Stanford AI Index report reveals: what matters in AI next (most founders miss this). | Is your AI feature secretly killing your margins?

This is the safest job in the age of AI - Shopify team analysis? & The biggest shift in the tradidional seed investing.

Find the right investors to pitch - with Evalyze

Most founders pitch the wrong investors and waste weeks sending cold emails that go nowhere.

I’ve seen this happen a lot - the problem usually isn’t your startup. It’s not knowing who’s actually a fit.

Evalyze helps fix that. It analyses your startup the way a VC would, then shows you investors who are actually likely to say yes - along with why they’re a match.

See your Investor Readiness Score (benchmarked vs funded startups)

Get matched with relevant investors, with clear reasoning

Export verified contacts (emails + LinkedIn)

Improve your pitch with a quick AI deck review

Instead of guessing, you approach the right people with context.

7,000+ startups are already using it.

Get your investor readiness score, free →

👋 Hey, here’s today at a glance -

Big idea + report of the week :

Stanford AI Index Report reveals: Is AI progress plateauing or quietly compounding?

Do you really need Stanford or Harvard to build a unicorn?

Frameworks & insightful posts :

Is your AI feature quietly killing your saas margins?

This is the safest job in the age of AI - Shopify team analysis?

Is the traditional seed investing playbook already broken?

START WITH

🧠 Big idea + report of the week

Stanford AI Index Report reveals: Is AI progress plateauing or quietly compounding?

There’s a narrative floating around that AI might be plateauing. That we’ve seen the peak, and now progress will slow.

The 2026 AI Index Report from Stanford tells a very different story.

If anything, AI isn’t slowing - it’s compounding across every layer at once: capability, adoption, investment, and global competition. And the gap between perception and reality is widening fast.

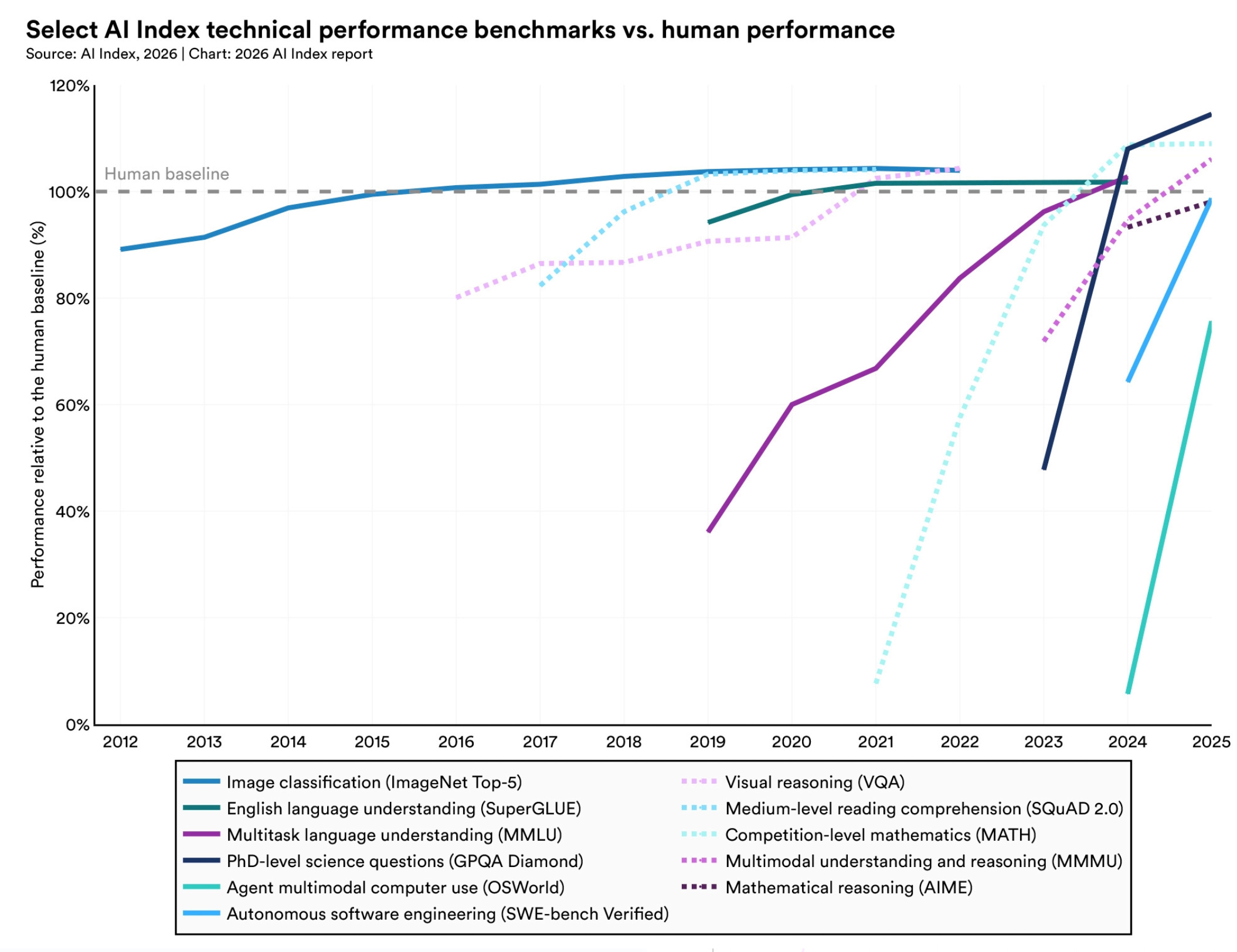

Start with the most important signal: capability.

In 2025, 90%+ of frontier AI models were built by industry, not academia.

And these models aren’t just incremental upgrades anymore. They’re now solving PhD-level science questions, performing near-perfectly on coding benchmarks, and even winning gold-medal-level math competitions.

But at the same time, they still fail at simple tasks like reading analogue clocks reliably.

That contradiction is what researchers call the “jagged frontier.” Progress isn’t linear- it’s uneven, unpredictable, and happening in bursts. Which makes it harder to evaluate how “good” AI really is.

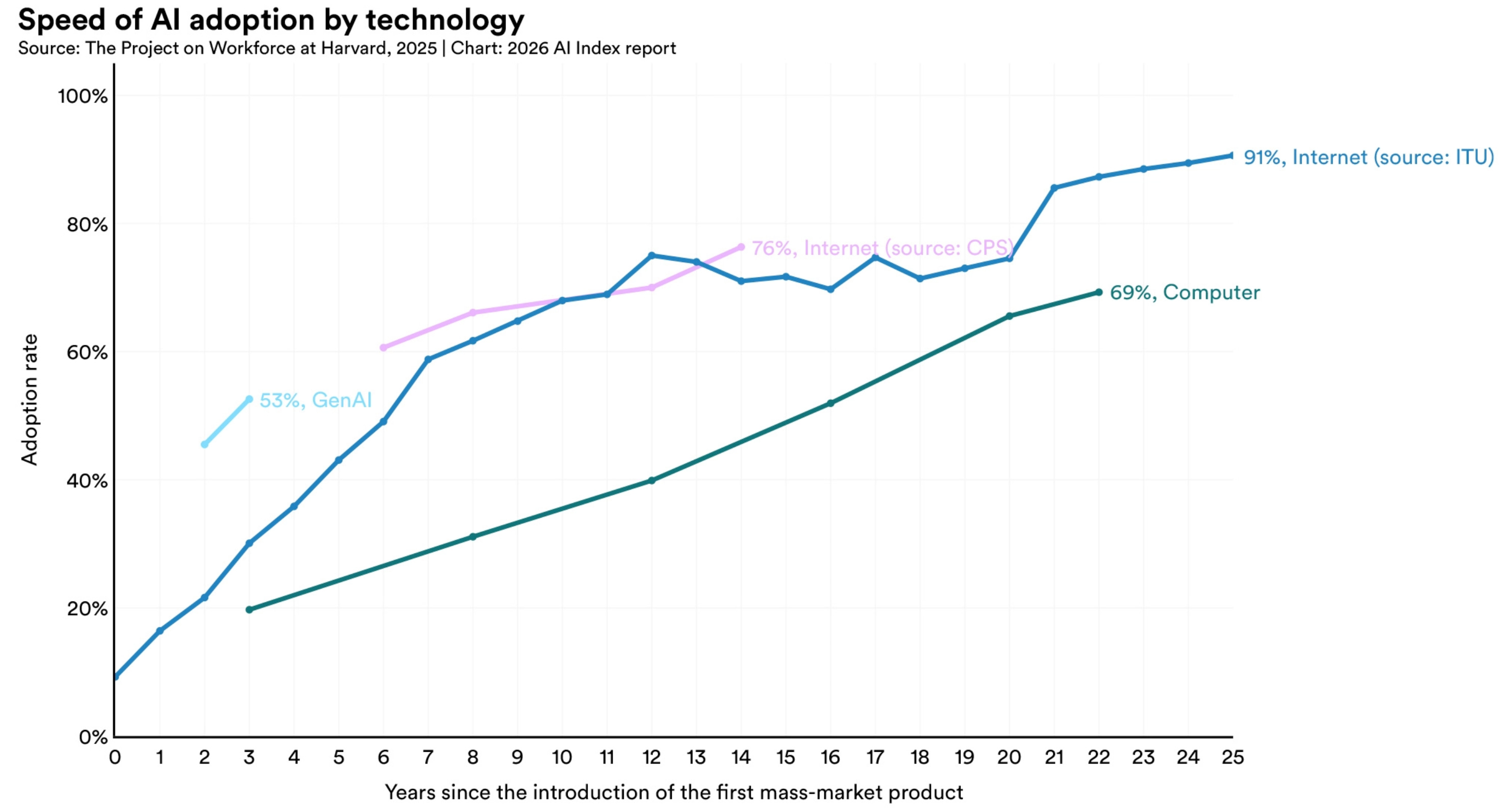

Now layer in adoption.

AI has reached 53% population adoption in just 3 years, faster than both the internet and the PC.

In parallel, 88% of organisations are already using AI, and 4 out of 5 university students rely on it regularly.

This is no longer early adoption. This is infrastructure-level penetration.

And interestingly, much of this value is being created before it’s fully monetised. In the U.S. alone, generative AI tools are estimated to deliver $172B in annual consumer value, much of it through free or underpriced products.

Then comes the geopolitical layer.

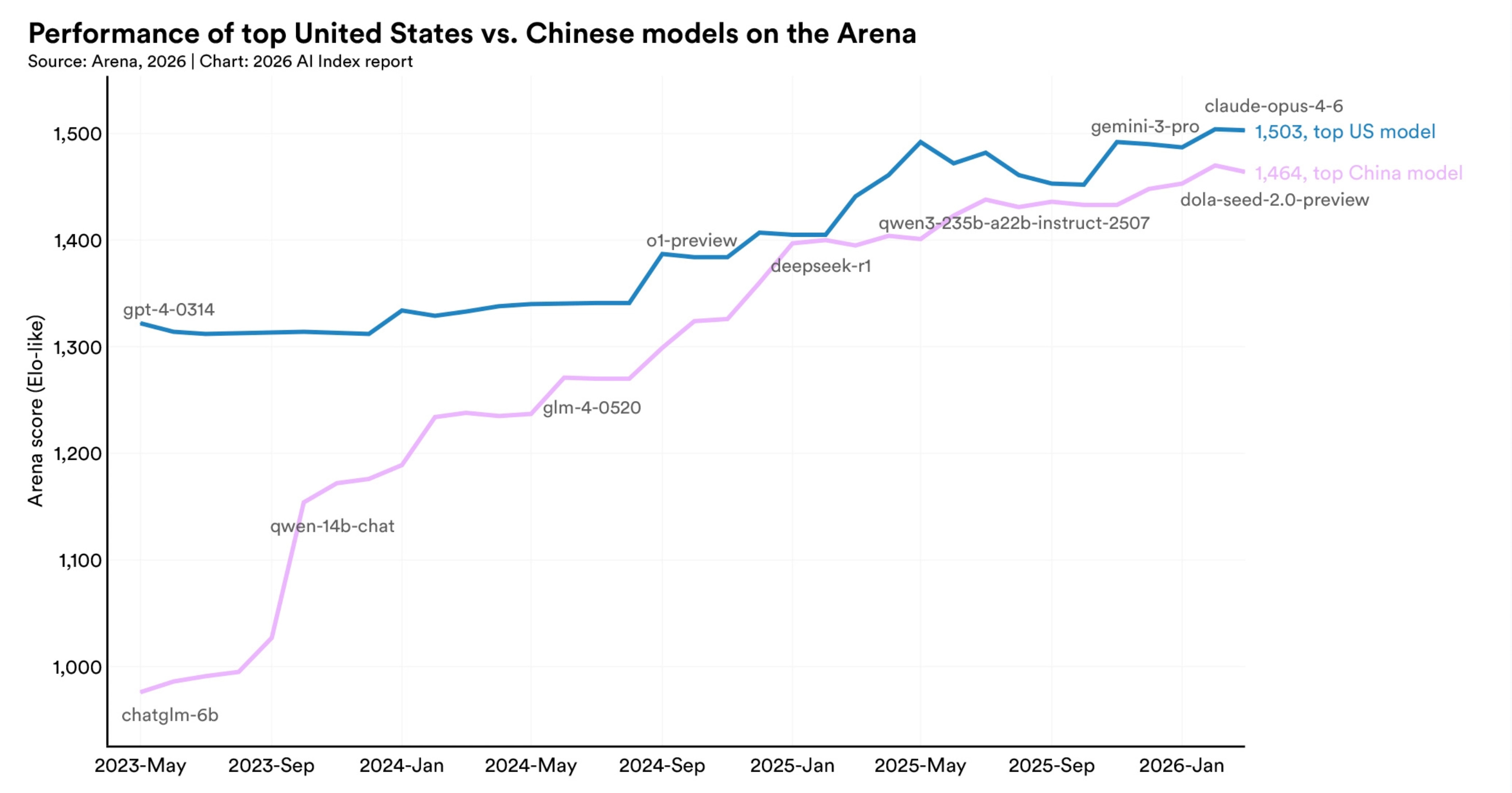

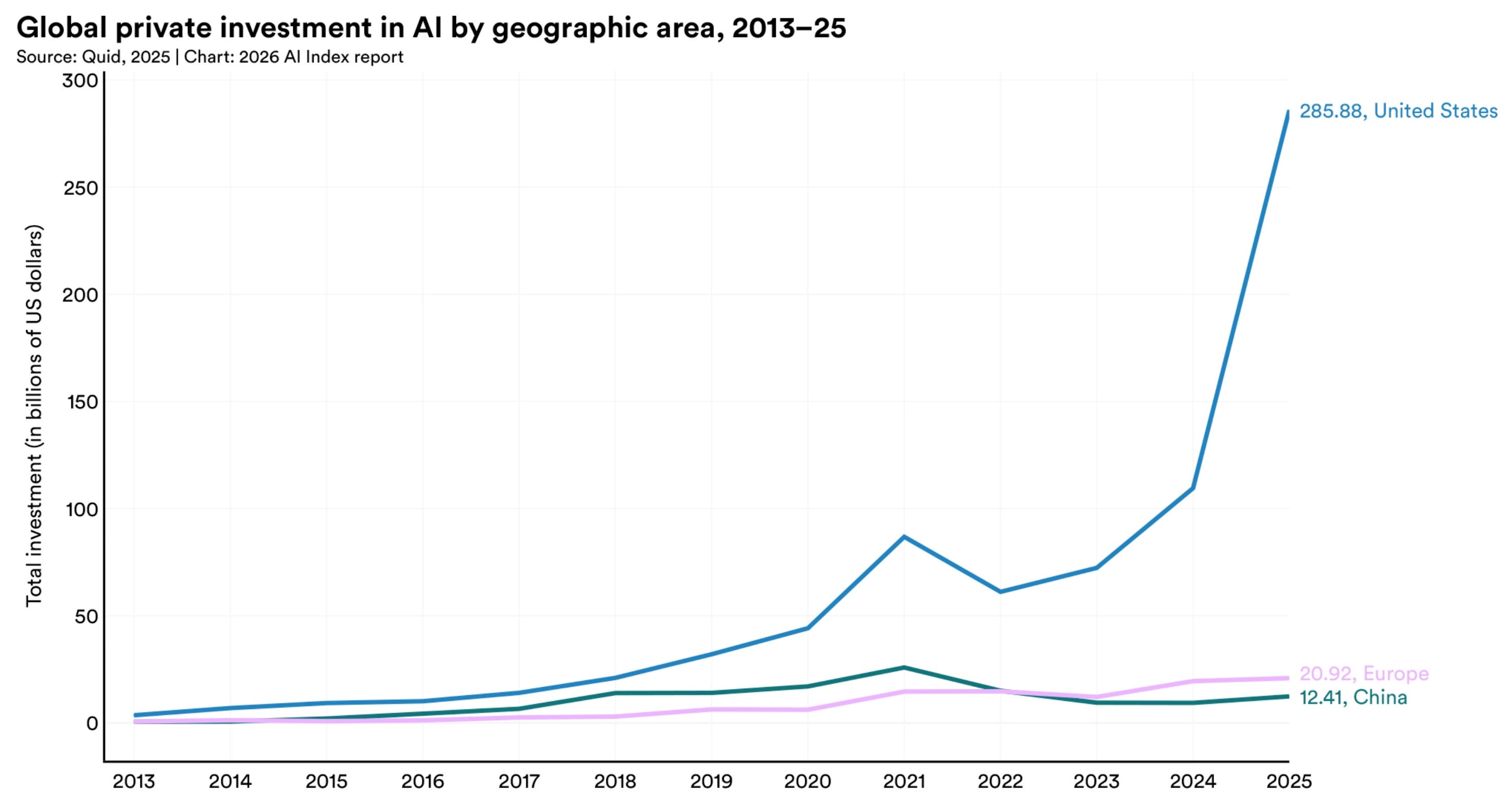

The long-standing assumption that the U.S. is far ahead in AI is no longer true in the same way.

The U.S. still leads in top-tier models and private investment

But China has closed the performance gap significantly

In some periods, Chinese models have matched or even led U.S. models

China dominates in research output, patents, and industrial deployment

At the same time, the entire AI supply chain depends heavily on a single chokepoint: TSMC in Taiwan, which manufactures the majority of advanced AI chips.

So while software is globalising, hardware remains highly concentrated, creating a very different kind of risk.

Another underappreciated shift is happening in talent.

Despite leading in funding and startups, the U.S. is losing its dominance in attracting global AI talent, with an 89% decline in researcher inflow since 2017. Meanwhile, countries like the UAE, Chile, and South Africa are seeing rapid growth in AI skill development.

This suggests the next wave of AI innovation may be far more geographically distributed than the last. But not everything is keeping pace.

This report highlights a growing gap between AI capability and AI responsibility.

AI incidents jumped sharply to 362 in 2025

Most companies report performance benchmarks - but not safety benchmarks

Improving one dimension (like safety) can degrade another (like accuracy)

In other words, we’re scaling our capability faster than we’re managing its consequences. And finally, there’s the perception gap.

AI experts are overwhelmingly optimistic - 73% believe it will positively impact jobs. But only 23% of the general public agrees. That 50-point gap reflects something deeper: people are experiencing AI differently than those building it.

Add to that fragmented global trust in institutions, and you get a landscape where technology is advancing faster than consensus around it.

Put all of this together, and the picture becomes clearer. AI isn’t one trend. It’s multiple curves compounding at once:

Capability is improving rapidly but unevenly

Adoption is spreading faster than any prior technology

Investment concentrating heavily in a few regions and companies

Talent and participation are slowly globalising

Governance and trust lag behind

For founders and investors, this changes how you read the market. It’s no longer about asking, “Is AI big?” That’s already settled.

The real questions are:

Where is the next layer of value forming?

Which parts of the stack are underbuilt relative to adoption?

And where are the bottlenecks that will define the next phase?

Because in cycles like this, the biggest opportunities don’t come from following the trend. They come from understanding where the trend is about to break next.

Do you really need Stanford or Harvard to build a unicorn?

There’s a strong belief in startups that the path to building a billion-dollar company runs through a handful of elite universities.

Stanford. Harvard. MIT. And to be fair, the data does show they matter.

In an expanded analysis covering unicorn founders from 2017 to 2025, Stanford’s Ilya Strebulaev tracked which universities consistently produce founders of billion-dollar companies.

Only three schools showed up in the top 10 every single year across all nine vintages: Stanford, Harvard and MIT

Stanford alone took the #1 spot in six out of nine years, which tells you how deeply embedded it is in the startup ecosystem.

But the more interesting insight isn’t that these schools dominate. It’s that they don’t dominate as much as people think.

When you zoom into the 2025 ranking, the picture becomes much more distributed:

Stanford and Harvard still lead

But schools like Cornell, UT Austin, Michigan, and UC San Diego are right there in the top 10

Public universities are consistently producing meaningful numbers of unicorn founders

The Ivy League advantage is real - but far less concentrated than brand perception suggests

Even historically, schools like Berkeley - which appeared in 8 out of 9 years - show that proximity to ecosystems can matter as much as prestige itself.

There’s also a global layer that often gets overlooked. A few non-US universities show up repeatedly across vintages: Tel Aviv University, Technion (Israel Institute of Technology) and University of Alberta.

These aren’t random appearances. They reflect something structural.

Israel continues to produce a disproportionate number of founders in deep tech and cybersecurity. Canada, especially through places like Alberta, is quietly becoming a major hub for AI research and talent.

So what does this actually tell you? The naive takeaway would be: “Top schools increase your chances.”

That’s true - but incomplete. The deeper takeaway is about the environment, not just education.

Top universities tend to provide:

Access to ambitious peers

Early exposure to cutting-edge research

Proximity to capital and startup ecosystems

A culture that normalises building companies

But those advantages are no longer exclusive. They’re increasingly being replicated across other universities and geographies. That’s why you’re seeing a broader distribution of founders over time.

For founders, this should be reassuring. Your university might influence your starting point - but it doesn’t define your ceiling.

What matters more is whether you can access the same underlying advantages:

Are you close to people building interesting things?

Are you plugged into emerging ideas and technologies?

Are you operating in an environment that compounds ambition?

Because the data is clear. Stanford, Harvard, and MIT may consistently show up. But they’re no longer the only places where unicorn founders are built. And over time, that gap is only getting smaller.

🤝 PARTNERSHIP WITH US

Get your product in front of over 115,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

SOMETHING MORE

🧩 Frameworks & insightful posts

Is your AI feature quietly killing your saas margins?

Most founders think about AI like a product upgrade. Better outputs. Better UX. Higher engagement.

But very few think about what it’s doing to their P&L.

Ben Murray (The SaaS CFO) recently highlighted a mistake that’s becoming common across AI-native and AI-enabled SaaS companies: treating AI costs like traditional SaaS COGS.

That assumption breaks your financial model faster than you expect.

Traditional SaaS was built on a simple foundation - high gross margins and low marginal cost.

You build the product once, serve many customers, and as you scale, your margins expand. That’s why 70-80% gross margins became the benchmark.

AI changes that dynamic. Every prompt, every generation, every workflow now carries a real, variable cost - inference, routing, vector databases, infrastructure. What used to be mostly fixed now behaves like a usage-sensitive cost layer.

And the impact is already showing up in the data.

Traditional SaaS: ~70–80% gross margins

AI-heavy SaaS (2026 estimate): ~52% gross margins

That gap isn’t small. It’s structural. The tricky part is how quietly this happens.

Teams ship AI features, see usage spike, celebrate adoption… and only later realise their cost to serve has fundamentally changed.

A simple example makes this clear.

You have a SaaS product doing $100 in revenue with $20 in COGS → 80% margin.

Now you layer AI features that add $15 in variable cost.

Same revenue. New COGS = $35. Your margin drops to 65% - instantly.

And that’s before: heavy users scale usages, poor prompt design increases cost, expensive models get overused, and pricing doesn’t reflect usage.

You’ve improved the product - but weakened the business.

This is why AI COGS is not just a finance detail. It’s the core lever that affects everything downstream: CAC payback, burn efficiency, Rule of 40 and ultimately, valuation

If gross margin compresses, every other metric gets tighter.

Where most companies go wrong is in visibility. They bury AI costs inside a generic “hosting” or “DevOps” bucket, which makes it impossible to answer a critical question:

What is the actual margin of the AI-driven part of the product?

That’s why the structure of your P&L suddenly matters a lot more. At a minimum, you need clarity across:

revenue streams (subscription vs usage vs services)

corresponding COGS layers

margins by each revenue stream

Because what’s happening in many companies right now is:

legacy SaaS → still high margin

AI layer → materially lower margin

And the blended number hides the problem.

Another shift that founders underestimate is pricing.

If your cost scales with usage, your pricing has to acknowledge it - even if you don’t expose raw token pricing. The models that are emerging look like:

platform fee + usage layer

tiered usage buckets or credits

overage pricing or soft caps

feature-based packaging for heavier AI workflows

The goal is simple: price on value, but protect against heavy usage that destroys margin.

Because AI cost problems don’t show up for average users. They show up in power users and edge cases.

But even with pricing fixes, investors don’t expect perfection right now. They expect clarity. What matters is whether you can show a credible margin roadmap:

better model routing

using smaller models where possible

prompt optimization

caching and infra efficiency

better packaging and higher ACVs

The point isn’t “we’ll get back to 80% margins tomorrow.” It’s showing you understand the economics and are actively improving them.

One subtle but important metric shift here: Don’t just track average cost. Track distribution.

top-decile users vs median users vs low-usage users

Because a small group of heavy users can quietly destroy your margins while averages still look fine.

Sp, AI is not just a product decision. It’s an economic shift. You can build something far more valuable and still end up with a worse business if you don’t adjust your model.

So the right questions aren’t: “Do customers want this feature?” or “Is adoption growing?”

They are:

Where does this sit on the P&L?

How does it change our gross margin?

Is pricing aligned with usage and cost?

Because the companies that win in AI SaaS won’t just be the ones shipping the fastest.

They’ll be the ones who understand the economics well enough to scale it profitably.

Is entrepreneurship actually safer than a 9-5 in the age of AI?

For years, the default advice was simple: take the stable job, avoid the risk, and maybe start something on the side later.

That logic is starting to break.

A recent analysis by Shopify’s Data Science team - based on millions of merchants across 175 countries - paints a very different picture. The data doesn’t just suggest that entrepreneurship is growing. It suggests the risk equation itself is shifting.

The first signal is hard to ignore.

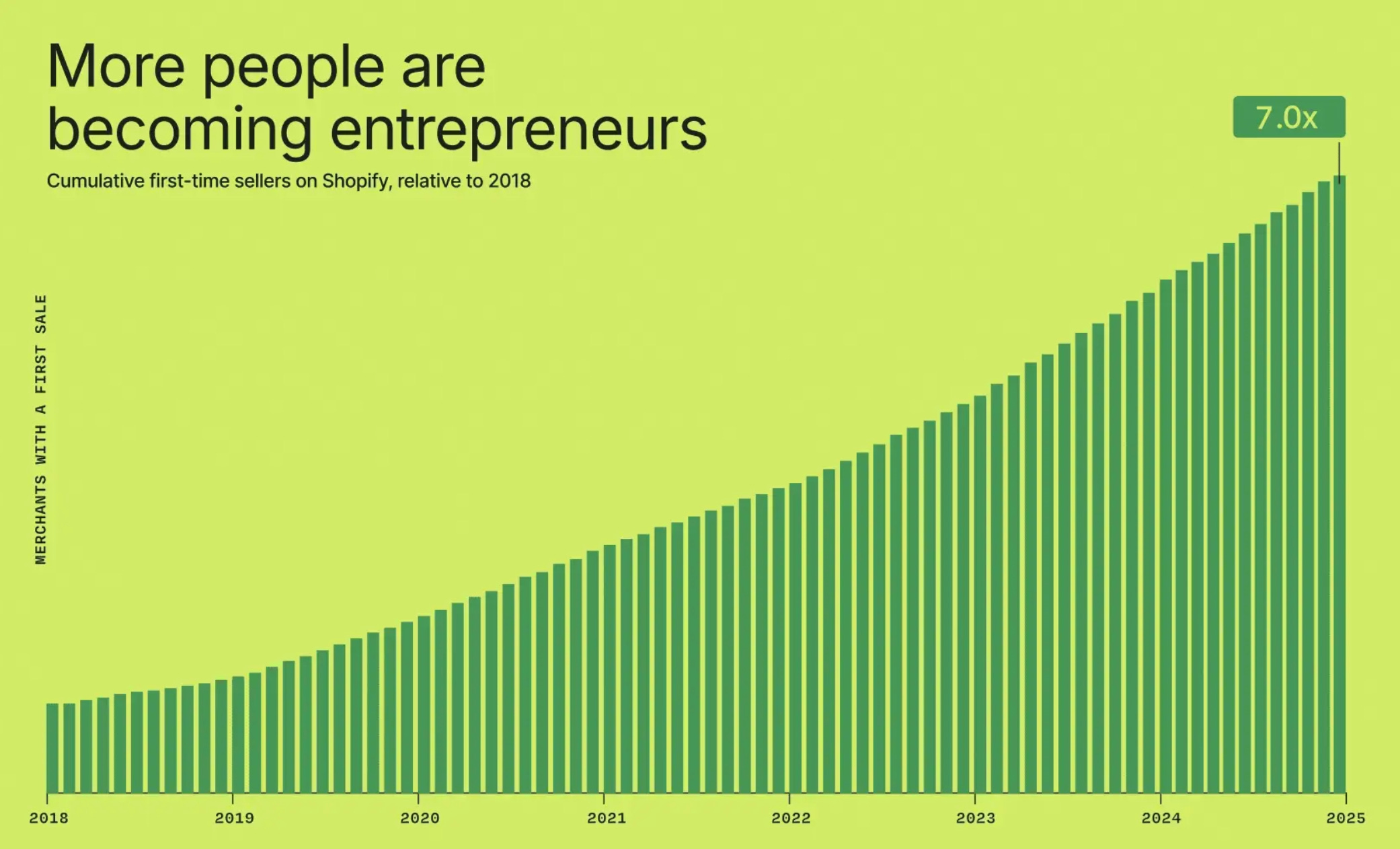

More people are starting businesses than ever before.

Since 2018, the number of Shopify merchants making their first sale has increased 7x. And this isn’t happening in isolation. It’s happening alongside a weakening traditional job market. In 2025 alone, U.S. companies announced 1.2 million job cuts, with AI cited as the primary reason in a significant share of them.

You don’t need to over-interpret the causation here to see the pattern:

Traditional employment is getting more uncertain

Entrepreneurship is getting more accessible

When you make something easier, you get more of it. That’s exactly what’s happening with building businesses. But the more interesting insight isn’t just that more people are starting.

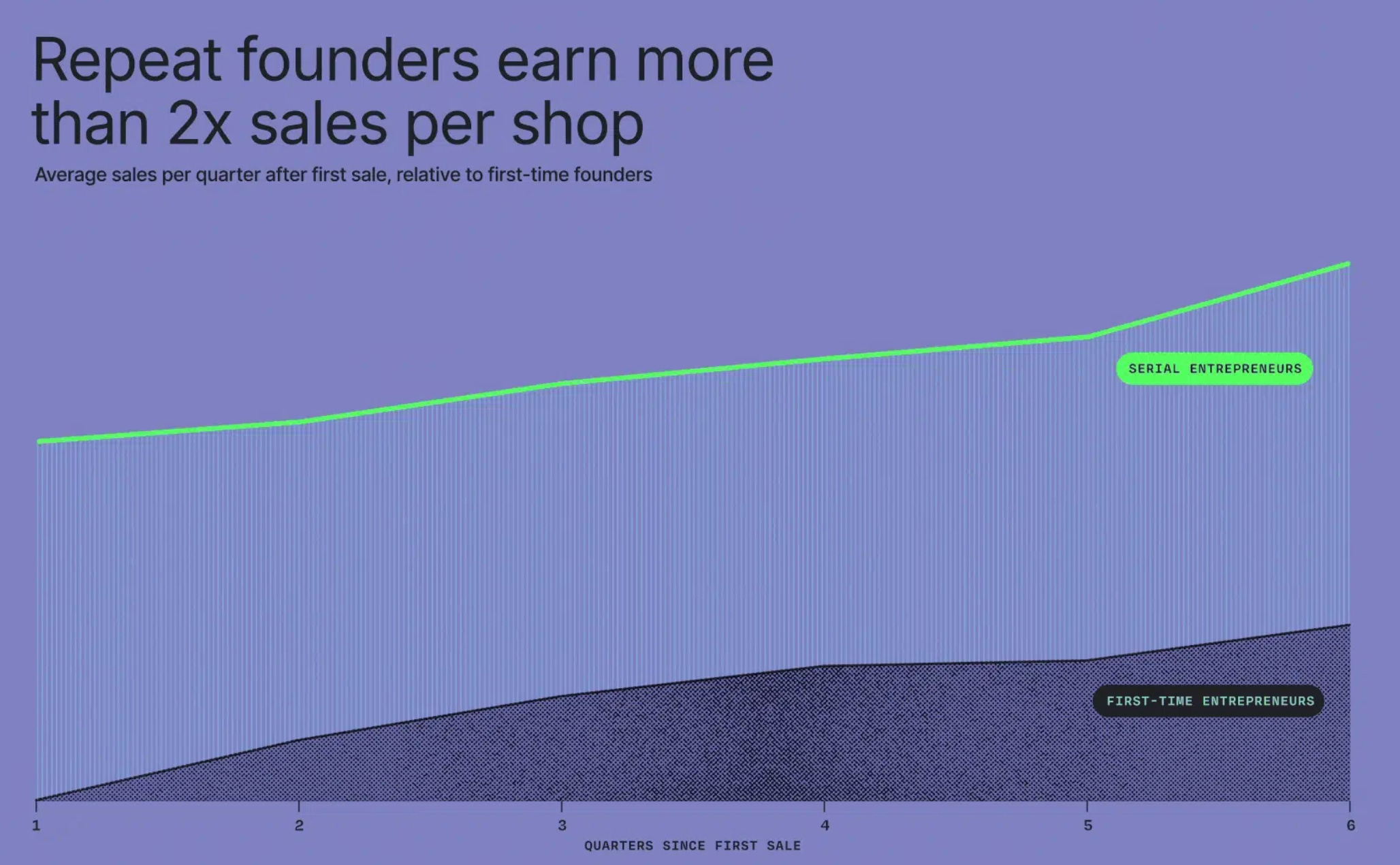

It’s that people who do it again get significantly better.

Repeat founders on Shopify generate more than 2x the sales per shop compared to first-time founders. And this aligns with broader research - entrepreneurial performance compounds over time.

This is where the “entrepreneurship is too risky” argument starts to weaken.

Because, unlike traditional jobs - where skills can become obsolete - entrepreneurial skills tend to compound:

finding customers

identifying opportunities

operating under uncertainty

building distribution

These don’t reset. They stack.

The first venture is the hardest. But each one after that becomes more informed, faster, and often more successful.

The third shift is even more subtle, but powerful.

Entrepreneurs aren’t just starting more - they’re earning more over time.

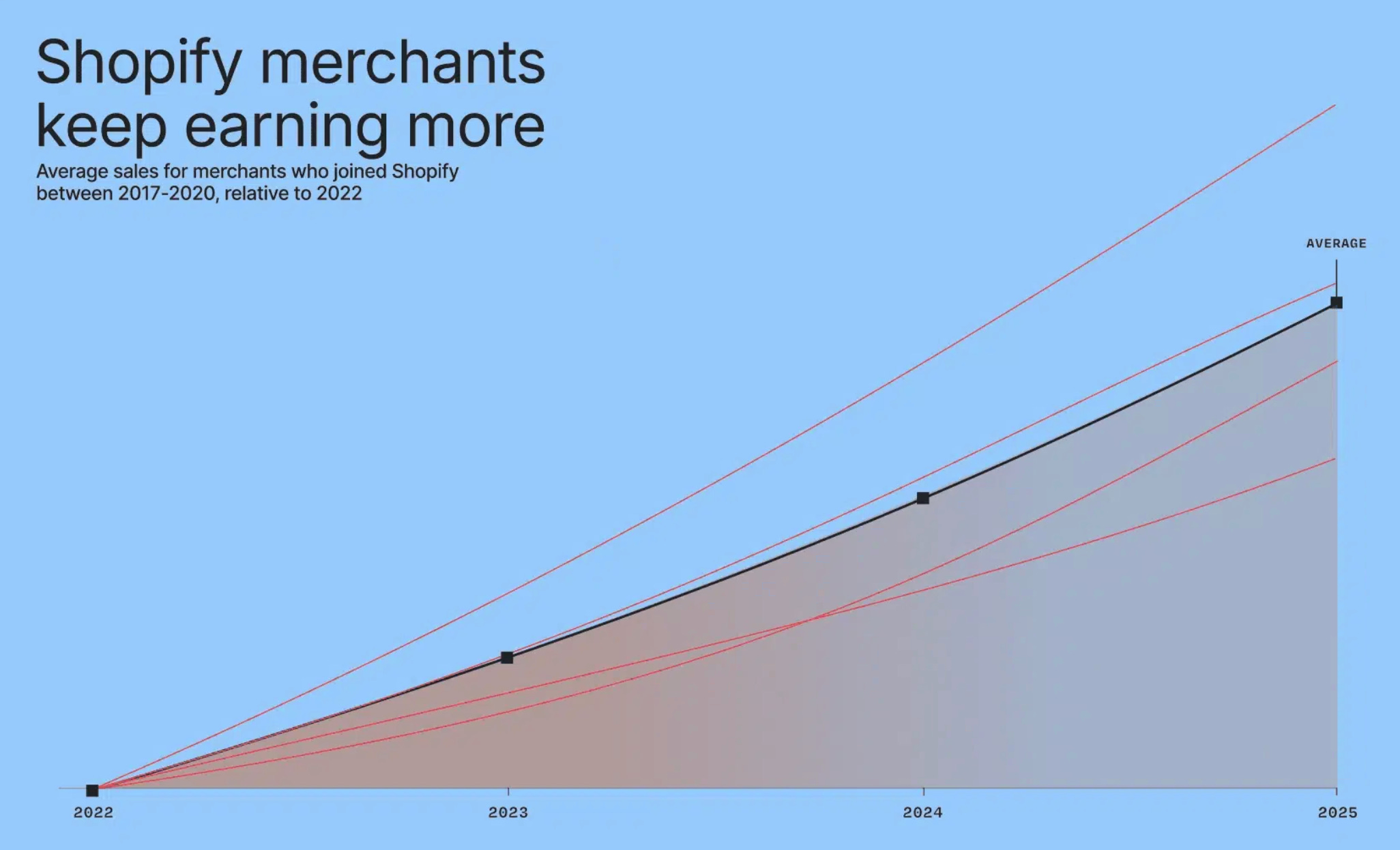

Shopify merchants who started between 2017 and 2020 saw their average sales grow 25% between 2022 and 2025. This isn’t just individual improvement. It’s also because the underlying market is expanding.

E-commerce itself has grown from 14% of global retail in 2019 to over 20% in 2025, and Shopify now powers more than 14% of U.S. e-commerce.

So founders today aren’t fighting for a fixed pie. They’re building inside a growing one.

And that’s the real shift most people are missing. Entrepreneurship used to be risky because:

Tools were limited

Distribution was expensive

operations were complex

Now, a lot of that friction has collapsed. AI tools, better logistics, global payments, and platforms like Shopify have effectively turned entrepreneurship into something closer to a skill-driven system rather than a pure gamble.

So the takeaway isn’t that entrepreneurship is easy. It’s that the definition of “safe” is changing.

The traditional path is no longer as stable as it once was. And the alternative path - building something of your own - is no longer as unpredictable as it used to be.

More people are choosing it. The ones who repeat it are getting better at it. And over time, they’re earning more from it.

The safest job used to be working for someone else. Now, increasingly, it might be learning how to build for yourself.

Is the traditional seed investing playbook already broken?

For years, early-stage investing followed a simple belief:

Invest early. Invest cheap. Diversify widely. And let one 1000x outlier return the fund.

That model is quietly breaking.

Lucas Vaz recently laid this out using fresh data, and the shift is hard to ignore. Seed valuations have exploded. The top 5% of seed rounds are now regularly happening at $150M–$175M+ valuations, up nearly 3x in a short period. Even median-ish rounds have moved up meaningfully.

At the same time, something else is happening, and it’s even more important. The biggest winners are no longer returning what they used to.

Take the OpenAI example.

Early investors collectively put in around $10M and are now sitting on roughly $1.4B in paper value. That’s ~140x.

In any other era, that sounds incredible. But for venture math, it’s not enough.

If your fund had only a small position in the biggest company of the decade, even a 140x outcome may not return your fund meaningfully. The combination of high entry prices, heavy dilution, and massive capital flowing into winners is compressing returns at the very top.

Which leads to a non-obvious conclusion:

The era of 1000x outcomes isn’t disappearing because companies are weaker.

It’s disappearing because the structure of venture has changed.

Most emerging managers react to this the same way. They go earlier. They go cheaper. They try to find $5M0$10M entry points where big funds aren’t competing.

That feels like a smart adjustment. Lucas argues it’s a trap. Because the market isn’t just getting expensive - it’s splitting.

What’s happening is a clear bifurcation of the venture ecosystem. At the top, a small set of companies:

raise at high valuations

have real traction or strong signals early

attract top-tier capital immediately

compound advantages through network, talent, and follow-on access

These are not “overpriced hype deals.” They’re increasingly predictable winners with clearer paths to scale.

Below that is a much larger pool of companies that look cheap - but structurally struggle to break out. They might go from: $5M → $25M → $100M on paper

But paper markups are not real outcomes. Most of these companies never reach meaningful liquidity - not because they’re bad, but because:

Capital is concentrating on fewer winners

Talent follows those winners

The bar for Series A keeps rising

Exit markets (IPO/M&A) are tighter than before

So what looks like a “cheap entry” is often just a value trap. This is where most portfolio strategies break. The old model said: diversify broadly and wait for one outlier.

But if outliers now return 50–150x instead of 1000x, that math stops working. Because:

a 3% position needs ~30x+ to return the fund

A small ownership in a winner isn’t enough anymore

Spreading capital across 40–50 bets dilutes impact

So the shift isn’t just about valuation. It’s about portfolio construction.

The new reality is much simpler - and harder. You need to make money on 10–20x outcomes. Not hope for a miracle.

That changes how you think about everything:

price becomes relative to quality, not absolute cheapness

Concentration matters more than ownership %

conviction matters more than diversification

Owning 10% of a mediocre company doesn’t matter. Owning 2-3% of a real $5B+ outcome can.

This is why “fund size is your strategy” is also flawed thinking. Smaller funds often default to lower prices to get higher ownership. But ownership alone doesn’t create returns. What matters is:

the quality of the company

probability of a large outcome

And how much of your fund is allocated to it

In every other asset class, this is obvious. In venture, it’s often ignored. So what actually works now? The path forward is narrower — but clearer.

You need to operate in two lanes at once:

Get into the best companies you have the right to access

Even if they’re expensive. Even if ownership is lower initially. Because these are the only assets with real path-dependency and liquidity potential.

Find high-conviction opportunities before the market sees them

Your edge gives you early insight and then helps those companies become “obvious” to the next round of capital.

And most importantly - size your bets correctly. Because the biggest mistake now isn’t missing deals. It’s under-allocating to the right ones.

So, the old venture playbook optimised for randomness. Cheap entries. Wide portfolios. Hope for a breakout. The new environment rewards precision. Fewer bets. Higher conviction. Willingness to pay for quality.

Because in this market, picking well isn’t just an advantage anymore. It’s the entire game.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Treehub & AI Health Fund, U.S.-based healthcare-focused initiatives launched by Mary Minno, are building an accelerator + venture model to back early-stage AI healthcare startups. (Link)

Sideline Group, a NYC-based investment firm that partners with brands and experiences at the intersection of consumer, sports, and media & entertainment, closed its debut fund, Sideline Group Fund I, with $155 million in committed capital. (Link)

Accel, a global venture firm, has raised $5B in fresh capital to back late-stage startups, with $4B allocated to its Leaders Fund and $650M to a sidecar vehicle. (Link)

A‑Street, a Bentonville, Ark.-based multi-stage investment fund focused on improving PK-12 student learning and achievement, announced a $675m capital raise. (Link)

Eclipse, a Palo Alto, CA-based venture capital firm, raised $1.311 billion for two funds. (Link)

Futurepresent, a NYC, Berlin, and Munich, Germany-based venture capital firm backing AI startups in the US and Europe, launched with its first $300M vehicle. (Link)

Zero Shot, a U.S.-based VC fund founded by former OpenAI leaders, has raised $20M in its first close toward a $100M target to invest in early-stage AI startups. (Link)

New Startup Deals

10x Science, a San Francisco, CA-based AI protein research startup, raised $4.8M in Seed funding. (Link)

Nox Mobility, a Berlin, Germany-based night train company, raised €2M in Pre-Seed funding. (Link)

VAST Data, a NYC-based AI operating system company, raised ~$1B in Series F funding at a $30B valuation. (Link)

Ray Therapeutics, a Berkeley-based biotech company, raised $125M in Series B funding. (Link)

Coral, a NYC-based healthcare automation platform, raised $12.5M in funding. The round was led by Lightspeed and Z47. (Link)

Ultralight, a San Francisco-based AI healthcare OS startup, raised $9.3M in Seed funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Partner 18, Healthcare - a16z | USA - Apply Here

Associate - DN Capital | Germany - Apply Here

Investment Intern - DTCP | UK - Apply Here

Venture Scout - First Momentum Venture | UK - Apply Here

Analyst, Global Investment Team - 500 Global | USA - Apply Here

Associate, Data Operations - Iconiq Capital | USA - Apply Here

Investor - AI - Samsung Next | USA - Apply Here

Finance Associate - RA Capital | USA - Apply Here

Fund Controller - NFX | USA - Apply Here

Vice President, Investor Relations - General Atlantic - Apply Here

Senior Associate - RA Capital | USA - Apply Here

PE & VC Partner Manager - Dealhub | UK - Apply Here

Partner 22 -a16z | USA - Apply Here

Infra / Platform Engineer - Pear VC | USA - Apply Here

Associate / Senior Associate - Stepstone Group | Italy - Apply Here

Investment Analyst - Lunicorn Venture | UK - Apply Here

PARTNERSHIP WITH US

Get your product in front of over 115,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

Funny thing about this chart. Every founder I know picks the line that confirms whatever they already decided to build on.

Claude shop? "Look at that lead." Gemini shop? "Look at that trajectory." Open source bet? "Look how fast Qwen closed the gap."

The chart everyone should actually be reading is the one that isn't here. The one showing what customers will pay per query as models converge. Arena scores climb. Willingness to pay for the marginal Elo point doesn't.

The real margin killer isn't your AI feature. It's building on a capability that's expensive today and commodity tomorrow.