How founders should think about runway: A guide from Sequoia Capital. | Is software about to shrink or expand 10x?

How much should a founder pay themselves: from seed to series A companies.

👋 Hey, Sahil here - Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

How founders should think about runway: A guide from Sequoia Capital.

Is software about to shrink or expand 10x? Redpoint’s data reveals the truth.

How much should a founder pay themselves in 2026?

FROM OUR PARTNER - WEB3 ENABLER

🧩 Investors are backing a Web3 infrastructure layer built for 150,000+ enterprise companies

Most enterprises still run on financial systems built 40-50 years ago. Payments are slow, expensive, and disconnected across borders. Poor exchange rates at the banks make international payments cost 5% or more in hidden fees. Stablecoins cut that to 0.5% or less.

Web3 Enabler is changing that by bringing blockchain directly into enterprise software like Salesforce. Instead of forcing companies to learn crypto or adopt new tools, it integrates wallets, payments, and on-chain data inside systems they already use.

This means a company can start sending global payments or managing digital assets without leaving its existing workflow. Web3 Enabler is selling to companies that are accustomed to paying for software to solve their problems.

Why investors are paying attention:

Only a Web3 platform native to Salesforce AppExchange

Access to 150,000+ companies, including 91% of Fortune 500

Early traction with players like Circle and Ripple

Web3 Enabler is building the bridge between legacy finance and blockchain, right inside enterprise systems. This is your chance to be early.

VENTURE CURATORS’ FINDING

📬 My Favourite Finds

Media Posts:

How I scale wrap to $500k active developers. (Link)

This prompt can replace a full research team. (Link)

How founders are getting better with storytelling. (Link)

Startup legal document pack - essential legal Docs for founders. (Link)

30 tactics working right now to improve free-to-play conversion rates. (Link)

What investors ask and how to answer: A practical Q&A prep kit for founders. (Link)

Bootstrapping an AI Agent Business to $9M ARR. (Link)

Google has been releasing a bunch of free AI tools outside of the main Gemini app. Most are buried in Google Labs. (Link)

Reports/Articles:

How to build a pMF machine by a16z. (Link)

There are two paths left for software companies. (Link)

The engineering manager. (Link)

Why are executives enamoured with AI, but ICs aren’t? (Link)

What is GTM as a product? (Link)

Deedy Das visually clusters what VCs are investing in right now (Link)

PARTNERSHIP WITH US

🤝 Get your brand in front of 116,000+ audience.

Our newsletter is read by 116,000+ tech professionals, founders, investors (VCs / Angel Investors) and managers around the world. Get in touch today.

📜 DEEP DIVE

How founders should think about runway: A guide from Sequoia Capital.

Founders often view runway as just a number or equation, but VCs expect them to think beyond that. Sequoia Capital shared a framework on how founders should approach the runway. In this write-up, we will discuss...

Runway Reality

What is your runway right now? How should you calculate it?

How should you think about how much runway you need?

How do you extend your runway if you need more?

Let’s deep dive into this….

The basics: What is a runway?

It’s your cash balance divided by your monthly burn.

If you have $10M in cash and $0.5M in burn, you have 20 months of runway

But it gets a little more nuanced than that. The cleanest way to look at your cash balance is net cash, which is the cash you have on your balance sheet minus any debt you’ve drawn.

If you have $10M in cash but you’ve drawn $5M in venture debt, you really have $5M of net cash and you should use that number to think about your runway.

But why? The reason is that debt is borrowed money. It’s not yours. You owe it to a creditor. Similar to how you make personal budget decisions based on your assets minus whatever debt you owe, you should think about your company’s cash position the same way.

The TLDR is that having a line is a helpful lifeline when you’re facing a cash crunch, but drawing it comes at a cost. It makes it harder to raise your next round. It comes with covenants which means debt holders can own more and more of your company. It can be a negative signal, and it can generate a lot of overhangs.

That said, one of our recommendations, if you are tight on cash, is to secure a venture debt line and just not to consider it part of your runway. Ideally, you don’t draw on it unless absolutely necessary, with eyes wide open to the tradeoffs

Monthly burn—this is different from your net income.

Net income is an accounting concept. Burn is cash in minus cash out.

It takes into account things that aren’t in your monthly P&L: for example, if you have to buy inventory upfront, or if you have capex outlays upfront, or for a subscription company if you collect upfront on yearly contracts—all of these things impact your cash burn. It’s critical to have a very tight grip on what your cash burn is. There may be ways to reduce the gap between EBIT and free cash flow—maybe that means paying your suppliers a little later or collecting revenue earlier.

If you have a lumpy business, meaning you have to provide cash upfront to build out capital expenditures or you’re purchasing inventory, it’s existentially important to have a very detailed understanding of your expected cash outlays. If you’re not careful in managing and forecasting these outlier expenses, then your runway can turn out to be 3 months when you thought it was 15.

One more thing: Runway is not static.

Just because you have 8 years of runway doesn’t mean you can forget about it and assume you’re fine. As your revenue and expense base change, your runway can change very quickly. You want to stay focused on the burn number.

You should be calculating your runway every single month and watching that number religiously.

A Mental Framework For Founders - Runway and Milestone

If you are reading this newsletter, previously I have mentioned “You are raising fund not to increase your runway, but to achieve your milestone”

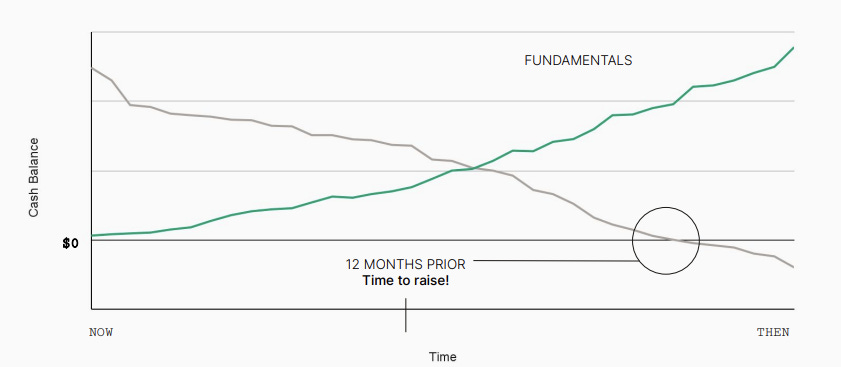

As a founder, how should you look at this graph? Suppose you and your CFO put your heads together, and your best guess for how cash changes over time looks something like this chart.

This is your cash-out point. 12 months before that, it’s time to think about raising again.

Runway doesn’t come in a vacuum. It’s intimately tied to meeting valuation milestones.

Imagine you’re driving your car on the freeway and running out of gas. What matters is not how many gallons of gas you have in your car, but whether it’s going to last you until you reach the next gas station. Think about what your goal is for your next fundraising. Maybe it’s an up round. Maybe it’s a flat round. Maybe it’s a down round. Maybe it’s to reach a cash flow positive.

Whatever your goal is, which is a conversation between the leadership team and the board, there is some valuation milestone attached to achieving that goal. Figure out what metrics or “fundamentals” get you to your goal. Maybe it’s ARR. Maybe it’s Gross Profit. This is the green line on this chart.

The rough mental framework is that well before you run out of cash, you need to make sure you have the fundamentals in order to meet your next valuation milestone.

These two lines are intertwined (Previous image). There’s a delicate balance in your scenario analysis between investing in growth and burning cash in order to make sure that you are leaving enough runway to meet the next milestone.

It’s important to hope for the best but plan for the worst as you are plotting out how to make the math work.

Raising your next round on pure story is not enough anymore.

That worked when the capital was plenty, but investors are now going to care about your metrics, and more importantly your financials. So it’s important to make sure that you are focused on getting that valuation milestone to the right place.

Now, you’ve done the exercise of figuring out your runway versus your metrics and valuation fundamentals. There are three possible scenarios for your runway situation:

Bucket 1: <12 months of runway, when it is existential to focus on your runway

Bucket 2: 12 months of the runway but not enough to raise a flat round based on rational metrics: Here it’s critically important to focus on the runway.

Bucket 3: Enough runway to raise a flat round, up round or reach cash flow positive: Stay the course and continuously optimize.

Some founders are in Bucket 1. A few are in Bucket 3. But many are in Bucket 2. If we can emphasize one point in this writeup it’s this: many founders may think they’re in Bucket 3 but are actually in Bucket 2.

The financials that you have to reach to cover your next round have changed. The bar has been raised. Many of us are 3-4 years away from reaching our last valuation, with less than that amount of cash. In that case, it’s critically important to focus on managing the runway, even if you have years of runway remaining.

So - how to extend your runway?

If you take us at our word that all probably need more runway than thought, the question is: How do you get it?

Like many things in business, it’s very easy to say and it’s very hard to do.

The first step in getting very tactical is to understand your current state.

This means looking deeply into your P&L. If you’re talking about runway, that means you’re losing money every month. So you have to figure out where the net loss comes from. Once you’ve identified the specific places in your P&L causing your burn, you can start thinking about which dollars yield efficient growth and which are not as helpful

To understand which parts of your P&L need to be addressed, begin with the big picture and break it down into parts. Starting with net loss, you can break that into two parts: gross margin and opex.

Then break each of those down into component parts: ○ What are all the drivers of your gross margin? What is the cost of sales, etc? ○ What are all the drivers of compensation opex and non-compensation opex? How much of the opex is dedicated to computer hardware, hosting and subscriptions, etc? ● Keep breaking it down until you have a detailed view of the components that contribute to total net loss.

Once you’ve identified the important contributions to your burn, you can plot them in terms of their burn impact on the y-axis. Then there’s the ease of execution:

how easy is it to address and how big an impact does it have? Unfortunately, you’re not likely to find many items that are high-impact and easy to execute. Changes that extend your runway a lot will almost certainly be difficult. This plot is important because it will set your roadmap for the actions you take to extend your runway

Once you understand the levers available to impact the runway, you can use them to set a goal. Your goal should be oriented around how long it’s going to take for you to reach a rational milestone. Let’s say your goal is a flat round. Given the market conditions, for many of us that’s going to take us three years.

To unpack why that is:

Say you hypothetically raised your last round at a billion dollars, and you have five to 10 million of ARR.

if you want to raise your next round at a billion dollars, you might need 75 to 100 million of ARR, which might mean you need to grow about 10 to 15X.

It takes time to do that. It very well might take three or four years

If it takes three years, recommend you have four years of runway. The reason: as mentioned earlier, you want to raise 12 months before running out of money. Generally, investors view it as a bad sign to have a very short runway, so you want to avoid being in this situation when raising a round. So the time you need to hit your goal plus 12 months is the ideal runway that would suggest.

One recommendation: When you decide how long it will take to reach your goal, be very realistic. Use public comps and ask the toughest board member. Ask her what it will take to reach a flat round based on rational milestones, and then add 12 months.

So now you’ve taken the steps to understand where you are, and you’ve broken down your P&L to understand where the money goes. You’ve plotted your options in terms of ease-to-execute versus burn impact. And you’ve set a goal based on rational milestones.

So let’s say hypothetically you need to cut your burn from $3 million a month to $2 million. We don’t want to sugarcoat this: It’s going to be hard. Of course, a people-related cut is the hardest decision any leader makes. Beyond this, you may face many challenging and nuanced decisions:

If you’re a global company, you might need to reevaluate certain markets.

If you’re a company that’s relied on a marketing or sales investment in order to grow, you might have to reevaluate your strategy.

You might have to increase pricing. This is scary, especially if you don’t have time to fully test the value proposition.

The big thing to remember is this: If you take the steps necessary to extend your runway in line with rational milestones, confident you and your whole company will be better on the other side.

So Overall :

You likely need more runway than you think.

Ultimately, your next round will be based on your metrics, which is going to be reflected in your financials.

Be real about what bucket you’re in. Think most companies are in Bucket 2, which is more than 12 months of cash, but need to make some changes.

You have what you need to win. You can execute and we’re here to help you do that

📃 QUICK DIVES

Is software about to shrink or expand 10x? Redpoint’s data reveals the truth.

Every time markets pull back, the same comparison shows up - “this looks like 1999 again.”

Redpoint Venture recently broke this down in their 2026 market update, and the data tells a very different story. What we’re seeing isn’t speculative excess running ahead of reality. Its demand is pulling the entire ecosystem forward.

In the dotcom era, infrastructure was massively overbuilt with almost no usage. Today, it’s the opposite.

OpenAI and Anthropic are already doing $20B+ ARR

90%+ of new data centre capacity is pre-committed before it’s even built

ChatGPT reached ~1B users in ~4 years (the internet took a similar time to reach just ~70M)

The constraint today isn’t demand - it’s supply. Power, land, and compute are limiting how fast infrastructure can scale. That’s a fundamentally different setup from 2000.

But the more important shift isn’t infrastructure - it’s what AI is doing to the software market itself.

Until recently, most AI products lived in “copilot mode” - they helped people do their jobs better. That meant they competed for existing software budgets.

Now we’re moving into something bigger: agents that actually do the work.

Software market today → ~$0.5T

With task-level agents → expands to ~$1.2T

Fully autonomous systems → could tap into ~$6T+ knowledge worker labor

This is where things change. AI stops being a feature and becomes a substitute for labour.

And that shift is already showing up in how software companies are being valued.

The selloff in software isn’t random - it’s selective.

Vertical SaaS is holding up → strong data moats, embedded workflows

Infrastructure is stable → AI increases demand for compute, storage, observability

Horizontal SaaS is down ~35% → most exposed to AI disruption

The pattern is clear. Products that own data + workflows survive. Products that mainly coordinate tasks are at risk - because coordination is something AI does natively.

This is also visible from buyer behaviour. CIOs aren’t increasing budgets. They’re reallocating.

45% of AI spend is coming from existing software budgets

54% of companies are consolidating vendors

Only 3% expect to add more tools

So the pressure isn’t just competition - it’s replacement.

Categories like sales automation, customer support, and IT management are the most exposed - not randomly, but because AI can directly do the job, not just assist it.

At the same time, incumbents aren’t out yet.

More than half of buyers still prefer to add AI to existing vendors rather than switch. But that creates a different challenge: these companies don’t just need to ship features - they need to rebuild themselves.

And that’s where most will struggle.

AI-native companies are built differently:

They rely on first-principles thinkers, not “pattern-matching” operators

Product development starts from capability (what models can do), not just customer requests

The entire org is structured around speed and iteration

This isn’t a feature upgrade. It’s a re-founding. Finally, one subtle but important insight from the data:

Private AI companies look expensive - until you adjust for growth.

Private growth-stage companies → ~61x ARR

Public comps → ~9.7x ARR

But growth rates flip the story:

Private → ~640% growth

Public → ~29% growth

On a growth-adjusted basis, private companies are actually cheaper per unit of growth.

The takeaway here isn’t just about markets - it’s about timing.

Historically, the biggest companies in every tech wave were founded around years 4–5 of the shift. We’re now in year 4 of the AI cycle.

That window is open - but it’s also the most competitive it’s ever been.

Which makes this moment unusual: It’s not a bubble driven by hype. It’s a market being reshaped in real time, where demand is real, stakes are higher, and the bar to win is significantly tougher.

How much should a founder pay themselves in 2026?

Founder compensation is one of the most misunderstood topics in startups.

From the outside, people assume founders of venture-backed companies are paying themselves massive salaries. In reality, most founders keep salaries relatively modest because the real upside comes from equity, not salary.

A new report analysing (Creandum) compensation across hundreds of startups (from bootstrapped to Series D) shows a clear pattern:

Founder salaries increase steadily with stage, but the biggest payoff still comes from ownership.

Founder salaries grow with the company stage

Founder compensation tends to scale alongside funding and company maturity.

Median salaries increase consistently as companies raise larger rounds:

Seed founders: ~€89K median salary

Series A founders: ~€154K

Series B founders: ~€199K

Series C founders: ~€225K

Bonuses also become more common as companies scale. By Series C, around 70% of founders receive bonuses, reflecting more structured compensation systems.

Interestingly, Pre-Seed salaries actually declined about 12% year-over-year, suggesting early founders are conserving cash and extending runway rather than paying themselves more.

Another surprising data point: bootstrapped founders sometimes earn more than Pre-Seed founders. Many profitable bootstrapped companies generate enough revenue to support higher salaries even without outside capital.

The biggest salary gap is in geography

Where a founder builds matters a lot.

US founders earn significantly more than their European peers.

On average:

US founder salaries are about 1.5× higher than European founders

Companies that raised €100M+ pay ~€225K in Europe vs ~$350K in the US

The difference reflects several factors:

larger funding rounds

the higher cost of living

stronger venture competition for talent

Even within Europe, there are interesting regional differences. Baltic and Nordic founders reported surprisingly strong compensation levels, sometimes surpassing those in more traditional tech hubs.

AI founders are not the highest paid

Given the massive funding flowing into AI startups, many people assume AI founders are earning the most.

The data says otherwise.

Median founder salaries by sector:

FinTech: ~€142K

CleanTech: ~€142K

AI-native startups: ~€122K

Two structural reasons explain this.

FinTech companies often monetise quickly, allowing founders to justify higher compensation earlier.

CleanTech companies tend to have long development cycles, so higher salaries help compensate founders during the long journey to profitability.

AI startups, despite the headlines, still vary widely in funding size and maturity, meaning founder compensation hasn’t yet caught up with the hype.

CEOs actually earn less than revenue-focused founders

Another interesting trend: founders responsible for revenue tend to earn more than CEOs.

Median compensation by founder role shows:

CRO / CCO founders: ~€133K

CEO founders: ~€118K

Product-focused founders: ~€85K

This reflects the current market environment.

Investors and boards are prioritising revenue generation and capital efficiency, rewarding founders who directly influence growth and sales.

The gender gap is shrinking, but representation remains low

Encouragingly, the pay gap between male and female founders is narrowing.

At Seed and Series A:

Female founders earn within 3–5% of male founders

At Series C, female founders even slightly out-earned their male peers in median compensation.

However, there’s still a major representation problem.

Only 13% of founders surveyed were women, reflecting the broader startup funding gap where:

only 2.3% of global VC funding goes to female-only teams

Equity still matters far more than salary

The biggest financial outcome for founders is still equity ownership.

And one factor dominates equity outcomes: how early you joined the company.

For example:

Founder joining at incorporation: ~48–50% ownership

Founder joining six months later: ~20–24%

That difference can translate into millions in exit value.

In other words, while salary matters for day-to-day life, the real financial impact comes from ownership and dilution over time.

How founders should think about compensation

The report suggests a practical framework for setting founder pay. Good founder compensation balances five principles:

Alignment: Most founder wealth should come from equity, not salary. Salary should support focus, not create lifestyle inflation.

Sufficiency: Pay enough to remove financial stress, but avoid draining company cash.

Transparency: Compensation decisions should be documented, benchmarked, and board-approved.

Accountability: Cash and bonuses should align with performance and operational impact.

Consistency: Founder pay should evolve predictably with company maturity, not spike suddenly after funding rounds.

Founder salaries are rising again after the startup slowdown in 2023. But the data reinforces a core truth of startups: Founders don’t get rich from a salary. They get rich from equity.

Salary keeps the lights on. Ownership is what changes your life.

QUICK HITS

🔋 Founder Fuel

Useful Data: 2700+ US angel investors & VC firms contact database (email + linkedIn link). (Link)

Trends with Benefits: Where did all the LPs go, and why is fundraising suddenly so hard for new VCs? (Link)

Founder Resource: What investors ask and how to answer : A practical Q&A prep kit for founders. (Link)

From Social: Such an Incredibly Freaking Awesome Breakdown of Different Paths to Product-Market Fit. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture Capital & Startup Jobs

Most aspiring VCs struggle with interviews, unclear expectations, no structured prep, and generic advice that doesn’t actually help. So we partnered with a leading investor group to build an all-in-one VC Interview Preparation Guide that gives you real clarity and frameworks. (Access Here)

Ventures Analyst/Associate - Plug and Play Tech Centre | USA - Apply Here

Associate/Senior Associate - Temasek Capital Management | USA - Apply Here

Research Innovation Program Director - Generator | USA - Apply Here

Investment Analyst Intern - NAV Capital | Dubai - Apply Here

Finance Associate - RA Capital | USA - Apply Here

PE & VC Partner Manager - Dealhub | UK - Apply Here

Associate / Senior Associate - Stepstone Group | Italy - Apply Here

Investment Analyst - Lunicorn Venture | UK - Apply Here

Program Manager - a16z | USA - Apply Here

Associate or Senior Associate - AI - BVP | USA - Apply Here

Venture Fellow - age1 | USA - Apply Here

Investment Associate - 500 Global | USA - Apply Here

Venture Capital Associate - Sky9 Capital | USA - Apply Here

Investment Summer Associate - AI Tooling - M13 | USA - Apply Here

Event Marketing Manager - AI Fund | USA - Apply Here

PARTNERSHIP WITH US

🤝 Get your brand in front of 116,000+ audience.

Our newsletter is read by 116,000+ of tech professionals, founders, investors (VCs / Angel Investors) and managers around the world. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

the bucket 2 trap is real. thank you for the article!

While I appreciate Sequoia's insights, I think runway discussions can be overly simplistic. It's not just about numbers; it's also about adaptability and vision. A strong founder can pivot and innovate even in tight spots. Let's not underestimate the power of creativity!