Everything founders should know before signing a VC term sheet. | How to turn AI into a second brain?

When (and when not) to fight your competitors & VC-Startup Jobs.

👋 Hey, Sahil here — Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Everything founders should know before signing a VC term sheet.

How to turn AI into a second brain?

13 successful VC fund decks that raised over $500M from LPs.

Market command matrix: when (and when not) to fight your competitors.

FROM OUR PARTNER - ROCKET

🚀 Vibe Solutioning: Rocket Reinvents App Building

Rocket is a $15M-backed startup reimagining how software is built. With our vibe solutioning method, you can turn prompts or Figma designs into fully operational web or mobile apps—front-end, back-end logic, AI workflows, and deployable code.

Unlike legacy tools stuck at prototypes, Rocket supports the full lifecycle: solutioning, launching, and iterating. For founders, investors, and growth leaders who demand scalable product velocity, Rocket is the path forward.

🤝 PARTNERSHIP WITH US

Get your product in front of over 100,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

📜 DEEP DIVE

Everything founders should know before signing a VC term sheet.

Founders often ask me these questions when raising a VC round:

How long does it take to negotiate a term sheet?

Who should start the valuation discussion the VC or the founder?

What are the top tips for negotiating a term sheet?

Getting a term sheet is a step toward closing your round but it’s not money in the bank yet. Many founders don’t fully understand this and have a lot of questions like the ones above. So I’m sharing this guide to walk you through everything you need to know. After reading it, I’m confident most of your doubts about term sheets will be gone.

Let’s start with the basics what’s a term sheet?

A term sheet outlines the key terms and conditions of an investor’s offer to invest in your startup.

Once an investor has done some initial due diligence and decides they want to invest, they’ll usually send you a term sheet that looks something like this:

The term sheet includes a lot of terms that can feel overwhelming especially for first-time founders. If you search online, you’ll find plenty of articles explaining each one in depth. But to save you some time, I’ve listed the most important terms below for quick reference:

Valuation Pre-money: Company’s valuation before investment to determine equity split. Post-money: Company’s valuation including the new investment capital.

Equity Common stock: Basic shares with voting rights but low priority in a liquidation. Preferred stock: Enhanced rights like priority in liquidation, and anti-dilution protection.

Liquidation Preference: Specifies the order in which shareholders get paid if the company is sold or goes bankrupt. Investors usually get paid back before founders/employees.

Vesting Schedule: The schedule over which founders/employees earn their equity over time, e.g. 4 years with a 1-year cliff.

Anti-Dilution: Protects investors by adjusting their price per share if the company raises money at a lower valuation in the future.

Board Representation: Who gets board seats - a mix of investors, founders, and independent directors.

Exit Strategy: IPO, acquisition, or merger provisions and the required shareholder approval for each path.

Confidentiality & Exclusivity: Can’t share details. Startup can’t talk to other investors for a set period.

Drag/Tag Rights Drag: Majorities can force minorities to join a company sale. Tag: Minorities can join a sale initiated by majorities.

Milestones & Tranching: Funding tied to startups achieving certain technical, revenue or other milestones.

You can also check out this 47-page guide that dives deep into term sheet terms, if you want to explore further. At its core, a term sheet is all about alignment how founders and investors come together and agree on key terms.

Now, most founders still have a few important questions, like:

How long does it take to negotiate a term sheet?

Who should open the negotiation on valuation – VC or entrepreneur?

“It shouldn’t take more than a week, or even just a few days, to negotiate a term sheet. That is once a VC decides they truly want to do a deal. There really aren’t many variables these days for seed to Series A deals, really just price and how much you are raising/selling.

Most of the rest of the terms are much lower drama than they used to be. Most VCs aren’t trying to control your board and your company in the early days anymore. (If they do, that may take longer to work out).”

Founders also often ask me for tips on how to get the best deal one that’s not just great on paper, but also actually closes. So here are a few things you should keep in mind:

Who goes first founder or VC usually doesn’t matter in early-stage rounds. Some founders hold back, hoping to gain leverage by making a VC go first. But it’s cleaner to just ask directly: how much are you raising, and at what valuation?

Leverage doesn’t come from going first. It comes from having multiple offers, from being in demand, or simply not needing the money urgently. Running low on cash weakens your position. Having a solid alternative makes everything move faster.

Asking for too much money can push a VC out, even if they like you. Every firm has check size limits. If you’d take $3M but ask for $6M, and their cap is $3M, they may walk. Showing flexibility on round size, especially with smaller funds keeps doors open.

If you’re raising a large round, know that some VCs will tap out early. For example, any founder raising $10M or more is outside what many seed investors can do. Even if the deal is good, it’s just too big for them.

If you’ve raised more than usual for your stage, don’t hide it. Address it upfront. $2M+ before early seed, $5M+ before pre-A, $10M+ before Series A those amounts are considered high. Be ready to show that existing investors are aligned on the current round’s pricing.

If there’s a past issue like an ex-founder conflict disclose it. Don’t let it surface late in the process. The closer you get to a term sheet, the fewer surprises there should be.

Ask what ownership target the VC has. Most firms have a minimum they need to hit. In pre-seed it might be 2–7%, in Series A it’s often 15–20%. If your round doesn’t get them there, they’ll likely pass. Better to know early.

Decide in advance how you feel about giving board seats. Many VCs will ask if they’re buying 8% or more. Some won’t care, others will insist. Know your line and be upfront about it.

Confidence is good, but too much can come off as arrogance. VCs want to back ambitious founders but also ones who want a long-term partnership. If you don’t show any real interest in them, some will walk away.

If you counter a VC’s offer, listen closely to their response. Some leave wiggle room, others don’t. If you sense hesitation after you push on price, don’t keep pressing especially if it’s your top pick. VCs have internal limits, and they rarely forget when you try to push past them.

Don’t waste energy on terms that don’t move the needle. Registration rights, legal fee coverage, SAFEs vs equity these details won’t make or break the deal. Price, ownership, and control matter most. Focus there.

Time can work in your favour if you’re growing fast. You might want to close quickly, but sometimes waiting a few months can strengthen your position. Growing from $20K to $50K MRR can dramatically change investor interest.

Tight deadlines can create urgency, but overplay it, and VCS may walk. Most can move fast when needed, but if the pressure feels forced, it can backfire. Be transparent about your timeline, and give space when you can.

Make sure your existing investors are aligned and supportive. If they’re quiet, unsure, or not reinvesting, that’s a red flag. But if they’re excited and joining the next round, it becomes much easier to close new capital.

There are also proven frameworks and strategies founders can use to negotiate a term sheet the right way. If you want to go deeper, check out this 42-page guide on term sheet negotiation.

Even after successfully negotiating a term sheet, most founders forget to ask key questions I always recommend before taking a VC’s money.

These questions reveal how a fund really operates behind the scenes and can protect you from surprises later.

1. How are the GPs compensated?

At most firms, the partner who brings in the deal gets the bulk of the profits (carry). That means the rest of the partners aren’t financially motivated to help you.

But in some funds like Benchmark or Hustle Fund carry is shared equally. This structure encourages teamwork. Every partner is aligned to support you, regardless of who sourced your deal.

If you want full access to a VC firm’s network, not just one person’s help, understanding their internal incentives matters.

2. Where is the fund in its deployment cycle?

Timing can impact your ability to raise follow-on capital. If you’re one of the last investments in a fund that’s five or six years old, there may not be money left for future rounds even if you’re doing well.

Newer funds = more dry powder.

Older funds = limited reserves.

Always ask how much capital is left for follow-ons. Don’t just assume a committed investor will be able to write a second check.

3. How quickly can they wire the money?

It’s not uncommon for VCs especially newer ones to sign a term sheet before they’ve raised their own capital. That can lead to long delays before money hits your account.

Even with established funds, VCs often rely on capital calls. That means they request money from their LPs after signing a deal and if LPs delay, so does your wire.

Ask if they have funds already on hand, or if it will depend on a capital call. Nail down the expected timing. Don’t risk missing payroll waiting on a wire.

Ask these early.

These aren’t awkward questions. They show you’re thinking like a serious founder who understands risk and wants real alignment from your investors.

Before you say yes to a term sheet, make sure you’re not just getting a check — but a committed, functional partner who can deliver.

That’s it. If you have any other questions regarding the term sheet. Feel free to email or reply on this post.

📃 QUICK DIVES

How to turn AI into a second brain?

Most people use AI like a fancy autocomplete. They type a question, grab the first answer, and move on. But that only scratches the surface.

Hiten Shah shared a powerful thread recently 11 prompt structures that help you think better, uncover sharper insights, and build stronger strategies using AI.

Here’s the full breakdown:

The Chain Reaction Method

Every answer is a building block. Instead of a single question, try “Summarize this” → “Now critique it” → “Now improve it” → “Now make it actionable.” One-shot prompts give surface-level answers. Chains go deeper.

The Forced Analogy

AI connects the dots in unexpected ways. Ask “Explain this like a sports coach would”

or “Compare this to how chess players think.” Ideas become clearer when framed through a different lens. The best insights come from collisions.

The Persona Flip

AI defaults to the dominant perspective. Flip it. Try “Explain this from the viewpoint of a sceptical CFO” or “Write this as if you are a customer who just churned.” Seeing through different eyes forces clarity.

The Priority Filter

If everything is important, nothing is. Ask “Rank these in order of impact” or

“If I could only do one, which should it be?” AI helps filter out noise. The best decision-makers cut through complexity fast.

The Gap Finder

You don’t know what you don’t know. Ask “What are three questions I should be asking but haven’t?” or “What’s missing from this strategy?”

Most people focus on what’s there. The real leverage comes from what’s missing.

The Stress Test

AI defaults to clean, logical reasoning, but real-world ideas break under pressure. Try “Find three ways this could fail” or “Where would this idea collapse under real constraints?” The strongest strategies aren’t just good, they survive reality.

The Break & Build

Instead of refining an idea, destroy it and rebuild it stronger. Ask “List all the weaknesses in this” then “Now reconstruct it while fixing those flaws.”

Most people iterate by polishing. The best iterate by breaking and rebuilding.

The Extremes Approach

AI thinks in averages. Force it to think in extremes. Try “Give me the most radical version of this idea” or “Now strip it down to the absolute simplest version.”

You’ll uncover insights that never appear in the middle.

The Layered Explanation

Great ideas work at multiple levels. Try “Explain this in one sentence” → “Now in one paragraph” → “Now in a full-page breakdown.” If an idea doesn’t scale from short to deep, it isn’t truly clear yet.

The Style Shifter

A message is only as strong as how it lands. Ask “Rewrite this with more urgency” or “Make this more persuasive to an investor.” Great thinking isn’t just about what you say. It’s about saying it the right way.

The Negative Space

People focus on what’s there. The best focus is on what’s missing. Ask “What isn’t being said here?” or “What’s implied but not directly addressed?” AI can surface gaps in logic, positioning, or messaging that you wouldn’t otherwise see.

You can check out 10+ prompts here in the Google Sheet.

13 successful VC fund decks that raised over $500M from LPs.

Raising money is tough for both founders and VCs, but it’s even harder for VCs. They must persuade limited partners (LPs) to invest in their venture capital funds.

I’ve analyzed how successful VCs craft pitch decks that help them raise massive amounts of capital. Here’s what I learned.

Think of fund managers as salespeople. Their pitch deck (or memo) is their most powerful sales tool. It needs to do two things really well: hook LPs enough to get that crucial first meeting, and serve as a compelling narrative during and after the pitch.

Here are four main takeaways to consider when creating a deck for LPs:

The purpose of your pitch deck is to convince LPs of your ability to make outlier investments. Show how you access, make sound decisions on, and win exceptional deals.

Your pitch deck should tell a clear, concise, and convincing version of your fund’s story.

Show, don’t tell, using examples, numbers, and visuals to add credibility.

Let others speak to your strengths with quotes from founders, testimonials from references, and committed LPs to establish social credibility.

But what Goes Into a $500M+ Fund Deck? Here’s the winning structure I’ve seen work:

Title: So, what’s this fund called? Which fund is it?

Team: Who is the GP? Who else is on the team?

Access: How do you get access to high-quality investment opportunities? What’s your advantage?

Ability to win: How will you win competitive deals? What’s your value-add to founders?

Investment Focus: What are you investing in? Why? Do you have a unique insight into that focus?

Track record: Do you have investment experience? What’s your past track record? What are your most impressive investments?

Fund structure: What’s the size of the fund, the stage you’re investing in, the number of expected investments, and other details on the fund structure?

Network: Who’s in your orbit? Which founders, investors, and others do you collaborate with and can you show examples?

Appendix: Additional materials that might be useful to include

You can access all 13 VC fund decks here.

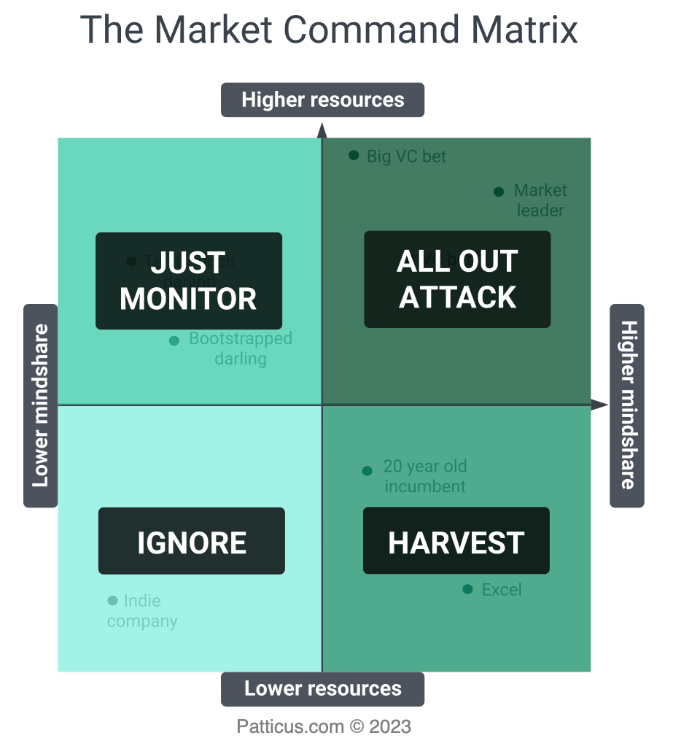

Market command matrix: when (and when not) to fight your competitors.

Patrick Campbell sold his startup, Profitwell, for $200 million last year — and it was entirely bootstrapped.

Since then, he’s started sharing a lot of primary research he’s commissioned into topics where there isn’t a lot of ground truth data on. Most recently, he shared his competitive research playbook and shared this framework — the market command matrix:

The y-axis represents how much of a competitor’s resources they’re piling into your market, and the x-axis represents how aware customers in your market are of the competitor.

The big text in each quadrant is what you should do in response. While the placements on the matrix aren’t exact (for example, a “big VC bet” could have dramatically more or less mindshare depending on what stage they’re in), Patrick’s recommendations are good.

Note that he only recommends you take action against the two quadrants on the right — the competitors who your target and/or existing customers are likely to be aware of.

Another note: “all-out attack” may mean exploring partnerships when you both have leverage in different parts of the market — it doesn’t mean burning all your money on paid ads.

He also includes free playbooks on how to handle competitors in each quadrant — the full article is worth a read.

TODAY’S JOB OPPORTUNITIES

💼 Venture Capital & Startup Jobs

2026 Venture Capital Summer Analyst - Stepstone Group | USA - Apply Here

Business Development & Fundraising Analyst/Associate - VNV | India - Apply Here

AI Venture Analyst Intern - Untaped Venture | USA - Apply Here

Investment Analyst Interns- AI & Consumer Markets - Titan Capital | India - Apply Here

Investor Relations Manager - Beco Capital | UK - Apply Here

Associate - Venture Capital - Artha Venture Fund | India - Apply Here

Executive Assistant - AN Venture Partner | USA - Apply Here

Senior Associate - M12 | USA - Apply Here

Analyst - Urban Partners | London - Apply Here

Investor Relations - Samved VC | India - Apply Here

Interim Senior Analyst, Investments - Pivotal Ventures | USA - Apply Here

Trade Operations Lead - Manhattan Venture Partner | USA - Apply Here

AI Builder In Residence - True Venture | USA - Apply Here

VP of Fundraising - Scale Asia Venture | Japan - Apply Here

🤝 Partnership With Us

Get your product in front of over 95,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

Links lead to an access error; can that be enabled pls