How big is AI spend, really? | What 180M job postings reveal about AI’s impact. | VC's turning into a network-effect business.

The state of GTM in 2025 & You should know this before signing a Shareholders Agreement.

👋 Hey, Sahil here — Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

How big is AI spend, really? Bigger than you think.

Europe’s valuation gap with the U.S. is closing, but only at scale.

VC valuations hit new highs, but investor returns are still near decade lows.

Frameworks & insightful posts :

Turning VC into a network-effect business.

The state of GTM in 2025: what founders should really pay attention to.

What founders should know before signing a Shareholders Agreement - Free template.

What 180M job postings reveal about how AI is actually changing jobs in 2025.

FROM OUR PARTNER - ROCKET

🤝 Why Rocket.new’s Precision Mode is the AI Builder We’ve Been Waiting For

We’ve tested every major AI builder. They all share the same fundamental flaw: they make you adapt to AI instead of AI adapting to you.

You learn prompt engineering. You write carefully. You retry constantly. You debug AI mistakes. That’s not building. That’s negotiating.

Rocket’s Precision Mode eliminates this entirely. Over 100 structured commands that execute exactly what you specify. “Fix mobile layout” repairs responsive issues. “Add Stripe integration” builds payment flows. “Optimize images” compresses and converts. “Update pricing table” modifies content.

No interpretation. No guessing. No retries. Just precise execution. This is what professional AI building looks like.

Try Precision Mode at rocket.new →

🤝 PARTNERSHIP WITH US

Get your product in front of over 95,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

How big is AI spend, really? Bigger than you think.

Fresh analysis comparing AI infrastructure investment to the largest capital mobilisations in U.S. history shows just how fast the AI economy is scaling and how far it still has to go.

AI vs historical megacycles:

World War II remains the biggest economic mobilisation ever at 37.8% of GDP, followed by WWI (12.3%), the New Deal (7.7%), and the railroad boom (6.0%).

AI infra spend is already at 1.6% of GDP — bigger than the entire telecom bubble at its peak (1.2%).

Corporate CAPEX is exploding:

Microsoft: $140B

Google: $92B

Meta: $71B

And OpenAI alone is reportedly planning $295B by 2030, signalling the scale of the compute arms race.

What 2030 could look like:

If OpenAI represents ~30% of total AI infra spend, the market would hit $983B annually by 2030, roughly 2.8% of U.S. GDP.

Hitting the railroad era’s 6% equivalent would require ~$2.1T per year, meaning today’s tech giants would need to 5–7x their current spend.

AI infra spending has already become one of America’s largest investment categories, and it’s only in the early innings.

While still far from the scale of wartime mobilisation, the compounding CAPEX cycle from OpenAI, Microsoft, Google, and Meta could reshape the U.S. economic landscape for the next decade.

Europe’s valuation gap with the U.S. is closing, but only at scale.

Yoram Wijngaarde’s latest analysis shows that European startups still face a 12% valuation discount compared to U.S. peers at the Series A stage. The gap reflects a persistent cost and capital availability imbalance in early-stage venture rounds.

12% early-stage discount: European Series A valuations remain roughly 12% lower than U.S. equivalents, underscoring how geography still shapes pricing in early venture deals.

Parity at $100M+ valuations: Once startups cross the $100M pre-money threshold, the gap nearly disappears — with European unicorns often priced on par with U.S. counterparts.

U.S. still dominates deal flow: Despite convergence at the top, U.S. founders capture larger and more frequent rounds, maintaining a structural edge in access to late-stage capital.

Europe’s venture ecosystem is maturing fast, but scale is the great equaliser; the valuation gap narrows only once startups break out of the early-stage orbit.

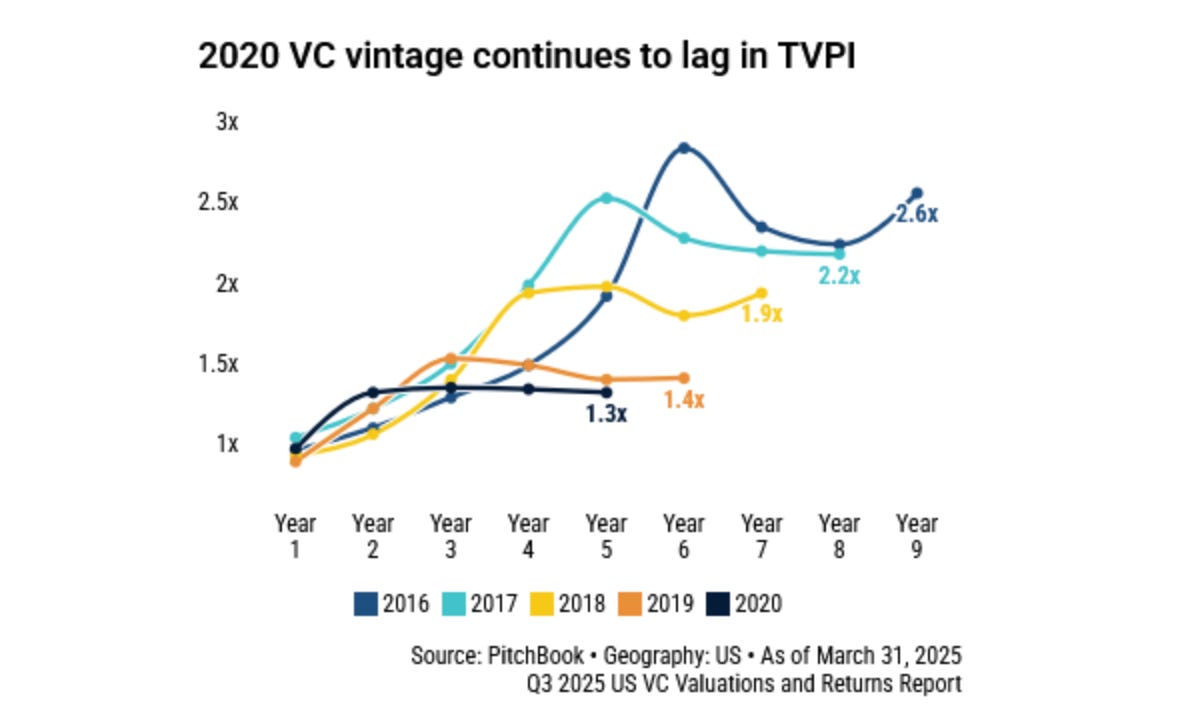

VC valuations hit new highs, but investor returns are still near decade lows.

PitchBook’s new Q3 2025 US VC Valuations & Returns Report captures one of the most uncomfortable contradictions in the market right now: Startup valuations look like 2021, but VC returns look like 2010.

Here’s what matters:

Valuations are back to peak levels

Across every stage, the median pre-money valuation is now equal to or above 2021 levels.

AI dealmaking is the biggest accelerant, but there’s a second driver: multi-stage funds are pushing aggressively into seed and Series A, bidding up prices with looser valuation discipline.

Seed valuations hit a fresh record :

Median seed pre-money valuation in Q3 2025: $13.9M, a new all-time high.

Returns tell a very different story

Despite rising valuations, VC’s rolling 1-year IRR is only 3.1%, and cash flows to LPs have been negative since 2022.

The 2020 VC vintage now has the worst TVPI after 5 years of any vintage since 2010, showing how badly late-cycle checks are struggling.

Liquidity pressure is intensifying

More unicorns have gone public in 2025 than in the prior few years, but the overall IPO count will still only match the last three years. Large-scale M&A hasn’t meaningfully rebounded either, leaving many funds dependent on 2026 outcomes to avoid prolonged underperformance.

Why valuations keep rising anyway

Dealmaking is climbing, and AI startup costs are dropping, letting founders justify richer terms. The market is effectively betting that liquidity catches up later — a narrative that has not yet materialised, but investors are hoping 2026 cracks open the exit window.

The bottom line:

VC is facing another valuation/returns disconnect. Prices are rising again, but distributions aren’t. Unless liquidity accelerates in 2026, many funds — especially those raised in the 2020–2022 boom years — will face steep pressure from LPs expecting real returns, not just paper markups.

TOOL FOR FOUNDERS

📑 Startup Legal Pack: VC-Ready Docs in One Place

Messy or missing legal docs slow founders down and turn off investors.

The Startup Legal Document Pack gives you everything you need to incorporate, protect equity, and raise confidently.

What’s inside:

Incorporation docs & founder agreements

SAFE notes, term sheets, cap tables

Employment, IP, and advisor agreements

NDAs, privacy policies & customer contracts

Built with startup attorneys and VC teams. Investor-ready. Easy to use.

SOMETHING MORE

🧩 Frameworks & insightful posts

Turning VC into a network-effect business.

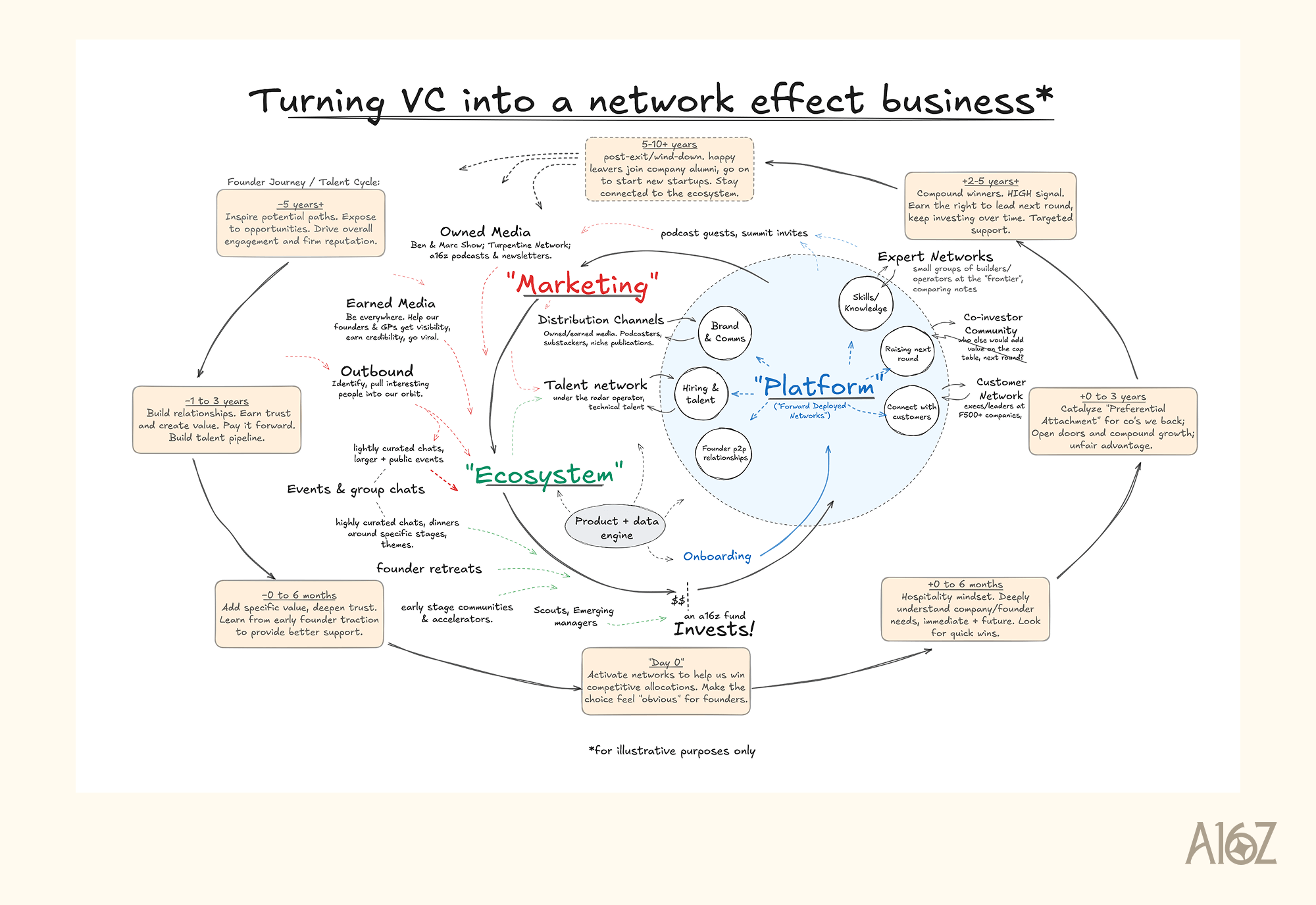

Most founders think great VCs win because they have money, brand, or a famous GP. David Booth’s insight is sharper: the next decade of VC will be dominated by firms that operate like network platforms, not service providers.

And this matters because the VC you choose directly affects how fast your startup compounds.

Why traditional VC hits a ceiling

The old model is intimacy-driven: partner time, partner intros, partner advice. But that model collapses at scale. Every new investment dilutes attention. Founders feel it immediately: fewer intros, slower help, weaker leverage.

This is why VC historically does not behave like a network-effect business.

The shift: preferential attachment

Marc Andreessen calls it the core mechanic of startup success: when you’re winning, everything starts attaching to you, talent, customers, capital, media, momentum.

VC firms themselves can harness the same mechanism. The ones that build systems, not just relationships, start compounding.

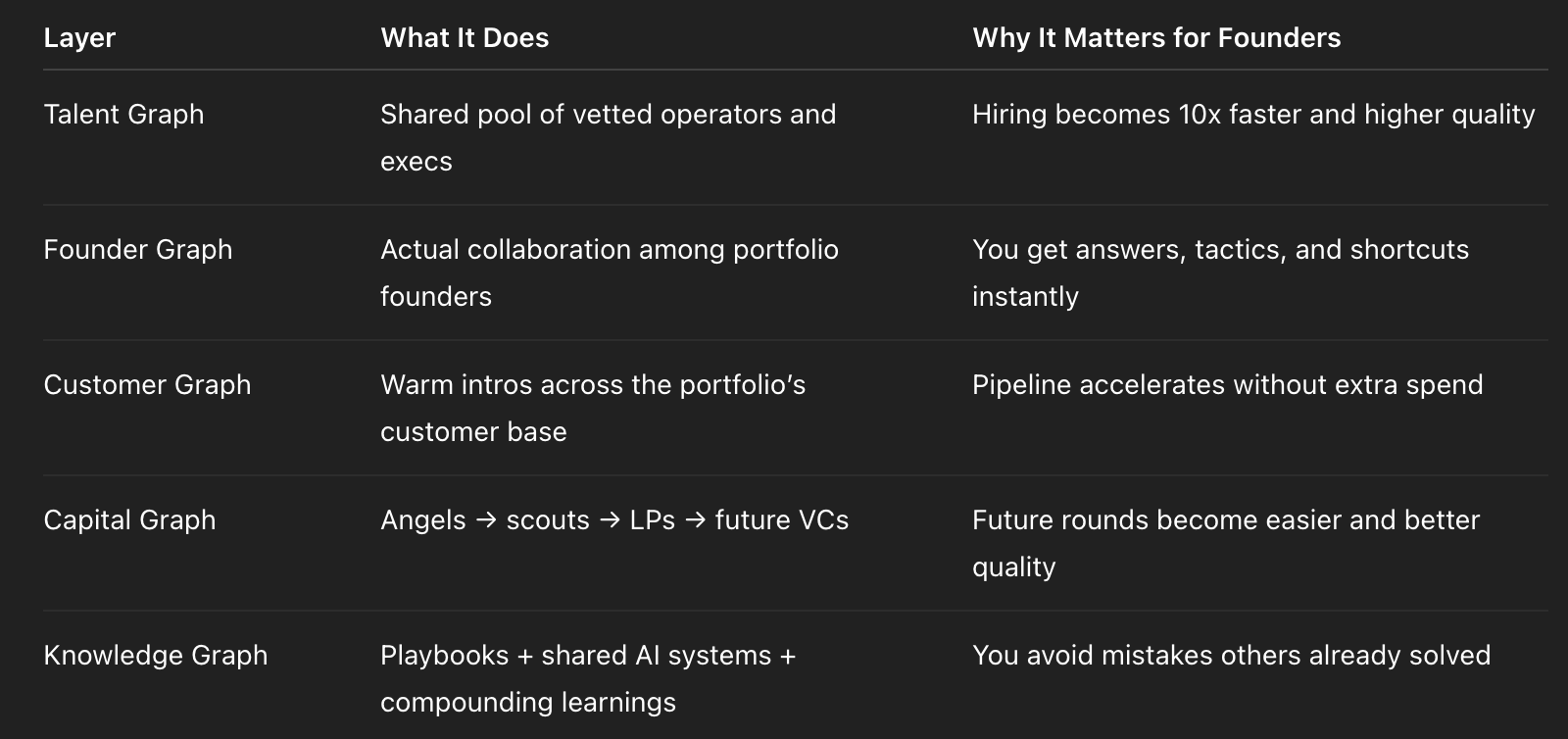

What a “network-effect VC” actually looks like

Not events. Not fancy platform decks. Not “value-add” slogans. A real networked VC looks like this:

A firm with these layers doesn’t add value linearly; it compounds with every new founder who joins.

What a16z got right (and others are now trying to copy)

They built the “pit crew” behind the GP. Yes, the partner wins the deal. Yes, the partner advises you at critical moments.

But the actual advantage comes from the invisible infrastructure:

talent pipelines continuously flowing into portfolio companies

customers and execs moving between companies

alumni founders becoming angels for new founders

internal tools, research, and distribution that everyone can access

vertical GPs + horizontal networks that multiply over time

This turns a VC firm from “GP attention divided across 40 companies” into: “A system where each company makes the next one stronger.”

Why does this matter when choosing your investor

Founders often focus on: Which GP is nice?, Who has the biggest brand?, Who writes the fastest check?

The better question is: Which firm gives me access to a network that compounds?

Look for signals like:

Do portfolio founders collaborate or live in silos?

Does talent circulate within the network naturally?

Is there real customer flow, or just promises?

Does joining this firm instantly increase your surface area of luck?

Because at seed and Series A, you don’t need capital, you need acceleration.

For founders: You’re not just raising money. You’re plugging into an operating system. A traditional VC gives you credibility. A network-effect VC gives you momentum, which is far more valuable.

The state of GTM in 2025: what founders should really pay attention to.

ICONIQ Capital just released new GTM data, and the takeaway is simple: growth isn’t broken; the motions powering growth have changed. The companies pulling ahead aren’t selling harder. They’re rebuilding GTM around AI, faster adoption, and smarter pricing.

Most founders still focus on top-of-funnel. ICONIQ’s data shows the real bottleneck is now late-stage conversion and post-sales execution. That’s where AI-native companies are opening a huge gap.

Growth is returning, but only for teams that rebuilt the funnel

ARR growth has been flat since 2023, but companies between $25M–$200M ARR are finally reaccelerating. The difference is how quickly they turn trials and POCs into paid deals.

AI-native companies are converting nearly twice as well in this stage because they prove ROI faster.

Practical signals:

Free-trial/POC conversion at $100M+ ARR: 56% for AI-native vs 32% for others

Top-quartile growth (for $25M–$100M ARR): up from 78% → 93%

Quota attainment is flat, meaning the market hasn’t fully recovered — but conversion winners are still growing

The new GTM structure: more post-sales, fewer “classic” sales roles

ICONIQ found something important: the fastest-growing companies now look more like “adoption machines” than traditional sales orgs.

AI-native teams are shifting headcount toward:

Post-sales

Forward-deployed engineers

Technical onboarding roles

Why? Because if adoption is slow, revenue is slow. If adoption is fast, revenue compounds.

What founders should do:

If your product requires behaviour change, post-sales is now a growth function, not a support function

Forward-deployed engineers shorten time-to-value → meaning they directly increase revenue

Don’t scale AEs faster than you scale adoption capacity

Pricing is changing: hybrid models are becoming the norm

ICONIQ shows nearly one-third of companies now use hybrid pricing — especially AI-native ones. Pure subscription is becoming risky because AI cost-to-serve is unpredictable.

What’s working:

Platform fee + usage

Seat + consumption

Commit + overage

Hybrid pricing protects margin, aligns with customer value, and lets you scale AI without burning cash.

AI implementation: real efficiency only shows up when it’s deep in the workflow

Seventy percent of companies have moderate or full AI adoption, but the winners go deeper than lead gen or content automation.

High-performers use AI for:

Qualification and forecasting

Meeting intelligence and objection analysis

Research and enrichment

Faster onboarding and enablement

Result: leaner teams, faster cycles, higher conversion.

What founders often get wrong:

AI only helps if it replaces steps, not adds steps

Tool sprawl kills efficiency gains

Rollout fails when reps don’t trust the AI outputs

Focus on one: AI that removes work, not AI that creates new dashboards.

ICONIQ’s data points to three non-negotiable shifts:

Fix late-stage conversion before you pour money into the pipeline.

Shift headcount toward adoption: post-sales + forward-deployed engineering.

Move to hybrid pricing early to protect margin as AI usage scales.

Founders who rebuild GTM around these moves are already outperforming. Everyone else is trying to force 2019 playbooks into a 2025 market.

What founders should know before signing a Shareholders Agreement - Free template.

Airtree shared a solid open-source SHA template, but most early founders still underestimate what the SHA controls. This isn’t a legal formality; it’s the document that decides who has power, who gets diluted, and who wins disagreements inside your company.

Here’s the compact founder-focused version.

What the SHA really does

A SHA is the private rulebook for how your startup runs. Your default constitution is generic; the SHA lets you define how decisions actually happen, who votes, who controls the board, how shares move, and how conflicts get resolved.

Board control and decision-making

Early teams blur the lines between founders and board, but once investors come in, the SHA locks that structure. A few things it typically settles:

How directors are appointed or removed

Who gets a board seat

How many seats exist

What vote is required to change board composition

Get this wrong and you can lose control long before Series A.

Who decides what

Founders often assume they can make most decisions themselves. The SHA decides otherwise.

Generally:

Shareholders vote on big structural matters (remove directors, amend the constitution, wind up the company)

The board handles hiring, budgets, financing, issuing shares, and approving a sale

Some investors also ask for specific veto rights. Understand every veto before you sign; one line can change the power dynamic for years.

Voting thresholds

This is where many founders sleepwalk into giving minority investors blocking power.

Common thresholds:

50% for standard decisions

≥75% for major decisions

100% (unanimous) for a small set of sensitive matters

The fewer decisions that require 75% or 100%, the safer you are.

Share rules that matter most - Most real conflicts happen around new funding, exits, or someone selling shares. Three clauses determine how that plays out:

Pre-emptive rights - Existing shareholders get first right to buy new shares or buy a selling shareholder’s shares. This protects everyone from unexpected dilution, but it also slows down deals if written poorly.

Drag-along rights - If the majority wants to sell the company, the minority can be forced to sell too. It keeps an acquisition clean. The key thing for founders:

check the drag threshold. If it’s too low, you can be forced into a sale you don’t want.Tag-along rights - If majority shareholders sell, minority shareholders can join and sell on the same terms. This stops control from shifting to a stranger without everyone being protected.

Handling disputes

Good SHAs try to prevent legal battles from exploding. Usually, the process is simple:

founders + shareholders try to negotiate

If that fails, a neutral mediator steps in

Only after that can anyone take legal action

This saves time, money, and relationships.

You can also check out our Startup Legal Document Pack – Essential Legal Docs for Founders.

What 180M job postings reveal about how AI is actually changing jobs in 2025.

AI didn’t destroy the job market in 2025; it reshaped which parts of each job matter.

Henley Chiu analysed 180M job postings, the pattern is clear: roles built on execution fall, roles built on judgment and strategy hold, and AI-infrastructure roles explode.

The biggest drops came from creative execution roles.

Computer graphic artists, photographers, and writers are down 25–33%. These are the jobs where AI can now produce “good enough” output instantly. But the creative roles that involve taste, decision-making, client navigation, and strategy are holding steady, with creative directors, designers, and PM-led creative work.

The same split appears everywhere: AI compresses the bottom of the ladder but pulls the top upward.

Other declines have nothing to do with AI.

Corporate compliance, ESG, and sustainability roles fell 25–35% because the regulatory climate shifted. When the government stops enforcing rules, companies stop staffing for them. Sometimes AI isn’t the culprit, politics is.

Medical scribes may be an early real AI displacement story.

Scribe postings fell 20%, while medical coders and assistants stayed flat. With AI tools that automatically generate clinical notes from doctor–patient conversations, documentation-heavy roles are becoming vulnerable. It’s not conclusive yet — but the trend is worth watching.

The biggest growth is in the AI infrastructure stack:

Machine Learning Engineers: +40% (fastest-growing job title)

Robotics engineers: +11%

Research scientists: +11%

Data centre engineers: +9%

AI isn’t replacing tech jobs; it’s creating a whole new supply chain around training, running, and scaling models.

Leadership hiring stayed surprisingly strong.

Overall, job postings dropped 8%, but directors, VPs, and C-suite roles dropped only ~2%. Middle managers fell more, and IC roles fell the most. Senior leaders who can use AI to prototype ideas, validate technical decisions, or run analysis simply need fewer layers under them.

Marketing split in two.

Influencer marketers grew 18% — one of the few bright spots. With AI flooding the internet with generic content, people trust creators more than brands. Traditional marketing roles stayed flat or dipped slightly.

Engineering jobs were far more resilient than the hype suggested.

Most engineering roles were flat or growing. AI coding tools are amplifying engineers, not replacing them. The one soft spot: frontend roles — likely because no-code/AI builders now handle simple UI work extremely well.

Customer support survived the AI wave.

Customer service reps dropped just 4%, far better than expected. Companies tried replacing support with AI… and quickly realized angry customers don’t like arguing with bots. Human empathy still wins.

Sales roles were mixed, but one role surged: Director of Revenue (+10%).

Companies want people who understand pricing, churn, expansion, PLG, and how AI changes the revenue engine. And behind the scenes, a new role — “GTM engineer” — grew more than 200% (small base), driven by AI-powered ops work.

The pattern across all categories is the same.

AI kills repetitive execution.

AI boosts people who make decisions.

And AI creates entirely new industries around itself.

EXPLORE MORE

💡 Reports, Articles and a few interesting stuffs

2700+ US angel investors & VC firms contact database (Email + LinkedIn Link).

40 real startup pitch decks that raised $350M+ (Including leading startups’ decks).

What investors ask and how to answer: A practical Q&A prep kit for founders.

LPs are still focused on distributions, but VC continues to disappoint.

Do things that don’t scale - Fireflies AI founder story.

A Claude prompt can validate any SaaS idea in 10 minutes.

How Publer went from $0 to $3M ARR and almost died (twice) along the way.

The best time to invest in a company is when it’s most in violation of a popular narrative.

Investor data room superpack: Everything you need to build a VC-ready data room (Guide/Templates).

How fundraising size influences unicorn odds (Stanford GSB research).

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Glasswing Ventures, a Boston, MA-based VC firm focused on AI-native and Frontier Technology startups, closed its Fund III at over $200m. (Link)

359 Capital, formerly known as Sapphire Sport, is a New York-based venture firm focused on sports, media, and entertainment, and has officially spun out from Sapphire Ventures, managing $300M in assets.(Link)

Forbion, a Naarden, The Netherlands-based life sciences venture capital firm, closed its Forbion BioEconomy Fund I, at €200m. (Link)

New Startup Deals

EVE, a San Francisco, CA-based inbox revenue engine for B2B small businesses, raised $2M in pre-seed funding. (Link)

AirOps, a NYC-based provider of a content engineering platform for AI search, raised $40M in Series B funding. (Link)

1mind, a San Francisco, CA-based AI-led growth (AILG) company, launched with $40m in total funding. (Link)

Spectral Compute, a London, UK-based company behind SCALE, a software framework that enables CUDA, raised $6M in funding. (Link)

Aily Labs, the NYC-based creator an AI-native decision intelligence platform for global enterprises, raised $80M in funding. (Link)

Graymatter Labs, a Chicago, IL-based consumer mental wellness company, raised $1.3M in Seed funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Senior Principal - Newsbreak Venture | USA - Apply Here

Investment Analyst - Cornell University | USA - Apply Here

Associate - Venture Capital - Artha Venture Fund | India - Apply Here

Investment Team - WEH Venture | India - Apply Here

Venture Scout - First momentum Venture | Remote - Apply Here

Analyst / Associate - Core Innovation Capital | USA - Apply Here

Program Associate - Plug and Play tech Center | USA - Apply Here

Executive Assistant - AN Venture Partner | USA - Apply Here

Visiting Investment Analyst - Join Capital | USA - Apply Here

AI Tech Lead - Core Innovation Capital | USA - Apply Here

Investment Analyst - Caanan | USA - Apply Here

Venture capital Fellowship for PhDs - Contrarian Venture | USA - Apply Here

VC Associate UK - Breega | UK - Apply Here

Analyst - Investments - Blackhill Fund | India - Apply Here

Partner 16, Deal Operations - a16z | USA - Apply Here

PARTNERSHIP WITH US

Get your product in front of over 95,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

very insightful!