Sequoia Capital: The biggest AI opportunity for founders. | 5 predictions that reveal where AI agents will actually make money.

This founder used Claude to validate the idea & Bigger ARR equal better IPO outcomes?

👋 Hey, Sahil here — Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

5 predictions that reveal where AI agents will actually make money.

Does bigger ARR equal better IPO outcomes?

Are AI companies secretly training their models on your chats?

Frameworks & insightful posts :

31 ways to grow your startup fast in 2026.

Sequoia Capital: The biggest AI opportunity for founders.

Framework: How to get warm intros to VCs without a network?

How this founder used Claude to validate the idea (Now at $2.3k MRR)

FROM OUR PARTNER - UPDF

🤝 UPDF - An AI PDF Editor Built for People Who Don’t Have Time to Waste

For professionals who handle large volumes of documents, UPDF’s advanced search and organisation features are invaluable. Quickly locate key information with keyword search, categorise documents with folders and tags, and navigate efficiently with smart indexing.

You can also batch process and export files, making it easier to prepare reports, presentations, or academic materials without repetitive work.

Whether you’re managing contracts, research papers, or business reports, UPDF gives you the flexibility to work seamlessly across Mac, Windows, iOS, and Android.

Try UPDF and simplify how you manage PDFs →

🤝 PARTNERSHIP WITH US

Get your product in front of over 115,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

5 predictions that reveal where AI agents will actually make money.

Everyone is talking about AI agents. But the real question isn’t whether agents will exist - it’s where the money will flow once companies start deploying them at scale.

A recent report from CB Insights breaks this down using hiring signals, funding activity, and enterprise surveys.

Building agents is no longer the hard part. Deploying, securing, and scaling them inside enterprises is.

That shift is creating several new markets around the “agent stack.” Here are the five areas where the biggest opportunities are emerging.

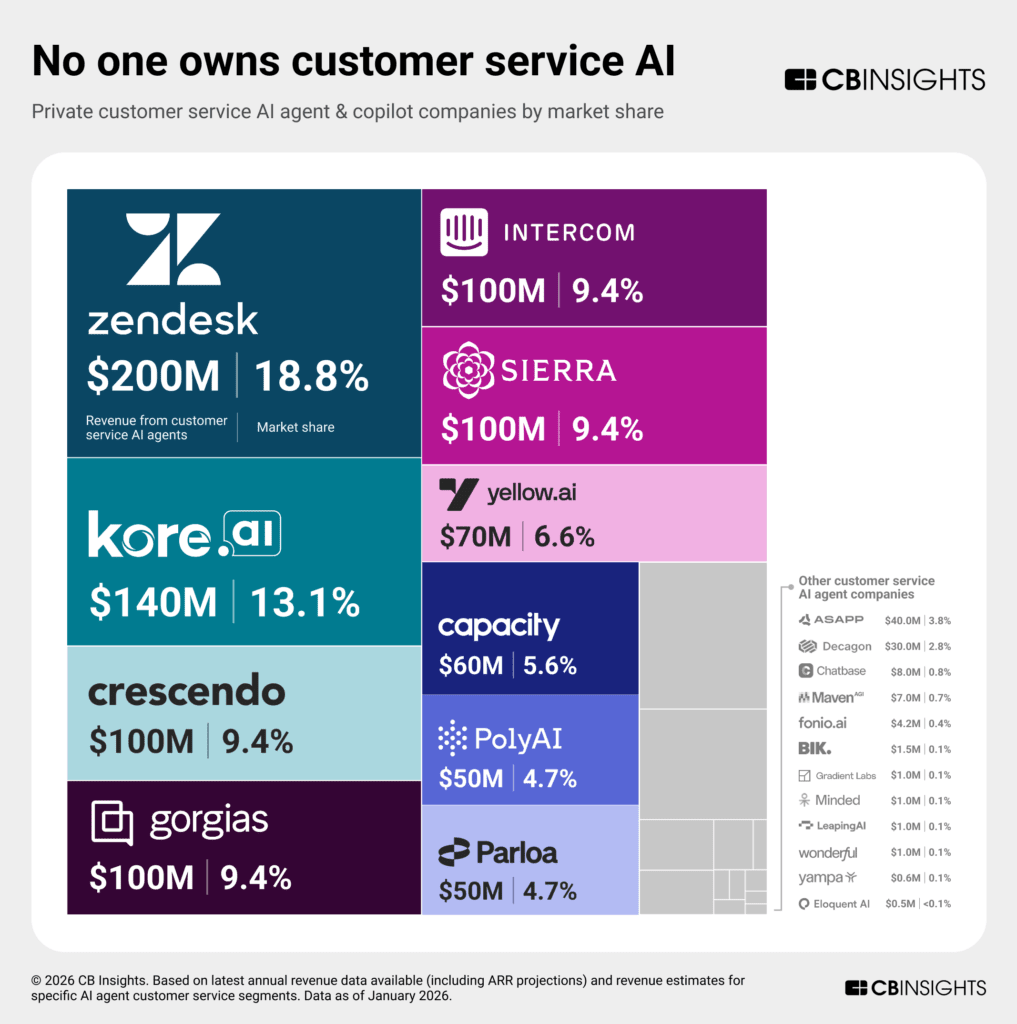

Multimodal AI agents will dominate customer service

Customer support is quickly becoming the largest deployment ground for AI agents. According to the enterprise survey, it’s already the #1 adoption area for enterprise AI agents, with 115+ companies competing in the market and at least 6 private companies generating $100M+ in revenue.

The next wave of competition will revolve around multimodal capabilities - agents that seamlessly operate across: voice, text, documents, images and video inputs.

Voice is becoming the real proving ground. Handling interruptions, latency, and conversational turn-taking requires much deeper architectural design than text agents simply adding voice later.

This is why AI-native entrants like Sierra (2023) and Crescendo (2024) are quickly climbing into the top revenue leaders alongside earlier companies like PolyAI.

So the next generation of customer service tools won’t just automate tickets, they’ll manage conversations across every channel.

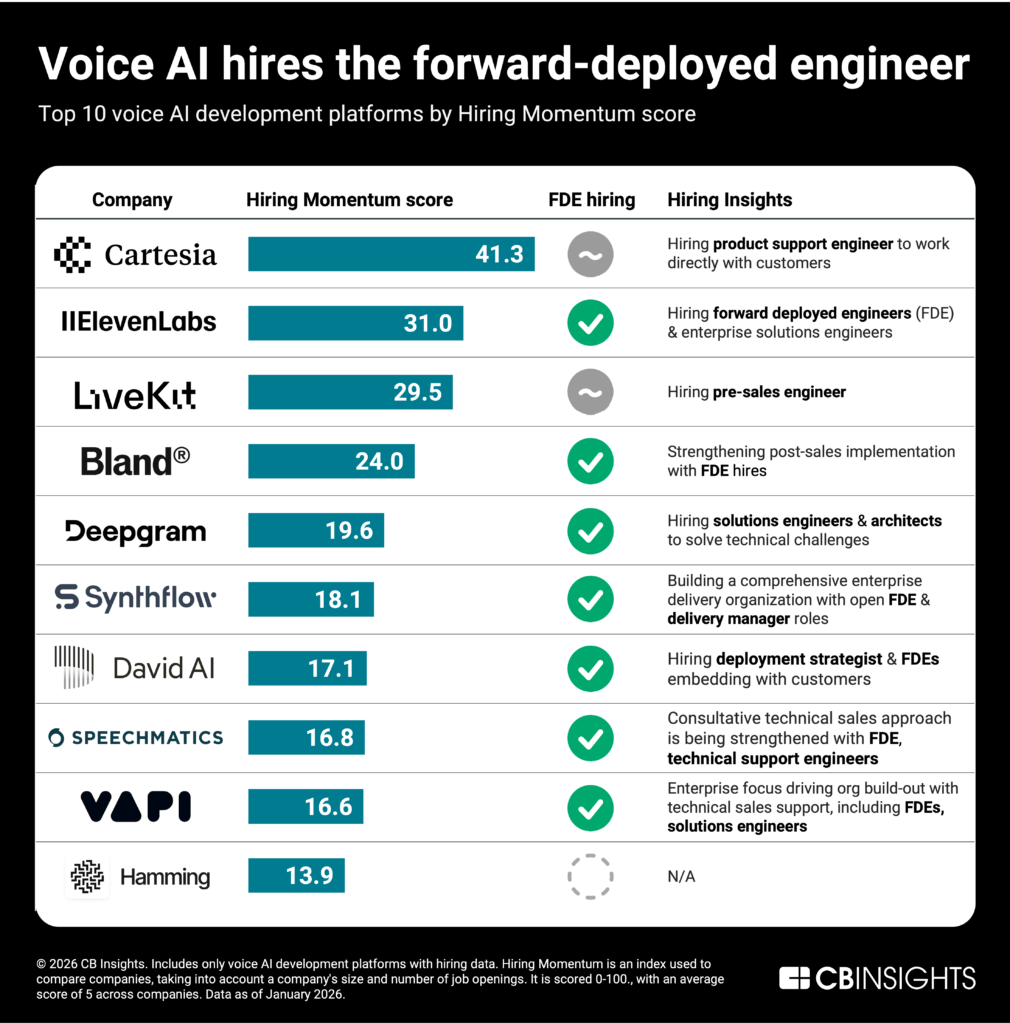

Voice AI will shift to “high-touch” deployments

Most AI tools today follow a self-serve model. Voice AI is going the opposite direction.

Startups such as ElevenLabs, Deepgram, Bland AI, Vapi, and Synthflow are increasingly hiring forward-deployed engineers and solutions architects to work directly with enterprise clients.

Why? Most enterprises still struggle with real-world AI implementation.

CB Insights’ survey found:

65% of companies lack internal expertise

59% cite integration complexity as the main barrier

So instead of selling software alone, vendors are embedding engineers directly inside customer environments to integrate voice agents with legacy systems.

This approach sacrifices some margin but dramatically increases enterprise adoption - especially in industries like healthcare, finance, quick-service restaurants, and government.

AI agent security will become mandatory infrastructure

Agents introduce a new type of security risk. Unlike copilots, agents can:

execute code

call APIs

move data between systems

make decisions autonomously

That means every tool an agent accesses becomes a potential attack surface.

Security vendors are responding with continuous red teaming systems, tools that simulate attacks against AI agents to uncover vulnerabilities before real attackers do.

These systems test issues like: prompt injection, agent hijacking, tool misuse and multimodal attacks

Startups like Virtue AI are building platforms that continuously stress-test agents in production environments.

Large cybersecurity players are already moving quickly:

Palo Alto Networks acquired Protect AI

Check Point acquired Lakera

F5 acquired Calypso AI

The message is clear: AI security is becoming an extension of traditional cybersecurity infrastructure.

AI agent observability will trigger a wave of acquisitions

Once agents are deployed, enterprises need tools to answer a simple question:

What are these agents actually doing? That’s why the market for agent observability and evaluation tools is heating up.

These tools help companies:

monitor agent decisions

audit behavior

Evaluate model performance

manage permissions and governance

M&A activity across the AI agent ecosystem jumped 10x in 2025, approaching 100 deals, with observability and evaluation tools becoming prime acquisition targets.

Examples include:

Coralogix acquiring Aporia

Snyk is acquiring Invariant Labs

ClickHouse acquiring Langfuse

Anthropic acqui-hiring HumanLoop

Even infrastructure giants are positioning themselves.

Datadog has already invested in multiple observability startups, including LangChain, Arize, Braintrust, and Patronus AI. Enterprise platforms like Salesforce and Workday are also expected to acquire reliability tooling to support their own agent ecosystems.

As Bessemer Venture Partners recently noted, AI evaluation remains one of the biggest bottlenecks in enterprise deployment.

Solving that bottleneck could unlock the next wave of adoption.

World models will power the next generation of physical AI

While software agents are transforming enterprise workflows, another frontier is emerging: physical AI agents.

These systems rely on world models, AI systems that simulate real-world physics such as gravity, friction, and object interactions.

World models allow robots, autonomous vehicles, and factory systems to train in simulated environments before operating in the real world.

Signals suggest this market is accelerating quickly:

Funding activity ranks in the top 3% of CB Insights markets

Talent from leading AI researchers is entering the space

Major companies are hiring aggressively to build simulation environments

Examples already appearing across industries include:

Waymo is building 4D world models for autonomous driving

Agility Robotics and Figure AI using Nvidia simulation models

Manufacturing systems using AI agents to autonomously manage factory operations

The result is a new foundational layer for robotics and physical automation.

Half the companies in this category are still early-stage or research-focused, but the hiring, investment, and deal activity suggest world models will soon become core infrastructure for physical AI systems.

Put together, these signals reveal an important shift.

The first wave of AI focused on models.

The second wave focused on applications.

The next wave will focus on deployment infrastructure.

And the companies that capture value will likely sit in the layers that make AI agents reliable, secure, and usable inside real businesses.

Does bigger ARR equal better IPO outcomes?

For years, venture capital has pushed a simple narrative: bigger ARR equals better IPO outcomes.

But when you actually look at public market data, the relationship is much weaker than most people assume.

Dan Grey recently highlighted an analysis from Meritech Capital that examines how ARR scale correlates with valuation multiples in public SaaS markets. The conclusion challenges one of venture capital’s most persistent assumptions.

There is very little correlation between ARR size and valuation multiples.

In a regression comparing revenue multiples vs ARR scale, the R² is just 0.11 - meaning ARR explains only a small portion of valuation differences. When outliers like Adobe and Salesforce are included, the correlation drops even further to around 0.02.

In simple terms: bigger companies do not automatically get higher valuation multiples.

The reason many investors believe they do comes down to something simpler -selection bias.

Companies with billions in ARR typically already have strong fundamentals:

durable growth

strong margins

leadership positions in large markets

defensible competitive advantages

Those qualities allow them to scale into the largest revenue buckets. But it’s those underlying qualities, not the scale itself, that public markets reward.

In other words, scale often reflects quality, but it doesn’t cause it.

The problem, according to Grey, is that venture incentives have gradually distorted this distinction.

Private market investors frequently optimise for rapid ARR growth at almost any cost, because higher revenue numbers support larger funding rounds and valuation markups. That dynamic encourages companies to prioritise aggressive scaling even when the underlying business quality isn’t strong.

Over time, this creates several structural problems.

Companies stay private far longer than necessary.

Public investors miss the early growth phase while private capital captures most of the upside.

Post-IPO performance deteriorates.

Businesses optimised for growth at all costs often struggle once public markets demand profitability and capital discipline.

Capital flows toward scalable models rather than innovative ones.

Ideas that can scale ARR quickly attract funding, even if they aren’t the most transformative technologies.

The result is an ecosystem where ARR becomes the headline metric, even though public markets evaluate companies using a much broader set of criteria.

Public investors typically look at a combination of factors:

sustainable growth rates

margins and operating leverage

total addressable market

product differentiation and competitive positioning

Revenue scale plays a role, but it’s only one piece of the puzzle.

This distinction also explains why some smaller SaaS companies can still command strong multiples if they demonstrate exceptional fundamentals, while larger companies with weaker economics may trade at lower valuations.

The deeper insight for founders is simple. Chasing ARR milestones purely to hit arbitrary “IPO thresholds” can be misleading. Public markets don’t reward size alone, they reward durable business quality that can scale over time.

In many cases, scale is simply the outcome of those fundamentals working. Not the reason investors value the company in the first place.

Are AI companies secretly training their models on your chats?

Most people assume their conversations with AI are private. But according to new research, that assumption may not match reality.

A group of Stanford researchers, King, Klyman, Capstick, Saade, and Hsieh, recently analysed the privacy policies of six major AI chatbot providers: Amazon, Anthropic, Google, Meta, Microsoft, and OpenAI. Together, these companies control an estimated 90% of the U.S. chatbot market.

Their key finding: every one of these companies trains AI models on user chats by default.

The shift became universal in September 2025, when Anthropic moved from an opt-in system to an opt-out model, aligning with the rest of the industry.

That means, unless a user explicitly changes settings, their conversations may be used to improve AI systems. The research surfaced several important dynamics shaping how AI companies handle user data.

Training on chat data is now the default industry practice.

All six major developers allow model training using user inputs and outputs. While enterprise customers are typically excluded from this data usage, individual consumers are included by default.

Enterprise and consumer users receive very different protections.

Companies generally opt enterprise customers out of model training automatically, creating a two-tiered privacy system. Businesses get stronger data protections, while hundreds of millions of consumer users remain part of the training pipeline unless they manually opt out.

The scale of data involved is enormous.

OpenAI alone reported around 700 million ChatGPT users as of August 2025. Given that most people never adjust default settings, a massive amount of conversational data is likely feeding model training systems.

Researchers also highlighted how difficult it can be for users to even understand these practices.

Across the six companies, the team analysed 28 separate policy documents, including privacy policies, FAQs, and additional sub-policies. Information about data usage was often scattered across multiple pages rather than clearly explained in a single place.

In one example, OpenAI’s data practices required six different documents to fully understand how chat data may be used.

That fragmentation makes it extremely difficult for ordinary users to grasp what happens to their conversations.

Another subtle dynamic involves how opt-out choices are framed.

Some platforms present the option to disable training with messaging such as “Help improve the model for everyone.” Researchers argue that framing like this can encourage users to leave defaults unchanged, aligning user behaviour with company incentives.

For AI developers, this approach has a clear advantage: conversational data is one of the most valuable resources for improving models, especially as companies compete to build more capable systems.

But it also raises broader questions.

As AI becomes embedded in everyday workflows, from writing and coding to therapy-like conversations, the boundary between private communication and training data becomes increasingly blurred.

If privacy matters, it’s worth checking platform settings and understanding whether conversations are being used for training.

Because in most cases today, the default answer is yes.

SOMETHING MORE

🧩 Frameworks & insightful posts

31 ways to grow your startup fast in 2026.

Most founders try every growth tactic they see on the internet. The fastest-growing SaaS companies don’t. They sequence their growth — using the right 3–5 levers at the right revenue stage. ICONIQ, Founderpath, and hundreds of SaaS founders keep repeating the same thing: growth is not about working harder, it’s about picking leverage that compounds.

Below is a cleaner, practical breakdown you can follow no matter where you are shared by Nathan Latka :

Stage 1: Bootstrap to $1M Revenue — Speed and Cash First

At this stage, anything slow is a distraction. You want distribution loops, cheap awareness, and anything that directly converts attention into revenue.

What works best

Virality loops: Add sharing triggers like “Powered by…”, referral rewards, and shared dashboards. This is how tools like Typeform and Dropbox grew without ads.

Webinars that sell Run tight, niche sessions with a strong CTA. Founders who are good storytellers convert faster because webinars collapse trust cycles.

Product Hunt launches. One strong PH push = thousands of new users. Relaunch often, test different angles, and collect emails.

Cold outreach with personalisation, Loom videos + targeted lists outperform templates. Even 100 great emails can get your first $10K–$20K MRR.

Influencer marketing (micro-creators only) Bottom-up trust works better than polished brand ads. Partner with niche creators who feel “native” to your audience.

What founders should remember At <$1M, your job is to find one repeatable way to acquire users cheaply. Most founders stall because they chase too many channels instead of doubling down on one.

Stage 2: $1M–$3M ARR — Build Compounding Inbound + Partnerships

This is where the engine needs more predictability. Founders who grow 300%+ yearly build content systems, partner loops, and scalable inbound.

Plays that work consistently

Free tools Calculators, templates, grading tools — these index extremely well and convert better than blog posts. Shopify scaled free tools into billions.

Newsletter Publishing weekly builds authority, lowers CAC, and compounds trust. At this stage, the founder voice is still the strongest asset.

Co-marketing with partners Joint webinars, shared ebooks, mutual case studies. This drives warm leads at almost zero cost.

Affiliate programs Think of it as a distributed sales team that only gets paid on performance. Stripe and Zapier used this extremely early.

Compare pages and programmatic SEO “X vs Y” pages rank fast for high-intent queries and consistently pull in users without spending.

Founder reminder Your time shifts from raw selling → building repeatable acquisition flywheels.

Stage 3: $3M–$5M ARR — Paid Growth + Acceleration

Now you have a working engine. The question becomes: how do we scale what already works while keeping CAC under control?

High-impact tactics

Retargeting Target people who already touched your product — demo viewers, free trials, website visitors.

Lookalike ads Feed Meta/Google a list of your top 500 users. This performs better than any cold targeting.

LinkedIn + short-form video ads Works well for B2B if messaging focuses on revenue triggers, not features.

Acquisitions (small ones) Buy small tools, Chrome extensions, or utilities that give you more distribution or features instantly.

Founder reminder Paid acquisition works when your retention is strong. If churn is weak, nothing in this stage will scale.

Stage 4: $5M+ ARR — Build Moats That Defend Your Category

At this point, growth comes from trust, brand presence, and ecosystem dominance. These plays are slow but incredibly durable.

Moats that actually work

Review site dominance G2, Capterra, and TrustRadius. Enterprise buyers care more about peer validation than ads.

App marketplace distribution: Salesforce, HubSpot, Zapier — marketplaces can become passive growth channels.

Books + podcasts + events These aren’t vanity — they’re how you cement a category narrative and attract higher-ticket buyers.

Live events + communities You build a tribe around your brand. Companies like Notion and Figma built defensibility with community long before they had revenue.

Founder reminder At scale, your advantage is no longer speed. It’s authority, relationships, and the ecosystems you control.

You don’t need all 31 tactics. You need the right ones for your stage. The best founders don’t hustle harder, they sequence smarter — and they resist the temptation to mix Stage 1 tactics with Stage 4 tactics. That’s how companies go from $0 to $10M without burning themselves out.

Sequoia Capital: The biggest AI opportunity for founders.

Most founders building AI products worry about the same thing: What happens when the next model update turns my product into a feature?

It’s a valid concern. If you’re selling a tool, you’re competing directly with the model itself. But there’s another path emerging, one that may create much larger companies.

Instead of selling the tool, sell the work. For example, a company might pay:

$10K/year for accounting software

But $120K/year for accountants to close the books.

The next generation of AI companies won’t just sell accounting software; they’ll close the books themselves.

That shift from copilot (tool) to autopilot (outcome) could unlock a massive opportunity.

Where AI agents are actually being used today

Recent data shows where AI agents are already doing real work.

Nearly half of all agent activity today is in software engineering, while every other category is still relatively small.

Top domains where AI agents are deployed today:

Software engineering: ~49.7%

Back-office automation: 9.1%

Marketing & copywriting: 4.4%

Sales & CRM: 4.3%

Finance & accounting: 4.0%

Data analysis: 3.5%

This pattern reveals something important.

Software engineering is largely intelligence work, translating specifications into code, debugging, and testing. AI excels at this type of structured problem-solving.

Other professions still require more judgement, which slows automation.

But that gap is shrinking quickly.

Copilots vs Autopilots

Most AI startups today are building copilots. A copilot helps professionals do their job faster. The human remains responsible for the output.

Examples:

Harvey → helps lawyers

Rogo → helps investment bankers

coding copilots → assist developers

But a new category is emerging: autopilots. Autopilots don’t help professionals - they replace the workflow entirely.

Examples already appearing:

Companies drafting NDAs directly instead of hiring lawyers

AI systems are closing accounting books

Insurance purchased through AI brokers instead of human brokers

The difference is massive.

A copilot captures the software budget.

An autopilot captures the labour budget.

And labour budgets are far larger.

The smartest place to start: outsourced work

The easiest entry point for autopilots isn’t replacing employees, it’s replacing outsourced services.

When a task is already outsourced, three things are true:

The company already pays an external vendor

There’s a clear budget line

The buyer is purchasing an outcome, not a tool

That makes switching to an AI service much easier.

For example:

Replacing a legal service with an AI legal service → simple vendor swap

Replacing internal employees → requires a full organisational change

So the playbook is simple: Start with outsourced tasks that are intelligence-heavy.

Some of the biggest opportunities

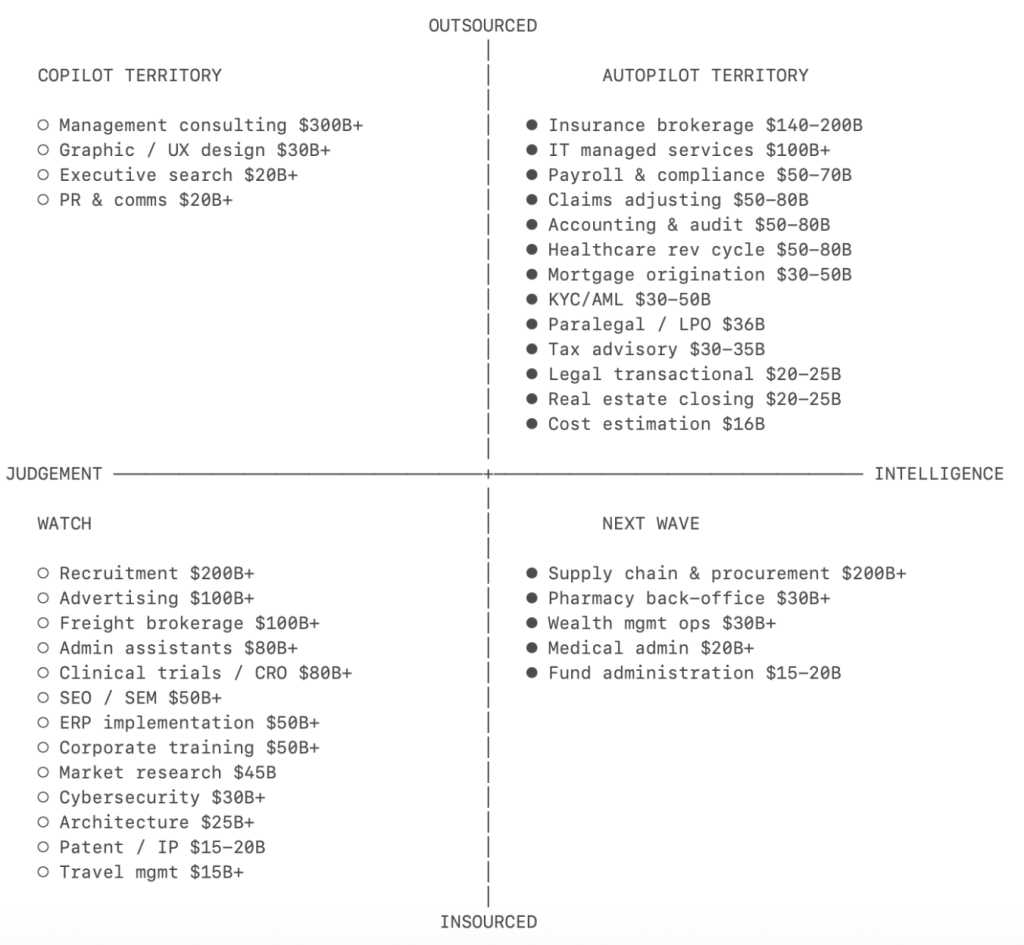

Sequoia Capital shared this - When you map services markets by intelligence vs judgment and outsourced vs internal, several large AI opportunities appear.

Examples include:

Insurance brokerage ($140–200B) Brokers mostly compare policies and fill forms, highly structured work that AI can automate.

Accounting & audit ($50–80B). The profession faces a major labour shortage, making firms more open to automation.

Healthcare revenue cycle ($50–80B). Medical coding translates clinical notes into standardised codes, complex but rule-based work.

Claims adjusting ($50–80B). Interpreting insurance policies and calculating settlements follow structured processes.

Tax advisory ($30–35B). Multi-jurisdiction tax rules are exactly the type of complexity AI handles well.

IT managed services ($100B+). Monitoring systems, patching, and troubleshooting are repetitive intelligence tasks.

Supply chain & procurement ($200B+) Large enterprises leave huge portions of supplier negotiations untouched because humans can’t manage the scale.

Why this shift matters

For every $1 spent on software, roughly $6 is spent on services. That means the real AI opportunity may not be software tools at all, it may be AI-native services companies.

Companies that:

sell outcomes instead of tools

automate entire workflows

Capture labour budgets rather than software budgets

The next generation of AI giants may look less like traditional SaaS companies and more like services firms powered by AI systems.

In other words, the next trillion-dollar company might be a software company that looks like a services company.

Framework: How to get warm intros to VCs without a network?

Toby Egbuna shared one of the best no-network fundraising tactics and ways to get intros

Instead of cold emailing 300 VCs, he recommends this step-by-step process:

Shortlist 30 top funds you actually want

Use Crunchbase to find their 3 most recent portfolio founders

Connect with those founders on LinkedIn

Email and ask for a quick chat about their experience with the fund

If the call goes well, ask for a warm intro

Why it works:

Founders usually say yes

VCs value intros from their own portfolio more than cold emails

You often get bonus intros to other funds too

“You don’t need a huge network. You just need a system.”

Here’s the 14-step process Toby recommends:

Build a list of 300+ VCs

Prioritise the top 10% (30 funds) based on thesis, connections, brand, and fit

Filter for just those 30

Go to Crunchbase

Search each fund

Find the 3 most recent investments

Note founder names, sites, and companies

Repeat for all 30 funds

Go to LinkedIn

Send a connection request to every founder

Open your email

Email each founder asking about their experience (include a short, warm note)

Do the calls, be genuinely curious

If it goes well, ask for the intro

How this founder used Claude to validate the idea (Now at $2.3k MRR)

From a Reddit founder who turned 12 scattered SaaS ideas into one that actually made money, all by using Claude for validation instead of guesswork.

They had tried everything before: built two projects, got almost no users, lost motivation. The turning point came when they stopped building from instinct and started validating using real user complaints.

Here’s the process that worked:

Use AI to find real pain, not fake demand.

They prompted Claude to scrape Reddit, Quora, G2, and other public forums for real complaints about “cold email personalisation.”

It came back with 3 pages of data, real quotes from salespeople complaining about manual personalisation, bad templates, and low reply rates.

Ask AI to rate the opportunity.

They told Claude to score the idea 1–10 on “demand vs. competition.” It gave an 8.5, with reasoning about why the gap existed. That was enough to commit.

Build the simplest version fast.

They built Introwarm, upload a prospect list, and it generates personalised openers by analysing what each person posts or reacts to online.

Soft-launched it quietly → got the first paid user ($29) in week 2 → now at $2.3K MRR.

What founders can steal from this:

Users are already validating your ideas for free, in the form of online complaints.

AI can connect patterns way faster than manual research.

You don’t need “perfect” validation, just enough data to prove people care.

Prompt

You are my personal market research assistant. I’m a solo developer, fully bootstrapped, building B2B or prosumer SaaS tools with a strict infrastructure budget of $200/month or less. No big team, no venture capital, just me coding and deploying.

Your job is to scan the web for current, real pain points that users, developers, or small businesses are struggling with. You can look in forums (Reddit, Hacker News, Indie Hackers, Twitter/X, GitHub issues, niche Discords, Quora), reviews, blog comments, etc.

My main goal is to scale a product from $0 to $10k month and see how it goes from there.

For each opportunity you surface, break it down like this:

1. Pain Point: Describe the real-world problem or complaint users are having.

2. Target Audience: Who is having this problem? Be specific.

3. Why It Hurts: Explain why this problem matters or costs them time, money, or peace of mind.

4. Tool Idea: Suggest a simple SaaS or tool I could build to solve it, considering my constraints:

- Solo dev

- <$200/month infra

- MVP in ~2 weeks

5. Monetization Potential: Explain how it could realistically make money (subscription, pay-per-use, etc.)

6. Bonus: If applicable, mention existing solutions and what sucks about them (pricing, UX, complexity, etc.)

Keep the tone direct, no fluff, and prioritize practicality over theory. Focus on problems people are actively complaining about, not abstract trends or “maybe someday” ideas.NEWS RECAP

🗞️ This week in startups & VC

New In VC

Axiom Partners, a San Francisco, CA-based early-stage venture capital firm, closed its $52M inaugural fund. (Link)

General Catalyst, a Silicon Valley–based venture firm with $43B+ AUM, has committed $5 billion to India over the next five years to back startups. (Link)

Quantonation Ventures, a NYC and Paris, France-based venture capital firm focused on quantum and physics-based technologies, closed its second flagship fund at €220m. (Link)

New Startup Deals

Vivox AI, a London, UK-based technology company building regulator-ready, atomic AI agents for AML, KYB/KYC and financial crime, raised £1.3M in its first funding. (Link)

Vor Systems, a San Francisco, CA-based provider of an AI-enabled transaction platform, raised $3M in Pre-Seed funding. (Link)

Navigara, a San Francisco, CA-based developer of an engineering performance measurement layer, raised $2.5M in Seed funding. (Link)

PartsPulse, a Las Vegas, NV-based provider of an AI-powered platform for managing parts businesses, raised $3M in funding. (Link)

Cyclops, a Miami, FL-based stablecoin and crypto infrastructure platform provider, raised $8M in funding. (Link)

Shellworks, a London, UK-based bio-materials startup, raised $15M in Series A funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Partnerships & Community Manager - Pear VC | USA - Apply Here

Portfolio Operations Associate - BVP | USA - Apply Here

Analyst - Iconique Capital | USA - Apply Here

Network Lead - Catalyst Lap | USA - Apply Here

Analyst - Infrastructure & Real Assets - Stepstone Group | Australia - Apply Here

Analyst / Associate - Saints Capital | USA - Apply Here

Head of Investor Community - Inovexus | Remote - Apply Here

Associate - Lightbank | USA - Apply Here

Investment Analyst Intern - NAV Capital | Dubai - Apply Here

PE & VC Partner Manager - Dealhub | UK - Apply Here

Investment Analyst - Lunicorn Venture | UK - Apply Here

Program Manager - a16z | USA - Apply Here

VC Platform & Events Manager - 1001 VC | USA - Apply Here

MBA Venture Capital Intern - Cerity Partners | USA - Apply Here

MBA Venture Capital Intern - Cerity Partners | USA - Apply Here

PARTNERSHIP WITH US

Get your product in front of over 115,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

Hi Sahil! Sequoia's thesis on AI-Native Service Companies is interesting. You don't own the software layer but do the work. Services businesses such as law firms, accounting firms and consultancies often had to hire more people to increase profit. However, with the advent of AI the relation between headcount and profit margin no longer are relevant. What I think about AI-Native Service Businesses that puts them at advantage is compounding intelligence. These AI-Native Service Businesses can build a knowledge base that continues to compound and make the AI tool accurate as each and every matter is completed. This is the real advantage as in a normal service business the knowledge usually walks out with the partner who handled the matter. Furthermore, these AI-Native businesses can use the roll-up strategy to acquire existing service providers and optimize them with AI.

I write a blog in LegalTech titled "The LegalTech Thesis" where I analyze the LegalTech sector and identify opportunities to build. Would love to connect and get your thoughts on my latest post!

https://harshithviswanath.substack.com/p/three-legaltech-whitespace-plays

this is very good. one pattern we see from our seat tracking 600+ VC newsletters: the autopilots winning right now are quietly buying small services businesses and rebuilding them on AI underneath, instead of trying to displace them from the outside. roll-up + AI is becoming the real autopilot moat