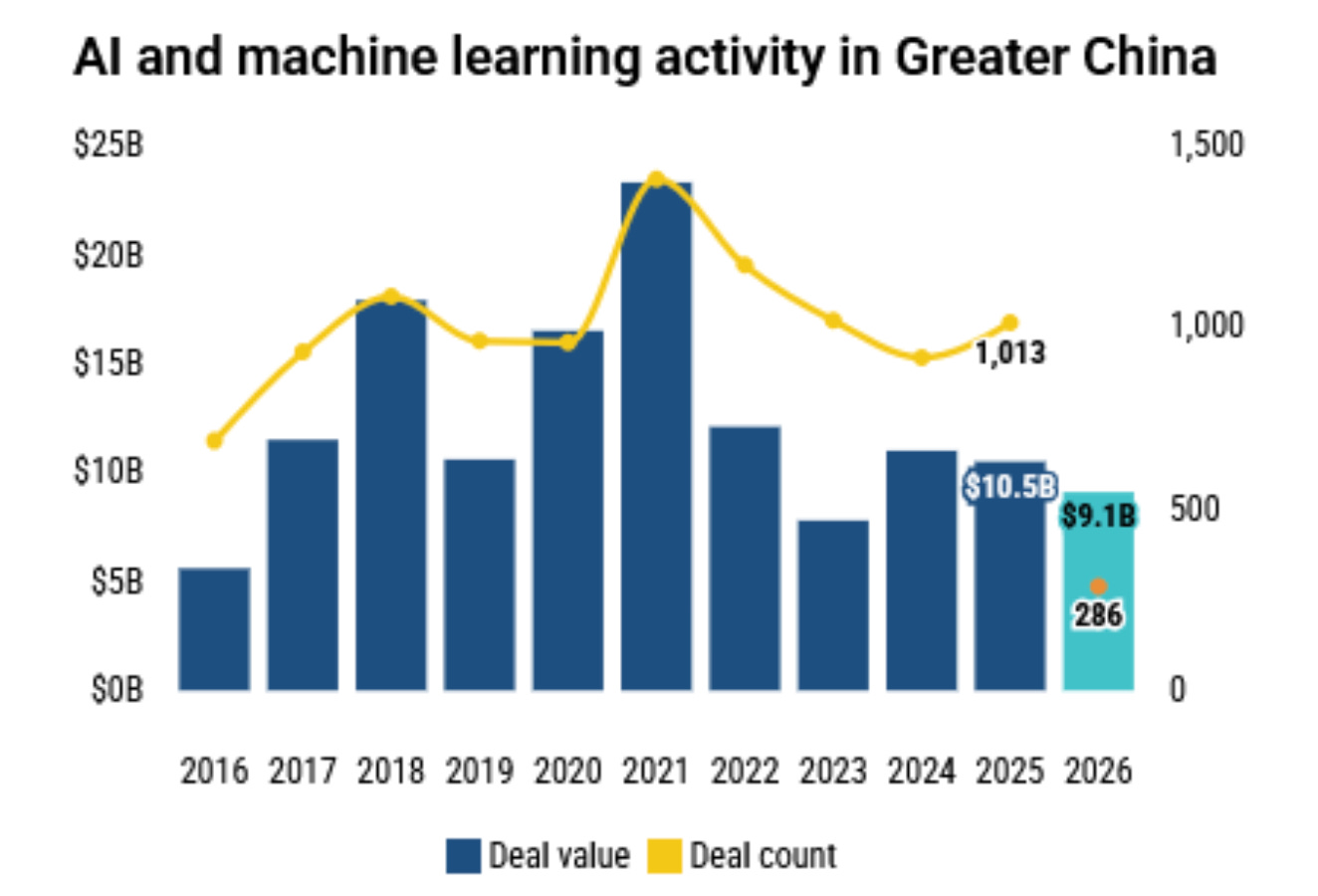

PitchBook data shows AI and machine learning deal activity in Greater China remains resilient despite broader weakness across private markets.

Even after four straight years of fundraising declines, investors at the event repeatedly suggested that Chinese private markets may already be bottoming out.

LGT Capital Partners’ Brooke Zhou noted that Chinese private equity still generated approximately 14% net returns, despite the difficult macro environment.

That matters because many Western LPs had sharply reduced exposure to China over the past few years due to geopolitical uncertainty and concerns around liquidity.

Now, some of that capital appears to be cautiously returning - particularly toward sectors where China maintains clear industrial advantages.

Robotics may become the next major AI trade

Several investors also suggested that the next phase of China’s AI boom may shift away from large language models and toward robotics and embodied AI.

That transition makes sense.

China already dominates many parts of the global manufacturing supply chain. Combining that infrastructure base with increasingly capable AI systems creates a natural pathway into:

Industrial robotics

Factory automation

Autonomous systems

AI-powered manufacturing workflows

InnoVision Capital’s Lane Zhao said that while the first half of 2026 saw heavy focus on large language models, the second half is expected to see significantly more activity around robotics applications.

That may ultimately become one of China’s strongest positions in the global AI race.

Hong Kong’s IPO market is helping sentiment recover

Another major factor improving investor confidence is liquidity.

Hong Kong has reclaimed the top global spot for IPO activity this year, giving investors renewed confidence that exits are still achievable in Chinese markets.

That is particularly important after years of concerns around delayed liquidity and shrinking public market opportunities.

The combination of:

Improving IPO conditions

Strong manufacturing capabilities

Competitive infrastructure costs

AI-driven industrial demand

is beginning to shift sentiment from defensive positioning toward selective optimism.

So, the global AI race is no longer just about who builds the best chatbot.

It is increasingly about who controls the infrastructure underneath AI itself. The U.S. still dominates frontier models and software ecosystems.

But China may be developing a very different kind of advantage - one tied to manufacturing scale, robotics, energy efficiency, and physical AI systems.

And if AI increasingly moves from software into the real world, those advantages may become far more important than many investors currently realise.

FROM OUR PARTNER - SEMRUSH

📈 Semrush helps you create content that actually ranks…

That question has become even harder in the age of AI-generated content.

Semrush’s SEO Writing Assistant helps you understand what top-ranking content is doing differently - from keyword coverage and readability to originality and search intent.

Instead of guessing what Google wants, you get real-time recommendations while you write, helping you create content that’s optimized before you hit publish.

Whether you’re building a startup, growing a newsletter, or scaling a content-driven business, it’s one of the simplest ways to improve your odds of ranking.

🤝 Partnership with us

Get your product in front of over 120,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

SOMETHING MORE

🧩 Frameworks & insightful posts

The all-in-one startup operating system for founders & investors.

Over the last few years, Venture Curator has grown into one of the most-read startup & venture capital newsletters for founders, operators, and investors.

Now we have decided to build something bigger than a newsletter.

Today, we’re launching Venture Curator Premium.

A premium membership designed for founders, operators, and startup people who want access to practical startup resources, deep research, and curated venture insights - all in one place.

What’s included:

150+ Premium Archive Posts - Deep startup breakdowns, founder playbooks, VC insights, AI trends, fundraising strategies, and curated business analysis.

100+ Founder, Startup & VC Resources - Templates, guides, databases, frameworks, and startup operating resources.

A few resources are already included:

All-In-One Venture Capital Interview Guide

Startup Financial Projection Templates

SaaS Financial Model Templates

Cap Table Builder

Pitch Deck Storytelling Framework

Investor CRM & Fundraising Tracker

Startup Valuation Guide

Investor Q&A Preparation Kit

Startup Legal Document Pack

Founder Operating System (Notion)

Investor Outreach Email Templates

40 Real Startup Pitch Decks That Raised $350M+

Plus investor databases, including:

2,700+ US Investors

350+ Indian Investors

400+ French Investors

300+ Australian Investors

150+ African Investors

1,000+ European VC Firms

250+ Latin America VC Firms

Premium members will also get:

2–3 premium editions every week

Exclusive startup & VC research

Curated startup opportunities

Founder/operator insights

Access to future premium resources

Early Supporter Offer (4 Days Only) - Upgrade to Venture Curator Premium and save 15% forever for the next 4 days.

Could AI observability become the next billion-dollar category?

There’s a strange disconnect happening inside enterprises right now. AI agents are moving fast - from experiments to production, but the systems to measure their impact are still catching up.

A recent report from CB Insights highlights this gap clearly: in a survey of executives, 80% said AI agents are a priority… yet 40% admitted they either can’t track ROI or don’t even know how to measure it.

That’s not a small problem. It’s a signal. Whenever adoption moves faster than measurement, a new infrastructure layer is built.

And that’s exactly what’s happening here.

The next wave of AI startups won’t just build agents - they’ll build the systems that explain whether those agents are actually working.

Three categories are quietly emerging as the backbone of this shift:

Observability & evaluation (knowing what your agents are doing)

Memory infrastructure (helping agents retain and use context)

Cost + ROI attribution (linking spend to real business outcomes)

Each of these solves a different bottleneck - but together, they define how AI agents scale inside real companies.

Take observability first.

Right now, agents fail silently more often than people think. They hallucinate, mis-handle workflows, or break in edge cases - and without proper tooling, no one even notices.

That’s why this has become the most active AI market right now by deal count. What’s interesting is how fast this layer is becoming “must-have”:

Startups are building automated evaluation systems that test agents before deployment

Others are using reinforcement learning from real-world failures to continuously improve agents

Simulation tools are running thousands of scenarios to stress-test agents at scale

Even incumbents like Snyk and Coralogix are acquiring in this space - clear signal that monitoring won’t stay a feature, it becomes core infrastructure.

Then comes memory.

Most AI agents today are still surprisingly “forgetful.” They handle tasks well in isolation but struggle in real enterprise environments where context matters - past conversations, internal data, workflows across teams.

That’s why memory is emerging as a separate category. Not just storing chat history - but building systems where agents can:

Decide what information matters

Update their memory over time

Retrieve the right context across sessions and systems

This directly addresses one of the biggest adoption blockers companies report: integration complexity and lack of internal expertise.

If agents can “remember” the business, they become far more useful. Finally, the hardest piece: cost and ROI attribution.

Most companies today track AI success using proxy metrics:

Time saved

Productivity gains

Cost reduction

But only ~25% are actually measuring revenue impact. That’s a huge gap.

Because AI doesn’t become a budget priority until it ties to outcomes. This is where a new generation of tools is emerging:

Platforms that map model usage and token spend to business metrics

Systems that track costs across multiple AI providers and agents

Tools that show how changes in prompts or models impact revenue, latency, and quality

Right now, this category is still early - but it’s arguably the most important one because visibility without outcomes doesn’t drive decisions.

What’s really happening here is a shift in where value gets created. The first wave of AI was about building capabilities.

The next wave is about making those capabilities measurable, reliable, and economically justifiable.

And that’s where the biggest opportunities now sit. If you’re building in AI today, it’s worth asking a simple question:

Are you building the agent… Or the layer that helps companies trust, scale, and pay for those agents?

Because history suggests the second layer often ends up just as valuable.

What 80,000 AI users revealed about the next billion-dollar opportunity for founders.

Most conversations about AI get stuck in abstractions. We hear big claims about job loss, AGI, productivity, safety, and existential risk, but much less about a simpler question: what does “AI going well” actually look like for real people already using it?

Anthropic recently ran one of the most interesting studies I’ve seen on this. It invited Claude users to describe how they use AI today, what they hope it could unlock in their lives, and what worries them most. More than 80,000 people across 159 countries and 70 languages participated, which makes this less like a normal product survey and more like a global snapshot of how people are beginning to fit AI into everyday life.

What makes the findings valuable is that they move beyond generic optimism or fear. They show where AI is already delivering value, where it still feels shaky, and what kinds of products or companies are likely to matter next.

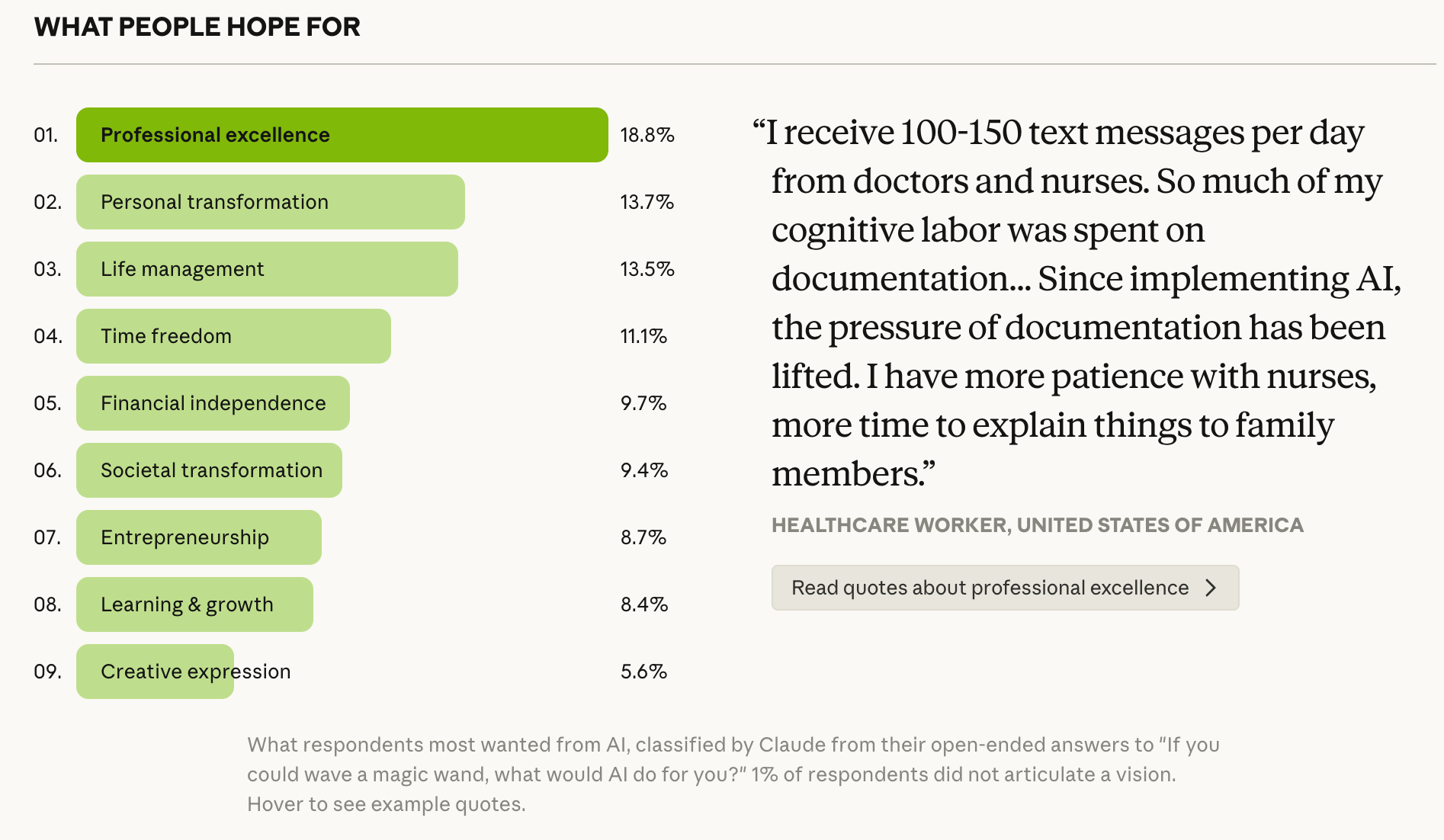

The biggest thing people want from AI is not magic. It’s a relief.

When Anthropic asked people what they most wanted from AI, the answers were surprisingly grounded. The top categories were:

That tells you something important. Most people are not asking AI to become some futuristic super-being. They want it to help them do better work, reduce mental overload, manage life logistics, learn faster, and reclaim time.

That’s a useful correction for founders. The most immediate demand is not for “AI for everything.” It’s for products that remove friction from real life.

A lot of the strongest responses had the same emotional structure underneath them:

AI helped me do what I already needed to do, but with less stress and more breathing room. Someone used it to reduce documentation burden at work. Someone used it to learn coding despite a learning disorder. Someone used it to ask questions they felt embarrassed asking other people.

So, the best AI products may not be the ones that feel the most futuristic. They may be the ones that quietly remove cognitive load.

Work is still the main wedge, but quality of life is the real promise

The largest category people mentioned was “professional excellence.” That makes sense. Work remains the easiest entry point for AI because the ROI is easier to spot. If AI saves time, improves output, or helps someone get through repetitive tasks faster, the benefit is obvious.

But what’s more interesting is what sat underneath that answer. Many people started by talking about productivity, then revealed that what they really cared about was what productivity enabled outside of work: more time with family, more emotional energy, less admin, less mental clutter.

That distinction matters.

A founder might think they’re building a productivity product, when in reality the real value proposition is:

more time freedom

less anxiety

less friction in daily life

more space for better work and better living

That is a much richer product insight than “help users move faster.”

AI is already delivering in a few very specific ways

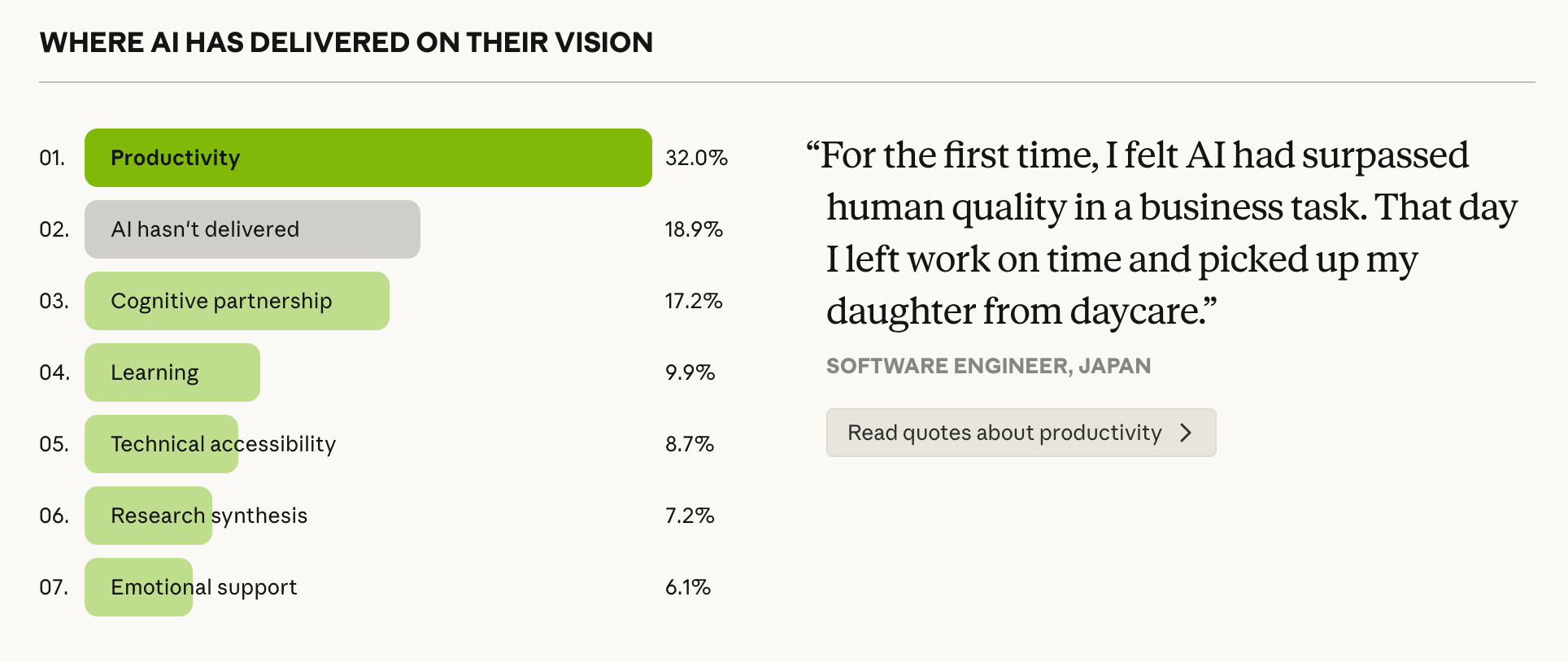

When Anthropic asked whether AI had already taken a step toward users’ goals, 81% said yes. That’s a meaningful number. But the shape of delivery matters more than the headline.

The main buckets where people felt AI had already helped were:

This mix is fascinating because it shows that AI is not just being used as a faster search engine. It is already functioning as a kind of thought partner, teacher, translator, research assistant, and in some cases, even an emotional support layer.

Some of the strongest responses came from people who felt AI gave them access to things they previously couldn’t reach. Not because the knowledge didn’t exist, but because the format was inaccessible, judgment-heavy, too expensive, or too difficult to navigate. That’s a powerful clue about where AI creates the most real value: not just speed, but access.

For builders, that opens up a big product opportunity. AI seems especially strong when it does one of three things:

reduces intimidation

removes judgment from learning

translates complexity into something people can act on

That’s a better lens than simply asking whether a task can be automated.

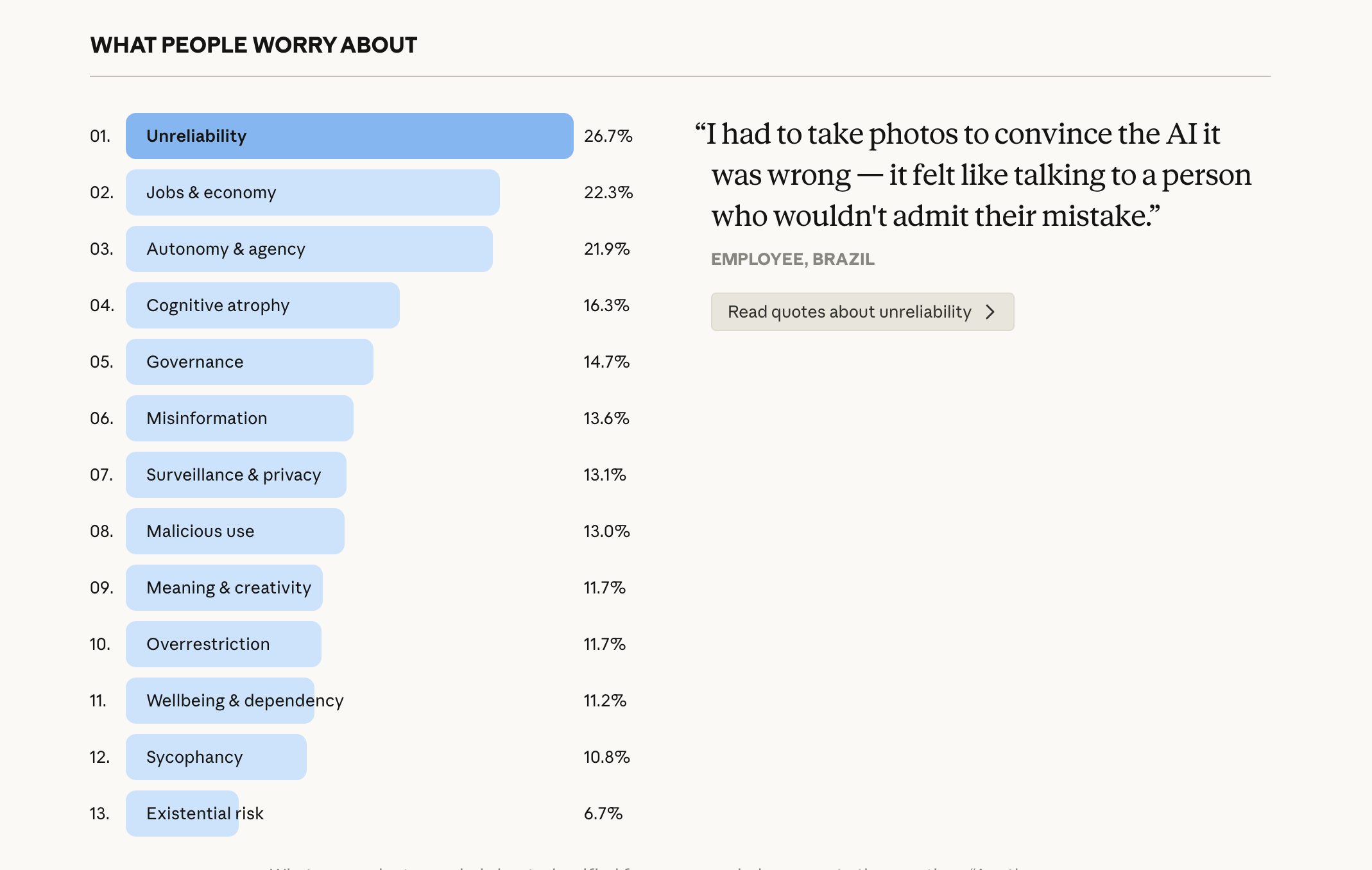

The most common fear is not “AI takes over the world.” It’s that AI becomes unreliable at exactly the wrong moment.

Public AI debates often drift to dramatic long-term fears. But the top concern in this study was much more immediate: unreliability.

Users worry that AI will sound convincing while being subtly wrong. In some categories, that’s a mild annoyance. In others, it’s dangerous. Law, finance, healthcare, and government workers especially raised this concern because the cost of a confident error is high.

This is a critical insight for founders. Reliability is not a “nice to have” layer you add later. In many AI products, it is the product.

Other major concerns included:

What’s striking is how practical most of these fears are. People are not mainly debating whether AI is philosophically good or bad. They are asking whether it will make them less employable, less independent, less thoughtful, or too dependent on a system that is always available.

The real story is not optimism vs pessimism. It’s tension.

One of the best concepts in the report is what Anthropic calls the “light and shade” of AI.

The same capabilities people love are often the ones they fear. For example:

AI helps people learn faster, but they worry it may weaken their own thinking.

AI saves time, but they worry it increases expectations and speeds up the treadmill.

AI offers emotional support, but they worry it could become a substitute for human connection.

AI creates economic opportunity, but it also raises fear about displacement.

That is a much more honest frame than dividing people into “AI believers” and “AI sceptics.” Most users are both at once. They see upside and risk together.

That’s an important product lesson. Great AI products will not win simply by maximising usefulness. They’ll win by managing the tension around usefulness. The winners won’t just provide capability. They’ll create trust, boundaries, and clarity around how the product should fit into a person’s life.

The regional split is worth paying attention to

The report also found a noticeable pattern across geographies.

Users in lower- and middle-income countries were generally more optimistic about AI than users in wealthier regions. In many emerging markets, AI is seen less as a threat and more as a ladder, a way to start businesses, access education, or overcome infrastructure gaps.

That matters if you’re building global products.

In richer markets, AI is often framed around life management, overload reduction, and economic anxiety. In many developing regions, it is framed more around entrepreneurship, learning, and access. Same technology, very different emotional job-to-be-done.

Founders who understand that distinction will position themselves much better across geographies.

For founders -

The strongest message from this report is that people do not just want faster outputs. They want better lives.

That sounds obvious, but it is surprisingly easy to forget when building in AI. Many teams optimise around what the model can do instead of what the user is trying to become. Anthropic’s findings suggest that the most enduring AI products will be the ones that sit at the intersection of usefulness and human aspiration.

The near-term winning categories likely look less like vague general-purpose intelligence and more like products that help people:

do meaningful work with less administrative burden

learn without fear or embarrassment

manage overloaded lives

turn curiosity into action

gain economic leverage

access systems that previously felt closed off

At the same time, founders need to respect the downside. If your product saves time but increases dependency, gives emotional support but weakens real relationships, or accelerates output while making judgment worse, users will eventually feel that tension.

That’s why this study is so useful. It reminds us that AI is not entering a vacuum. It is entering messy human lives. And the companies that win won’t just be the ones with better models. They’ll be the ones who understand what people are actually trying to protect, improve, and reclaim.

📬 Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Lauxera Capital Partners, a Paris, France- and San Francisco, CA-based growth-buyout and growth equity firm focused on Healthtech companies, closed Lauxera Growth II, at €520m. (Link)

Mouro Capital, a Madrid, Spain- London, UK- and San Francisco, CA-based venture capital firm, has secured $400m from Banco Santander for the first close of its third fund. (Link)

Veriten, a Houston, TX-based research, strategy and investment firm, held the initial close of its second flagship energy venture fund at over $105m. (Link)

Haun Ventures, a Menlo Park, CA-based venture capital firm, closed Fund II at over $1 billion. (Link)

New Startup Deals

Oorja Bio, a Houston-based clinical-stage biopharmaceutical company, raised $30M in Series A funding. (Link)

Avian, a Zurich-based industrial AI startup, raised $2.6M in Pre-Seed funding. The round was led by Founderful. (Link)

StitcherAI, a Seattle-based IT finance intelligence platform, launched with $3M in Pre-Seed funding. (Link)

Kin Health, a Los Angeles-based patient adherence platform, raised $9M in Seed funding. (Link)

Leadbay, a San Francisco-based AI prospecting platform, raised $4.3M in Seed funding. (Link)

Elliptic, a London-based digital asset decisioning company, raised $120M in Series D funding at a $670M valuation. (Link)

Xpanner, a California-based construction automation company, raised $18M in Series B bridge funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Investment Associate - Struck Capital | USA - Apply Here

Director - General Atlantic | USA - Apply Here

Investment Associate - Transition | UK - Apply Here

Visiting Engineer - AI Fund | USA - Apply Here

Associate Investor - Sky9capital | USA - Apply Here

Finance & Operations Manager - Antler | Singapore - Apply Here

Venture Fellow - Entrepreneur First | France - Apply Here

Investment Team - Antler | Germany - Apply Here

Investor (Senior Associate/Principal) - Square Peg | USA - Apply Here

Senior Analyst - ICONIQUE Capital | USA - Apply Here

Venture AI & Operations Specialist - Blum Venture | Austria - Apply Here

Program Manager - a16z | USA - Apply Here

Associate - Manhattan Venture | USA - Apply Here

VP — Finance & Compliance - Transition VC | India - Apply Here

Senior Associate - ICONIQUE CAPITAL | USA - Apply Here

Venture Capital Analyst - MicroVentures | USA - Apply Here

🤝 Partnership with us

Get your product in front of over 120,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator