The $20 Trillion Blind Spot: Bezos Just Showed You Where to Build.

AI Has Conquered Software. The $20 Trillion Physical World Is Next. Almost Nobody Is Building for It.

👋 Hey, Sahil here - welcome to this edition of Venture Curator, where we break down how great startups grow, how top investors think, and what’s shaping the future of tech.

P.S. Get access to 100+ startup & VC resources, investor databases, fundraising templates, 150+ premium archive posts and exclusive startup research - all in one place.

📜 DEEP DIVE

The $20 Trillion Blind Spot: Bezos Just Showed You Where to Build.

Something unusual is happening right now in the world of venture and technology, and most people are looking at the wrong part of it.

This week, Jeff Bezos’s startup Prometheus raised $12 billion at a $41 billion valuation. The backers weren’t just Andreessen or Sequoia.

They were JPMorgan Chase, Goldman Sachs, and BlackRock. The three largest financial institutions on the planet are now writing billion-dollar venture checks.

The company has 150 employees - no public product.

And a goal that sounds like science fiction: build an “artificial general engineer” - AI that can design jet engines, drug compounds, and complex physical systems the way GPT-4 writes emails.

Everyone covered the fundraise. Almost nobody asked the obvious follow-up question.

If this is where $41 billion of smart money is pointing - toward automating the physical world - then why are there almost no startups building the infrastructure that world requires?

This is not a rhetorical question. We spent a few days pulling the data. What we found was a gap so large it is hard to believe nobody is talking about it.

Three industries - construction, pharma manufacturing, and power grid infrastructure- together represent more than $20 trillion in annual economic activity. They employ hundreds of millions of people globally. They are the literal foundation of how civilisation runs. And they are about to face the most significant technological disruption since the Industrial Revolution.

The number of AI-native startups building for them? Relative to their size, negligible.

This is either the most obvious trap in tech or the most obvious opportunity. We believe it is the latter. This issue explains why, shows you who is moving, and maps what needs to be built.

We are going to cover:

The World Right Now: Why physical infrastructure is suddenly the centre of everything.

The Productivity Paradox: How big these industries are and how untouched they’ve been.

The Startup Density Gap: The data showing where founders have gone, and where they haven’t.

Why Nobody Has Built Here: The real structural reasons and why they’re moats, not blockers.

The Prometheus Signal: What a $41B bet tells founders who can’t raise $12B.

Founders to Watch: Who is actually moving in these spaces right now.

The Unlock Map: What needs to be built, in what order, in each industry.

The World Right Now

It is June 2026. Here is what the macro picture looks like.

AI has won the software layer. The race for foundation models is functionally over as a competition of new entrants - OpenAI, Anthropic, Google DeepMind, and a handful of others have consolidated the top.

Enterprise software is being rebuilt around AI agents. Developer tools, legal research, financial analysis, customer support - these are being automated faster than most analysts predicted two years ago.

The next frontier is physical. And the physical world is not ready.

The data centre crisis.

Large technology companies are expected to commit more than $1 trillion in infrastructure spend in 2025-2026 alone.

As of early 2026, 190 gigawatts of hyperscale data centre capacity has been announced across 777 projects globally - roughly 148 GW planned, 21 GW in construction, 12 GW already operational.

The problem:

Data centres can be built in 12 to 18 months. Connecting them to the power grid takes five to seven years.

Of the 110 data centre projects slated to open in 2025, more than a quarter were delayed - not because of chips or software, but because of power, permitting, and construction. The physical world is the bottleneck.

The infrastructure spending boom.

Governments globally are deploying historic levels of capital into physical infrastructure.

The US Bipartisan Infrastructure Law committed $1.2 trillion.

The EU’s NextGenerationEU fund is deploying €800 billion.

India’s infrastructure spend has grown at double-digit rates.

The Middle East is building entire cities.

The global construction market, already at $17 trillion in 2025, is projected to reach $19.6 trillion by 2032. Every one of those trillions requires engineering, permitting, construction, and supply chain work that is still largely done by hand.

The pharma manufacturing gap.

AI has revolutionised drug discovery. Companies like Recursion, Insilico, and Formation Bio have used machine learning to compress what used to be decade-long molecule discovery processes into years or months. Formation Bio reportedly cut clinical trial lead times by half.

AI pharma investment has crossed $485 billion in total disclosed capital. But the factory- the industrial process of actually making drugs at scale, maintaining quality, releasing batches, and meeting FDA compliance- has barely changed. Most facilities still run on paper. The discovery is AI-native. The manufacturing is 1970s infrastructure.

The labour shortage.

Across construction, energy, and advanced manufacturing, the skilled workforce is shrinking faster than industries can replace it. AEC (architecture, engineering, and construction) has 440,000 unfilled vacancies in the US alone, nearly double the 2019 level. Energy infrastructure is facing a similar wave of retirement.

The case for AI automation in these sectors is not theoretical - it is driven by an acute and worsening human capital problem.

This is the context in which Bezos raised $12 billion. He is not making a speculative bet. He is looking at $20+ trillion of industries, a global infrastructure boom, an AI model that is ready to automate engineering tasks, and a labour market that desperately needs it.

The bet is not that physical AI will eventually matter. The bet is that it matters right now.

The Productivity Paradox

Now consider what these industries look like from the inside.

There is a number that should bother every founder in tech. Since 1945, productivity in US manufacturing has grown by roughly 1,500%. Agriculture transformed beyond recognition. Retail, logistics, finance, media - all reshaped by digital tools, often multiple times over.

Construction? The Richmond Federal Reserve’s 2025 research found that US construction labour productivity fell more than 30% from 1970 to 2020 - a fifty-year decline- while the rest of the American economy doubled output per worker.

A 2022 academic paper estimated that the construction sector alone accounted for about one-third of the decline in US trend GDP growth since World War II. The compounding cost is approximately $1 trillion in lost value every five years.

McKinsey translates this into opportunity: if construction productivity merely caught up with the rest of the economy, the industry’s annual value added would rise by $1.6 trillion - enough to meet half the world’s annual infrastructure needs and boost global GDP by 2%.

This is not a sector that tried technology and found it didn’t work. It is a sector that technology has almost entirely skipped. AEC companies spend just 1 to 2% of revenue on technology - versus 3 to 5% across industries generally. The industry has been under-investing in software for so long that the gap between what is possible and what exists is measured not in years but in decades.

Pharma manufacturing tells a similar story. While AI drug discovery companies collectively raised nearly $1 billion in disclosed rounds just in the 12-month period to mid-2026, the broader pharma digital manufacturing market - estimated at $42 billion globally - is being served primarily by legacy enterprise vendors. Most pharmaceutical production facilities run batch release processes that involve manual review of paper records.

A contamination event or quality failure is caught by a human reading a printout. The AI revolution in pharma has been entirely front-loaded toward discovery and has barely touched production.

And the grid: the US interconnection queue - the waiting list for new projects to connect to the power grid - currently holds more than 2,400 gigawatts of pending projects.

For scale, total US generating capacity today is roughly 1,200 GW. There is twice the current grid sitting in a queue, waiting.

The bottleneck is not technology, not capital, not demand. It is the absence of modern software systems to model, manage, and accelerate the process of connecting new infrastructure to existing infrastructure.

The Startup Density Gap

Here is the most precise way to see the opportunity.

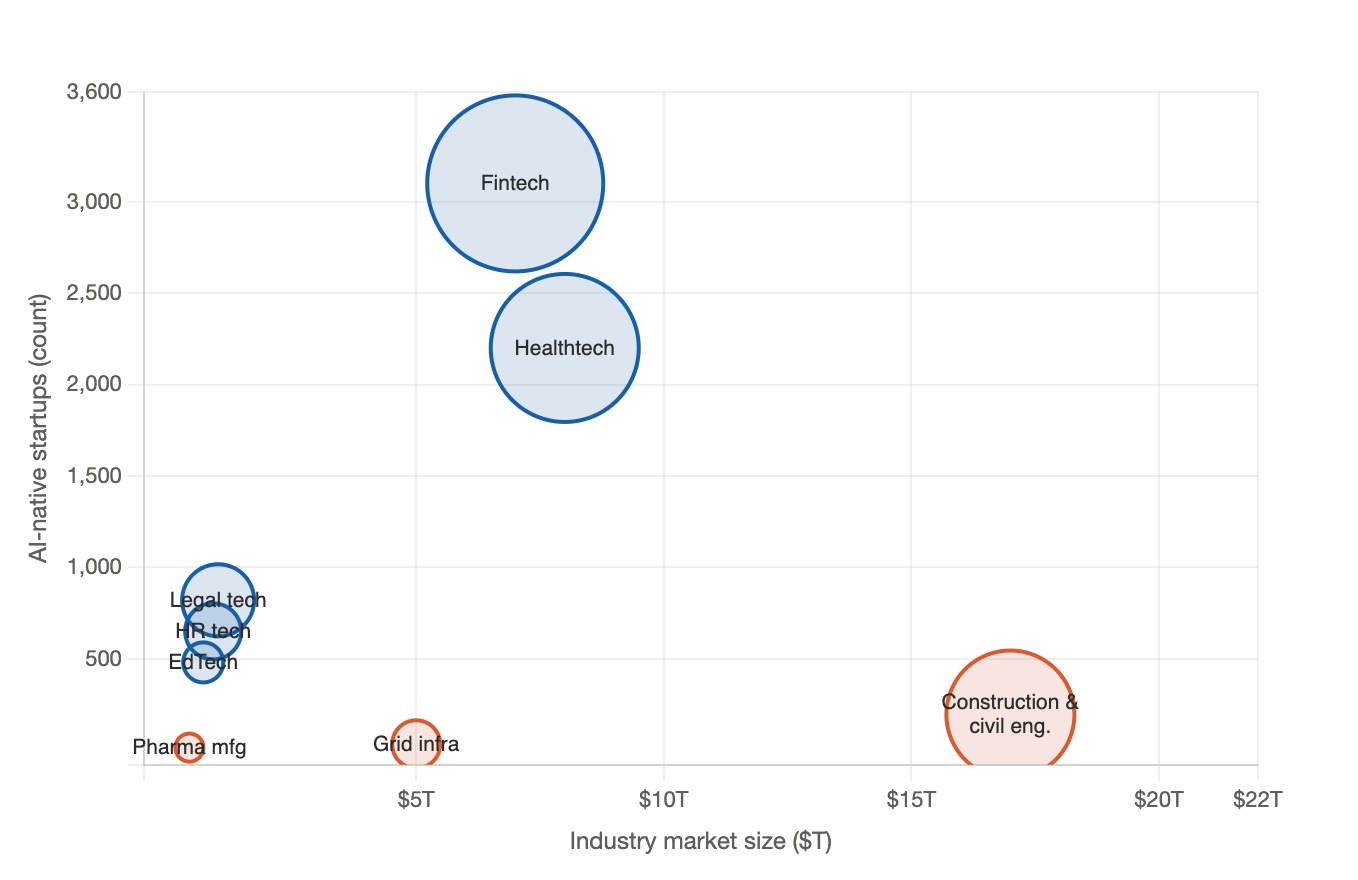

Take any major industry. Plot it on two axes: the size of that industry against the number of AI-native startups actively building for it. The result is a map of where founders have gone and, more importantly, where they haven’t.

Fintech: multi-trillion-dollar industry, thousands of AI-native companies.

Healthtech software: same.

Legal tech, marketing automation, enterprise SaaS, developer tools - all densely populated with venture-backed AI-native startups, across every subsegment, at every stage.

Now look at construction, pharma manufacturing, and grid infrastructure. Enormous industries. Tiny startup footprints.

The numbers make this concrete, which makes it even more interesting: