Sales funnel metrics you should track, What investors look for at seed & Homepage written for VCs or users ?

The valuation split, The rise of “seedstrapping” & Rethinking the startup MVP

👋 Hey, Sahil here — Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies. Today’s edition features even more carefully curated content.

Big idea + report of the week :

The sales funnel metrics every SaaS founder should track.

Startups are taking longer to exit — what it means for investors.

The valuation split: AI’s rise vs everyone else’s fall.

The quick test: Is your homepage written for VCs or users?

Frameworks & insightful posts :

What are investors actually evaluating at pre-seed and seed?

The rise of “seedstrapping”: A smarter fundraising strategy.

What founders should ask a potential investor?

Rethinking the startup MVP: Building a competitive product.

FROM OUR PARTNER - MECO

🤝 The best new app for newsletter reading.

Tired of messy inboxes? Meco moves your newsletters to a clean, scrollable app built for distraction-free reading.

Join 30K+ readers decluttering their inbox—connect Gmail/Outlook.

🤝 PARTNERSHIP WITH US

Get your product in front of over 95,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

The sales funnel metrics every SaaS founder should track.

If you’re building a SaaS startup, it’s easy to obsess over top-line ARR targets and forget the mechanics that actually drive those numbers. The truth is: you can only improve what you measure. And your sales funnel gives you the clearest picture of where revenue is being created — or leaking.

Here are the four funnel metrics you should track (with practical ways to apply them):

Lead volume & Lead Velocity Rate (LVR)

Track how many qualified leads you’re getting every month.

Calculate LVR = (This month’s qualified leads ÷ Last month’s qualified leads) – 1.

Example: You had 200 qualified leads in June and 250 in July. LVR = (250 ÷ 200) – 1 = 25% growth.

Pro tip: Set your LVR ~15% higher than your revenue growth target. If revenue is growing 10% MoM, your leads should grow ~25% MoM.

Conversion rates across funnel stages - Don’t just measure “leads to won deals.” Break it down:

Lead → Opportunity = (Opportunities ÷ Leads) * 100

Opportunity → Won = (Won deals ÷ Opportunities) * 100

Why it matters: If lead→opportunity is strong but opp→won is weak, the problem isn’t marketing — it’s sales performance, pricing, or product fit.Example: Out of 500 leads, 100 became opportunities (20% lead→opportunity). From those, 25 closed (25% opp→won). Overall conversion = 5%.

Sales velocity - This metric tells you how fast you’re turning pipeline into revenue:

Formula: (Leads × Deal value × Conversion rate) ÷ Sales cycle length

To speed velocity: increase lead flow, push up average deal size, improve conversion %, or shorten your sales cycle.

Example: 100 leads × $5,000 avg deal × 10% conversion ÷ 60 days = $833/day in velocity.

If you shorten the sales cycle to 45 days, velocity jumps to $1,111/day — without adding leads.

CAC & CAC payback by channel - Not all leads are equal. You need to calculate:

CAC = (Acquisition costs + Sales + Onboarding costs) ÷ New customers

CAC Payback = CAC ÷ Monthly contribution margin

Example: Channel 1 CPL = $100. You need 70 leads to land 1 customer = $7,000 CAC.

Channel 2 CPL = $200. But only 20 leads needed for 1 customer = $4,000 CAC.If your gross margin is $500/month per customer:

Channel 1 payback = $7,000 ÷ 500 = 14 months

Channel 2 payback = $4,000 ÷ 500 = 8 months

Higher CPL doesn’t always mean worse economics — look at funnel conversion + payback.

Audit your funnel this month. Pick one lever (conversion, cycle, or channel mix) to optimise, instead of blindly pushing for more top-of-funnel leads. Often, the fastest way to hit ARR targets is by fixing funnel efficiency, not by just “getting more leads. (Read detailed writeup here)

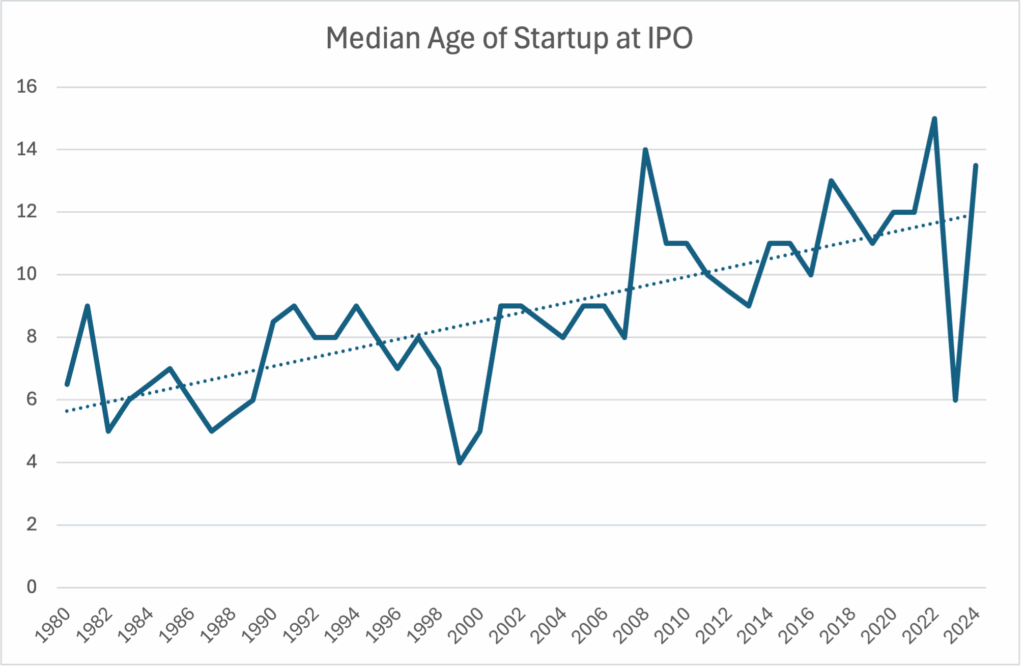

Startups are taking longer to exit — what it means for investors.

The “young and fast IPO” startup story is fading. According to University of Florida data, the median age of a company at IPO was 13.5 years in 2024, far older than the 5–9 year median from the 1980s–2000s.

Why are startups older at exit?

Private capital is abundant. With trillions flowing into private markets, companies don’t need to rush to public markets for funding.

Public company burden. Compliance, reporting, and scrutiny make IPOs less attractive.

Push for profitability. Markets expect sustainable models before rewarding IPOs.

What this means for investors:

Longer holding periods. Be prepared to wait years longer for liquidity.

Shift to later-stage. Growth and pre-IPO deals may gain more weight in portfolios.

Rise of secondary sales. More investors may seek liquidity through secondaries, though these aren’t always easy or guaranteed.

How to adapt:

Extend fund lifecycles beyond 10 years

Diversify across early and late stages

Build secondary sales into your strategy

Prioritise startups focused on capital efficiency and sustainable growth

The quick win here: If you’re investing in startups, recalibrate your expectations. The path to exit is slower, but with the right balance across stages and effective liquidity planning, you can ride this trend instead of being caught off guard by it. (Read the full breakdown here )

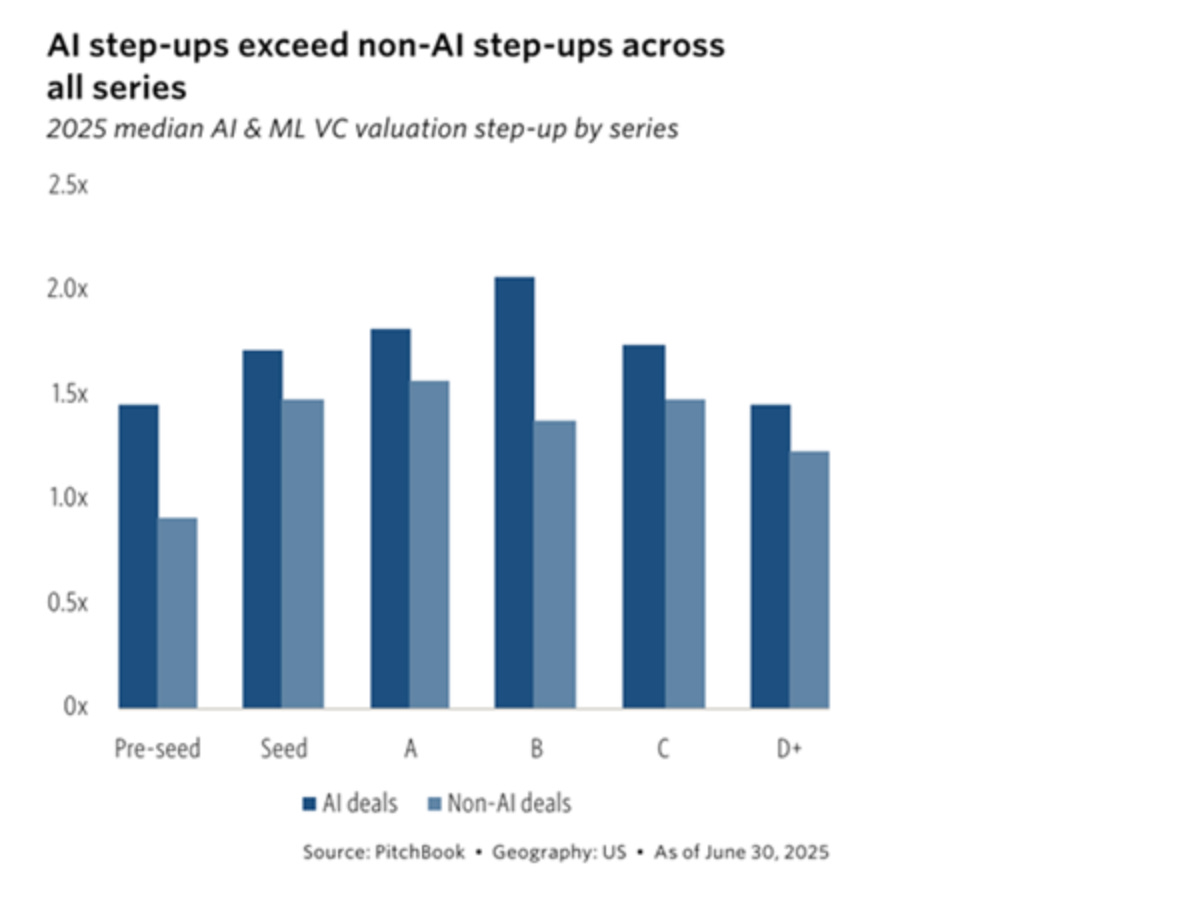

The valuation split: AI’s rise vs everyone else’s fall.

The frothy pandemic-era valuations are finally correcting. In Q2, 25% of VC rounds were flat or down, the highest share in a decade. Nearly every big IPO priced well below its last private round.

But the story isn’t uniform:

AI is the outlier. Median Series B step-up for AI startups is 2.1x, versus 1.4x for non-AI. Faster cycles, bigger checks, and resilient multiples define the sector.

Policy-linked sectors (AI, defence, fintech, crypto) are holding stronger, partly because of government tailwinds (e.g., Circle doubled on debut after progress on the GENIUS Act).

Normalisation is healthy. It frees startups from inflated markups that made new rounds or exits unrealistic, even if uncertainty still clouds public markets.

Don’t view the reset as a collapse; see it as a clearing. Strong startups now raise on cleaner terms, and AI’s premium shows where capital conviction remains strongest. (Read full report here)

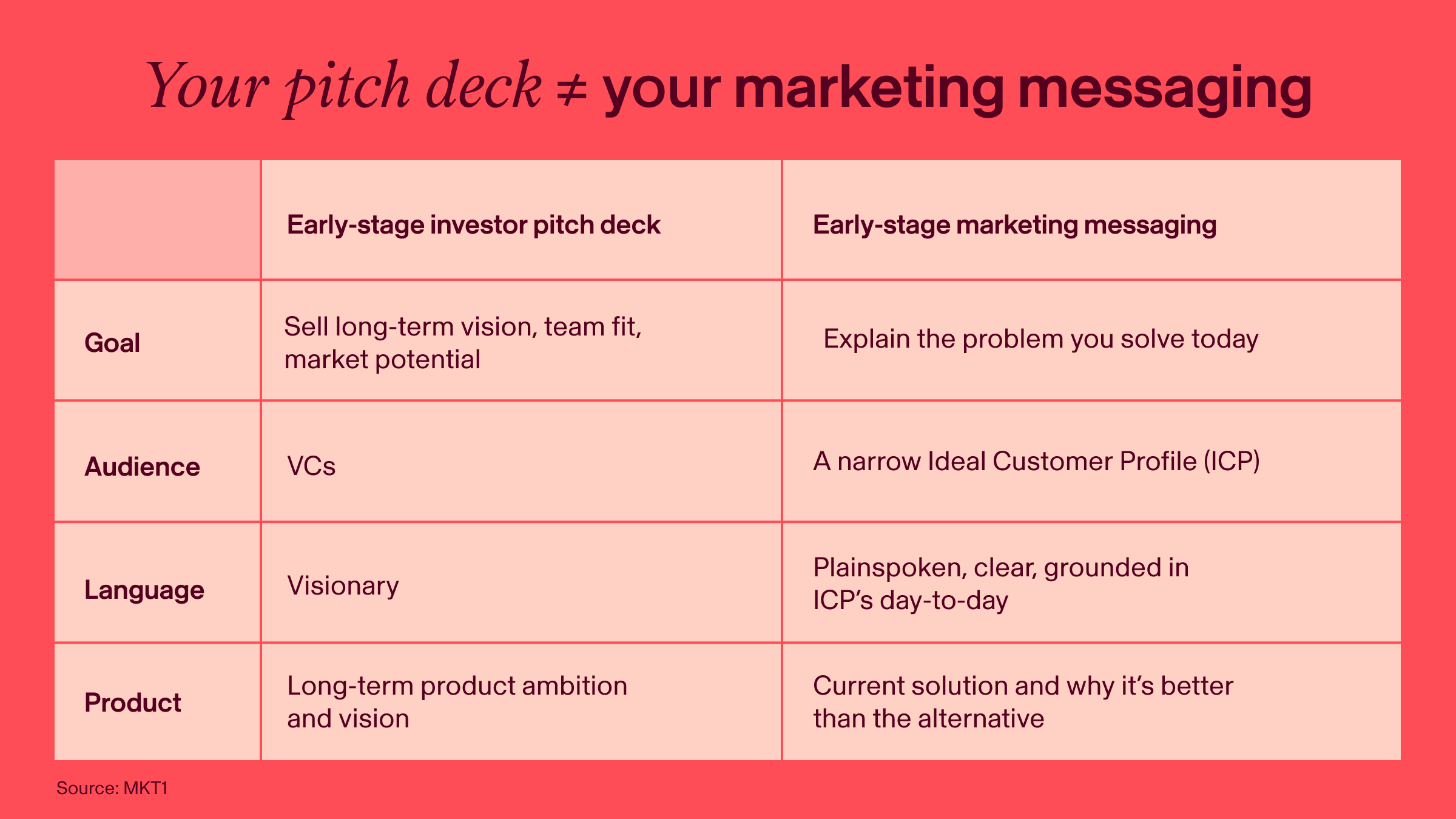

The quick test: Is your homepage written for VCs or users?

One of the most common mistakes founders make after raising their first round is copy-pasting their pitch deck into their website. But here’s the truth: investors and customers care about very different things.

Investors want the big picture — vision, TAM, defensibility, team strength.

Customers want to know one thing: “Can this product solve my problem today?”

If your homepage still sounds like your seed pitch, you’ll lose customers who just want clarity and confidence, not a roadmap of your 5-year vision.

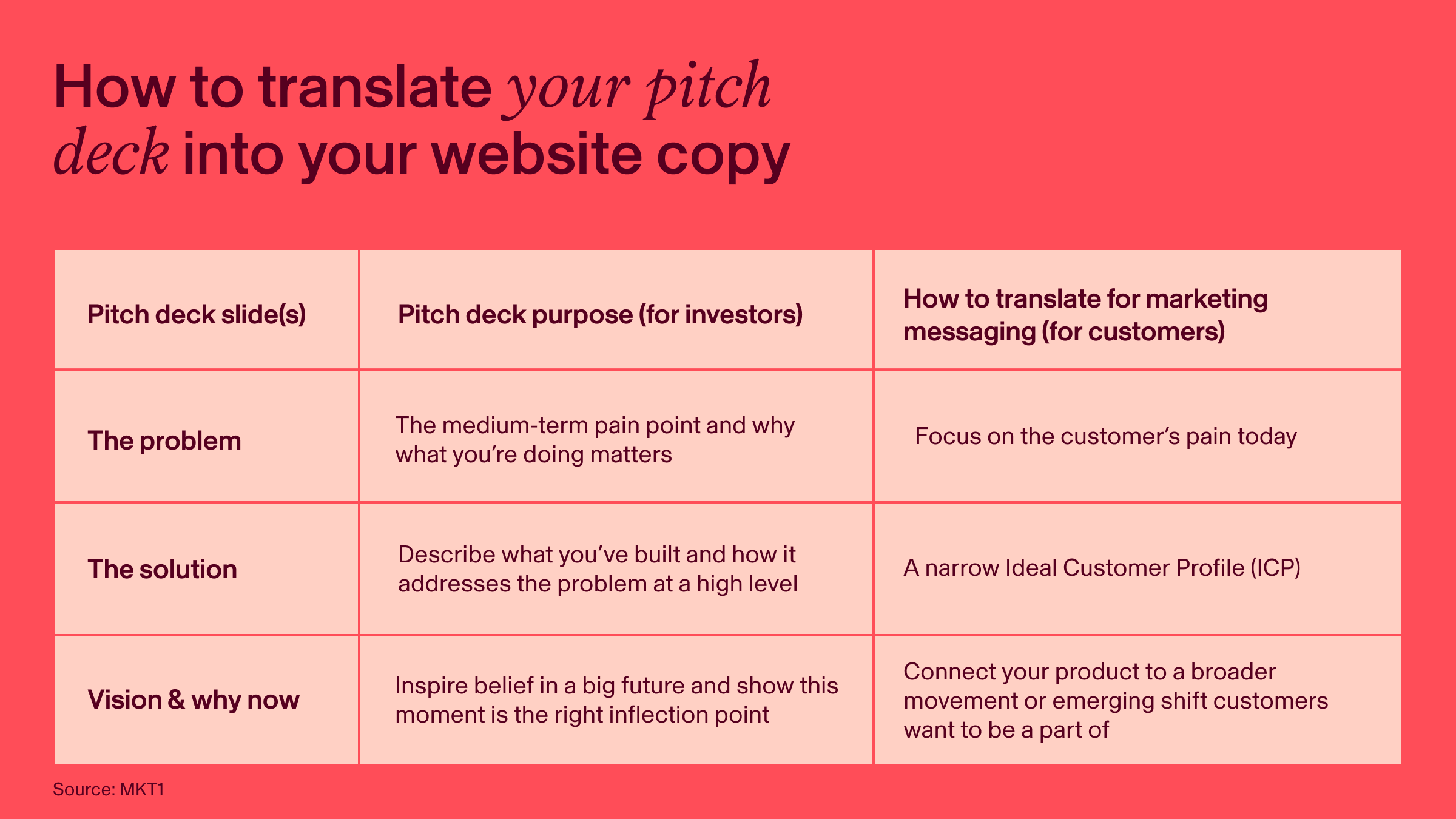

Here’s a simple framework (from Emily Kramer) to translate your pitch into customer-facing messaging:

Problem slide → Homepage hero

Don’t say: “Radiologist-read images are frequently misinterpreted.”

Do say: “Reduce diagnostic errors.”

Customers want today’s pain described in their language.Solution slide → Plain description of what your product does now

Don’t say: “Compliance and security management platform.”

Do say: “SOC 2 audit platform.”

Clarity beats cleverness every time.Market size slide → Targeted ICP callout

Don’t say: “We’re targeting remote-first and hybrid companies globally.”

Do say: “Built for early-stage remote startup teams.”

The more specific, the faster customers say, “This is for me.”Vision/Why now slide → About page, not homepage

Your website’s job isn’t to inspire belief in your billion-dollar market — it’s to show why you’re useful today. Save the big vision for your story page or founder’s note.

The quick win here? Audit your homepage. For every line of copy, ask: Is this written for a VC or a customer? If it’s VC-speak, rewrite it in your customer’s words.

Your website doesn’t need to sell the future of your category. It needs to sell the next signup.

SOMETHING MORE

🧩 Frameworks & insightful posts

What are investors actually evaluating at pre-seed and seed?

Fundraising isn’t about optics. It’s about showing investors you can figure it out. Here’s how they pattern-match across stages (shared by Amanda Zhu):

Investors aren’t scanning for perfection. They’re looking for proof you’ll figure it out.

The rise of “seedstrapping”: A smarter fundraising strategy.

Alex Lieberman (Morning Brew cofounder) recently put a spotlight on an emerging approach: raise one round of funding, then plan to never raise again. The internet calls it seedstrapping, a bad name, but a smart idea.

The playbook: raise $250k–$2m, use it to reach profitability, and keep building without relying on more VC.

Why it’s gaining traction:

The ZIRP era of unlimited capital is over—fundraising discipline is back.

GenAI is giving startups a huge efficiency boost, making profitability realistic earlier.

There was never a label for this “one-and-done” approach, until now.

Reactions are mixed. VCs like Eric Bahn and Elizabeth Yin see it as a smart path for software startups, while others argue ambition often requires more capital.

Founders, on the other hand, are fans, Josh Payne (StackCommerce) says, it gave him investor validation and networks without heavy dilution.

The bigger insight: most companies don’t become unicorns. There are 34.8M small businesses in the US, but only 30,000 hit $100M+ in revenue.

For many internet startups, one round is enough to find product-market fit, get the default alive, and build on your own terms.

This chart might be helpful to better understand various strategies:

What founders should ask a potential investor?

Founders ask me all the time what to say in a pitch. But here’s the better question: What are you asking them?

If you’re giving up equity, make them earn it. The power dynamic is broken if you’re doing all the prep and they’re just judging. Previously, we shared a write-up on questions founders should ask VCs in a fundraising meeting.

But I recently came across a post by Joseph (GP at Daring Venture), where he mentioned three questions every founder should ask a potential investor:

What does "hands-on" actually mean to you?

Everyone claims to be value-added. But does that mean weekly check-ins, midnight strategy calls, or just quarterly board meetings where they tell you what’s wrong? VCs define support very differently—know what you’re signing up for.When was the last time you backed someone who didn’t fit your pattern?

This reveals how they think. If their “example” is funding someone from Georgia Tech instead of Stanford… that’s just surface-level. Great VCs know that breakthrough ideas don’t come from cookie-cutter backgrounds.What’s the hardest piece of feedback you’ve given a founder?

The founder–investor relationship will hit rough patches. You want someone who can tell you hard truths with empathy—not someone who avoids conflict or sugarcoats reality.

The best founders don’t just pitch. They interview. Because capital is everywhere, but the right investor relationship is rare.

Also, other than this, investors will ask you some weird-tough questions, and most founders fail in answering those questions. That’s why, with leading investors and founders, we have created an all-in-one guide that helps you to prepare for such questions.

Check out our all-in-one What investors ask and how to answer guide.

Rethinking the startup MVP: Building a competitive product.

Most founders still treat an MVP as a hacky prototype just to prove an idea. That doesn’t work in today’s crowded markets.

vs today (wavy line)")

The better play is: build a competitive wedge by scoping down your users instead of scoping up your product.

Here’s how you can apply it this week:

Pick your smallest possible audience. Instead of “founders” or “teams,” choose a hyper-specific profile. For example, Linear didn’t target “all developers” — they started with individual contributors at small startups who hated issue tracking.

List their top 3 frustrations. Don’t guess. Ask them, run a short survey, or even use your waitlist form to capture pain points. Only build for the frustrations you hear repeatedly.

Ship for that audience only. Make it clear that your early version is not for everyone. Invite only those who fit your profile, so you avoid churn and gather sharper feedback.

Use your waitlist as a filter. Don’t just collect emails — ask 3–5 qualifying questions (role, company size, current tool, their biggest pet peeve). This way, you can handpick the right testers instead of getting noisy, unfocused feedback.

The win: Instead of trying to “validate” an idea in theory, you create a usable, competitive product for a narrow slice of the market — and that slice becomes your proof of product-market fit. (Read detailed here)

EXPLORE MORE

💡 Reports, Articles and a few interesting stuffs

The Sales Playbook For Founders | Startup School. (Link)

Getting Started with Usage-Based Pricing. (Link)

Alejandro Cremades on startup compensation. (Link)

Excel template: Early-stage startup financial model for fundraising. (Link)

All-In-One guide to pitch deck storytelling - free template & curated resources. (Link)

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Veteran Ventures Capital, a McLean, VA-based venture capital firm investing in dual-use national security technologies, closed Veterans Fund II at $60m. (Read)

Curql Collective, a Des Moines, Iowa-based collective of 160+ credit unions jointly investing in fintech, closed Curql Fund II at $360m. (Read)

Norrsken Evolve, a Stockholm, Sweden-based firm, has completed the first close of its maiden €57M fund. (Read)

New Startup Deals

OneCrew, a San Francisco, CA-based provider of a purpose-built platform for paving contractors, raised $7.5M in Series A funding. (Read)

Garage, a NYC-based marketplace for buying and selling specialised equipment, raised $13.5M in Series A funding. (Read)

Databricks is finalising a $1 billion+ Series K funding round led by Thrive Capital, Insight Partners, and Andreessen Horowitz, boosting its valuation 61% to over $100 billion. (Read)

Ohai.ai, a NYC-based provider of an AI-powered household assistant service, raised a new round of funding. (Read)

Firecrawl, a San Francisco, CA-based developer of a platform that generates web data for developers and AI agents, raised $14.5M in Series A funding. (Read)

Medallion, a San Francisco, CA-based company which specialises in AI-powered provider network infrastructure, raised $43M in new funding. (Read)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

Capital Formation Analyst - March Capital | USA - Apply Here

Associate - Episode 1 Venture | UK - Apply Here

Investment Analyst - Zeta Capital | India - Apply Here

Investor Relations Associate - Alumni Venture | USA - Apply Here

Associate - OMERSE Venture | USA - Apply Here

Investment Analyst - Caanan | USA - Apply Here

Events and Operations Intern - Plug and Play Tech Centre | UK - Apply Here

Partner 16 - a16z | USA - Apply Here

Associate Telescope Partner | USA - Apply Here

Operations & Finance Analyst - Faraday Venture Partner | Spain - Apply Here

Healthcare Analyst - General Investment Management | UK - Apply Here

Investor (AI) - Samsung next | USA - Apply Here

Partner 20 - a16z | USA - Apply Here

VP - Marketing & Communications - Transition VC | India - Apply Here

Investment Analyst - Miras Investment | Dubai - Apply Here

Program Manager - Tenity | UK - Apply Here

PARTNERSHIP WITH US

Get your product in front of over 95,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

Really comprehensive, Sahil!!