Some AI companies are about to disappear. Here's how to tell if yours is one of them.

It's called 'token capital.' Most founders have never heard of it and it might be the only thing that decides if they survive.

👋 Hey, Sahil here - welcome to this edition of Venture Curator, where we break down how great startups grow, how top investors think, and what’s shaping the future of tech.

P.S. Get access to 100+ startup & VC resources, investor databases, fundraising templates, 150+ premium archive posts and exclusive startup research - all in one place.

FROM OUR PARTNER - AQUIPOR

🏗️ Investors are backing AquiPor as cities face a $27B stormwater infrastructure shift…

Concrete covers modern cities - but it also creates one of the biggest environmental problems in urban infrastructure. Every time it rains, polluted stormwater floods streets, overwhelms drainage systems, and contaminates waterways.

AquiPor has developed a porous concrete technology that turns ordinary concrete into infrastructure-grade stormwater management systems, helping cities reduce flooding, recharge groundwater, and meet growing environmental regulations.

Why investors are paying attention:

Permeable pavement market projected to reach $27B by 2031

Third-party testing showed 97.2% filtration of stormwater particles

Paid pilot projects and demonstration installations already completed

Asset-light licensing model designed for scalable recurring revenue

As cities spend billions upgrading ageing infrastructure and managing climate-driven flooding, technologies built directly into existing construction materials could become critical infrastructure layers.

AquiPor is positioning itself at the intersection of climate tech, construction, and water infrastructure - while the market is still early.

📜 DEEP DIVE

Some AI companies are about to disappear. Here’s how to tell if yours is one of them.

A few weeks ago, a founder we know - Series A, decent revenue, the kind of company that gets written up as an “AI success story” - got a call from his lead investor for a routine portfolio check-in. Then the investor asked one question that the founder couldn’t answer cleanly:

If your model provider doubled its prices tomorrow, what happens to your margins?

He didn’t know. Not exactly. He knew his burn rate to the dollar. He knew his CAC, his churn, his NRR. He’d never actually sat down and worked out how much of his product’s value lived inside an API call he didn’t control.

That conversation has been happening a lot lately, in different forms, at different stages. It’s not really about pricing. It’s about a blind spot that’s gotten enormous while almost nobody was watching it - because for the last three years, the AI boom rewarded speed, not ownership. Ship the feature. Wire up the API. Worry about the rest later. Later kept getting pushed out, and now a lot of “later” is arriving at once.

Nobody built this blind spot on purpose. It’s just what happens when an entire industry optimises for speed over five straight years.

Then Satya Nadella gave the blind spot a name

Recently, Microsoft’s CEO posted something on X -

Just a framework, offered plainly, for a thing a lot of operators have felt but never quite said.

"Every company is going to have to build what I think of as human capital and token capital.

Human capital comprises the knowledge, judgment, relationships, ingenuity, and pattern recognition of its people, while token capital is the firm's AI capability it builds and owns."

Strip away the corporate phrasing and what he’s pointing at is pretty simple -

Companies have always tracked one kind of capital - the people, the relationships, the institutional knowledge sitting in a few senior heads. Nobody’s been tracking the other kind. The AI layer itself: do you actually own it, or are you just renting access to someone else’s?

Nadella isn’t warning about something that might happen. He’s describing something that already has, to companies that found out the hard way, usually right around the time a funding round or an acquisition conversation forced the question.

So that’s what this issue is actually about. Not a recap of his post. Instead, we went and found the actual numbers: what it costs a company when its AI is rented instead of owned, what the market pays extra for the ones that own it, and a five-minute test that tells you which one you are right now.

What we cover in this issue

The rented land problem - what API dependency really costs you

The defensibility spectrum - where does your company sit right now?

The model swap test - one question that reveals everything about your AI moat

What investors are about to ask you - The due diligence questions on AI ownership.

How to start building token capital this quarter - even if you're not a technical founder

The rented land problem - What API dependency actually costs you.

Here’s a scenario that played out in hundreds of AI startups across 2024 and 2025.

A founder builds a great product on top of GPT-4. Customers love it. Revenue grows. The team builds product intuition, the go-to-market works, and a Series A gets done at a solid multiple.

Then OpenAI

releases a native feature that does 80% of what the startup does, for free, inside ChatGPT.

Or the API pricing jumps, and it did, three times in 2025 alone.

Or a cheaper model from a competitor becomes available, but the entire product is so tightly coupled to OpenAI’s specific output format that switching would require a rebuild.

In each case, the startup discovered the same hard truth: the intelligence was never theirs. The economic consequences are real and measurable.

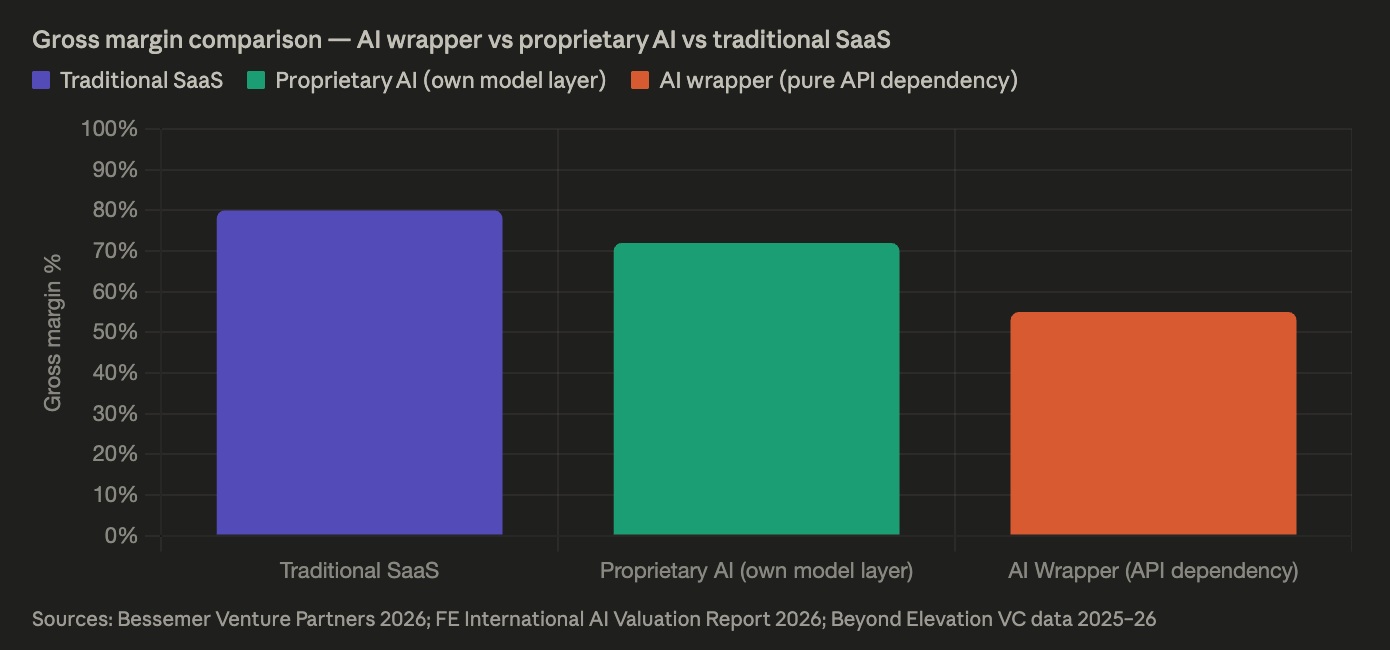

Bessemer Venture Partners found that AI wrapper startups - companies with no proprietary model layer - require 3.2 times more funding to reach profitability versus traditional SaaS businesses.

Traditional SaaS runs gross margins of 70-90%. AI wrappers run 50-60%, on a good day. And every time an API provider adjusts pricing, those margins shrink further - with no recourse and no leverage.

The valuation story is equally stark.

In 2025-26, AI startups with proprietary data moats and defensible model layers commanded 25-30× revenue multiples. While wrapper companies -