The dilution myth founders still believe. | Wispr Flow’s framework to reach 100,000+ daily users.

3 curves that quietly decide if your startup scales or collapses & These SaaS fundraising benchmarks officially dead in the AI era

👋 Hey, Sahil here — Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

The dilution myth founders still believe.

The $20B exit era: Why venture’s biggest outcomes keep getting bigger.

Venture Performance: Early TVPI can lie; DPI tells a different story

Frameworks & insightful posts :

Wispr Flow’s framework to reach 100,000+ daily users - The CEO’s exact consumer playbook.

Are the old SaaS fundraising benchmarks officially dead in the AI era?

The 3 curves that quietly decide if your startup scales or collapses.

FROM OUR PARTNER - FRAMER

🤝 Launch fast. Design beautifully. Build your startup on Framer — free for your first year.

First impressions matter. With Framer, early-stage founders can launch a beautiful, production-ready site in hours. No dev team, no hassle. Join hundreds of YC-backed startups that launched here and never looked back.

Pre-seed and seed-stage startups new to Framer can enjoy:

One year free: Save $360 with a full year of Framer Pro, free for early-stage startups.

No code, no delays: Launch a polished site in hours, not weeks, without hiring developers.

Built to grow: Scale your site from MVP to full product with CMS, analytics, and AI localisation.

Join YC-backed founders: Hundreds of top startups are already building on Framer.

Apply to claim your free year →

🤝 PARTNERSHIP WITH US

Get your product in front of over 103,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

The dilution myth founders still believe.

If you’re being told that “30% at seed is just the market,” it’s worth pausing.

In a recent post, Peter Walker shared fresh Carta data analysing 3,112 primary priced VC rounds raised by US startups in 2025. The goal was simple: look at what founders are actually selling in early-stage rounds, not what people assume they are.

The headline? Heavy early dilution is far less common than startup Twitter makes it sound.

At seed:

Median dilution sits at 20% for software and 21% for deep tech

Fewer than 10% of software seed rounds involved selling 30% or more

Deep tech has a wider distribution, with hardware, biotech, and energy deals still showing a longer tail of higher dilution

Important nuance: this excludes bridges, extensions, and SAFE conversions. These are clean, primary-priced rounds.

As companies move up the stack, dilution continues to compress.

At Series A:

Medians: 18% (software), 22% (deep tech)

AI-native companies are pulling software medians lower due to faster valuation expansion

By Series B:

Medians fall to 14% (software) and 16% (deep tech)

That’s meaningfully lower than what many founders expect when walking into negotiations.

So why does it feel like dilution is rising?

A few structural shifts explain the disconnect.

First, AI valuations are moving faster than round sizes. When valuation growth outpaces capital raised, the percentage sold naturally shrinks.

Second, round consolidation. Fewer companies are raising, but those that do are often strong, competitive deals. Multiple term sheets tend to push dilution down, not up.

Third, market standardisation. While geography still matters (a Silicon Valley deal isn’t identical to one in Dallas), early-stage norms are converging. Aggressive structures are harder to push through.

And importantly, risk isn’t quietly being shifted elsewhere.

Only 3% of Seed and Series A deals in 2025 included liquidation preferences above 1x. Participating preferred and other heavy structures are increasingly rare at the early stage.

That doesn’t mean you reject a 30% deal blindly. If it’s your only term sheet and you need the cash, survival matters more than optimisation.

But it does mean this: “that’s just the market” is no longer a convincing explanation for heavy dilution.

The market is competitive. Capital is concentrated. And clean deals are more common than many founders think.

Go into negotiations informed, not intimidated. But still, many founders failed in negotiating this funding dilution, so with the help of leading founders and investors, we have created a detailed all-in-one guide on equity dilution decision.

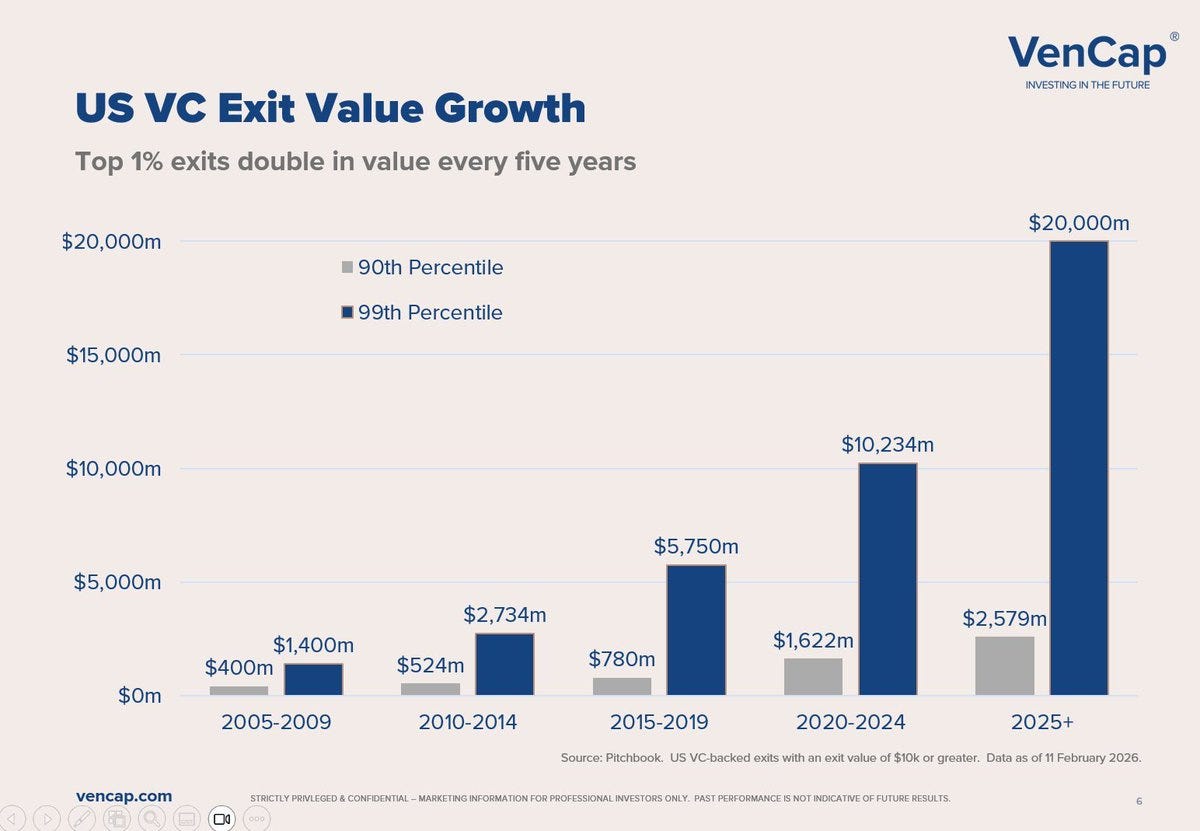

The $20B exit era: Why venture’s biggest outcomes keep getting bigger.

Every few years, someone says the venture is overheated. And then the data quietly does something else.

Garry Tan recently shared VenCap data (sourced from PitchBook US VC-backed exits) showing something most founders don’t internalise:

The top 1% of startup exits have doubled in value roughly every five years for the past two decades.

From 2005–2009, the 99th percentile exit was around $1.4B.

2010–2014: about $2.7B.

2015–2019: roughly $5.7B.

2020–2024: $10.2B.

2025 and beyond: projected near $20B.

That’s almost a 10x expansion in the ceiling of outcomes in 20 years.

Even the 90th percentile exists have grown materially, but the real acceleration is happening at the extreme right tail. The biggest companies are getting disproportionately bigger. Venture is not just growing; it’s stretching.

This matters more than most founders realise.

When seed valuations moved from $3–5M a decade ago to $15–20M today, it wasn’t just hype. Pricing moved because outcomes moved. If investors underwrite $10B–$20B potential exits instead of $1B outcomes, the math at entry changes.

But here’s where it gets nuanced.

The ceiling is rising — but dispersion is widening.

Outliers are compounding — average outcomes are not.

Capital is clustering around companies that look like category leaders.

That’s why it feels harder in the middle of the market.

You’re either building something that plausibly fits the new right tail global distribution, AI leverage, infrastructure scale, network effects or you’re fighting for capital in the “good but not dominant” zone.

Another shift behind these numbers: leverage.

Small teams today can build what used to require hundreds of people. AI, APIs, cloud infrastructure, and distribution platforms compress time and cost. A 10-person team generating $50M+ in revenue is no longer absurd. That mechanical leverage pushes the upper bound of outcomes higher.

And when the upper bound rises, everything upstream shifts:

Investors tolerate higher early valuations.

Mega-funds move earlier.

Ownership gets more competitive.

Founders are pressured to think bigger, earlier.

The uncomfortable truth is this: venture returns are increasingly dependent on extreme outliers. And those outliers are now operating at a scale that would have looked impossible 15 years ago.

So the real strategic question for founders isn’t “Is the market too hot?”

It’s this:

Are you building something that can sit inside that expanding right tail or something that peaks in the middle?

Because the abundance machine is accelerating. The data shows it. The only thing that hasn’t caught up for many people is their mental model.

Venture Performance: Early TVPI can lie; DPI tells a different story

Most LPs look at Year 5 numbers and think they’ve seen the future.

Top quartile? Great manager. Bottom quartile? Probably dead money.

But John Rikhtegar (Director, Capital at RBCx) recently shared StepStone data that complicates that narrative, especially when you compare TVPI and DPI side by side.

Before diving in, quick clarity on terms:

TVPI (Total Value to Paid-In) = Total fund value (realized + unrealized) divided by capital invested. It includes paper gains.

DPI (Distributions to Paid-In) = Cash actually returned to LPs divided by capital invested. It reflects realized liquidity.

TVPI tells you what a fund is worth on paper. DPI tells you what it has actually paid back.

And the difference matters more than most people realise.

StepStone’s dataset tracks how funds ranked at Year 5 end up ranking at Year 10. The reshuffling is significant.

On the TVPI side:

Only 49% of Year 5 top-quartile funds remain top quartile by Year 10

Bottom-quartile funds almost never recover — just 4% climb to top quartile

Translation: early paper marks don’t persist as reliably as allocators assume.

But DPI behaves differently.

63% of Year 5 top-quartile DPI funds stay top quartile by Year 10

And surprisingly, 22% of bottom-quartile DPI funds jump to top quartile

That second stat is important.

It shows that funds with slow early distributions can still produce late-cycle outliers. DPI captures the timing of liquidity, and venture outcomes often take longer to crystallise than interim marks suggest.

A few structural takeaways emerge.

First, DPI is stickier because it reflects real cashflows, secondaries, M&A exits, partial liquidity, not just valuation step-ups. In frothy markets, TVPI can look great on paper. DPI forces discipline.

Second, early DPI often signals a pacing strategy. Managers who trim positions or execute partial exits early may show stronger Year 5 DPI. That doesn’t necessarily mean they’ll generate the largest terminal outcomes — but it does mean they’re converting value into cash.

Third, the reshuffling between Year 5 and Year 10 reinforces something many LPs forget: venture is long-duration compounding. Outliers often take time. A bottom-quartile DPI at Year 5 doesn’t mean the fund is structurally broken — it may just mean the winners haven’t exited yet.

For GPs, this creates tension.

If early DPI strongly correlates with long-term rankings, managers may feel pressure to return capital early rather than recycle it into breakout companies. But recycling can sometimes enhance ultimate fund returns — even if it temporarily depresses DPI.

So what should founders, GPs, and LPs actually take from this?

Early TVPI is informative — but unstable

DPI is a stronger predictor — but still incomplete

Massive reshuffling happens between Years 5 and 10

Manager selection and portfolio construction matter more than mid-cycle quartile rankings

In short: early performance is a signal, not a verdict.

SOMETHING MORE

🧩 Frameworks & insightful posts

Wispr Flow’s framework to reach 100,000+ daily users - The CEO’s exact consumer playbook.

Most consumer startups don’t fail because the UI was ugly or the ads didn’t convert. They fail because they never became a habit.

Tanay Kothari, CEO of Wispr Flow (raised $81M), recently shared the internal playbook behind scaling to 100,000+ daily active users and over 10 billion words dictated. What’s powerful is not that it’s complicated. It’s that it’s simple, but brutally disciplined.

If you’re building a consumer, this is worth studying carefully.

(Wispr Flow is voice-first productivity software that helps people write, code, message, and work hands-free by speaking instead of typing )

I. Psychology: You can only change one behaviour at a time

This is the most expensive lesson in consumer.

Before Wispr Flow became software, the team built a hardware earpiece that could read neural signals from silent speech. It worked. Technically impressive. But it required two behaviour changes:

Wear a new device

Speak instead of typing

That’s where most products die.

Look at the pattern: Humane AI Pin asked users to wear a new device and interact with a projector. Google Glass asked users to wear a camera and talk in public.

Two behaviour shifts at once are too much cognitive friction.

When they pivoted to software, they asked for exactly one behaviour change: speak instead of type. Everything else stayed the same, same apps, same workflows, same screen.

That constraint became the growth engine.

90% of their growth is word of mouth. Not because of virality tricks but because they engineered around one psychological moment.

II. Product: Dependency beats demo

Most products impress in a demo. Very few become dependent. Two things moved the needle for Wispr.

First: they talked to 500+ people.

Not surveys. Not Typeform. Real conversations. Watching users struggle with existing dictation tools. Noting the exact moment frustration hit.

That’s where product clarity came from.

Patterns became obvious:

Names are constantly misspelt

Tone inconsistencies

Tools failing when users corrected themselves mid-sentence

Every core feature traces back to something someone said in those conversations.

Second: they built a product that learns about the user.

Not just AI dictation. Personalization:

Personal dictionary — if you fix a word once, it remembers

Tone controls — match capitalization, punctuation, style

Self-correction — “Let’s meet tomorrow, no wait, Friday” outputs correctly

These seem small. But they signal care.

And care compounds.

When users feel that a product improves with them, it stops feeling like software and starts feeling like infrastructure.

III. Team: How 200 people out-ship much larger companies

The product doesn’t matter if the team moves slowly.

Wispr’s team principles are unusually sharp.

Two-person pods Two engineers per project. Full ownership. No handoffs. No ambiguity.

Communication overhead scales exponentially with team size. Pods contain it.

Hire ex-founders Not for prestige. For instinct.

Ex-founders don’t file tickets. They fix problems. They can’t ignore broken things.

That ownership bias compounds velocity.

Hire for taste, not just skill

In consumer, taste is leverage.

The person who knows an animation is 50ms too slow.

The designer who rejects something technically correct but emotionally wrong.

The engineer who refactors invisible code because it feels wrong.

You can train skill. Taste is rare.

The underlying pattern

What’s striking is that none of this is a growth hack.

It’s alignment.

Psychology → one behaviour change

Product → remove friction repeatedly

Team → maximise ownership and taste

When these align, you don’t need constant marketing tricks. The product carries itself.

And the most important line Tanay shared:

Don’t build something people want. Build something people can’t live without.

Consumer products don’t win on features. They win on feelings. And the companies that understand that gap build habits instead of installs.

Are the old SaaS fundraising benchmarks officially dead in the AI era?

For years, founders had a clear playbook. Hit triple-triple-double-double growth. Cross a specific ARR milestone. Raise at the next valuation step.

That clarity doesn’t exist anymore.

Vivek Ramaswami, Partner at Madrona, recently shared “The New Rules for Fundraising in the AI Era”. The core idea is simple but important: in AI, growth is easier to manufacture, so investors care far more about durability than size.

Here’s what actually matters now.

Growth is louder, but less trustworthy

AI has collapsed the build time. Founders can ship fast, reach millions of users quickly, and even hit $5M–$10M ARR faster than ever.

But:

Usage can spike because it’s novel, not necessary.

Pilots look like traction but don’t convert.

Revenue can grow while retention quietly weakens.

Competition appears overnight.

In SaaS, recurring revenue was a clean signal. In AI, consumption can mean curiosity just as easily as dependency.

So investors aren’t asking “Did you hit $X ARR?” anymore.

They’re asking: Is this growth compounding — or about to stall?

What actually closes rounds now

The companies raising strong rounds today tend to show four things clearly.

Clean proof of real demand

It’s not about how big you are. It’s about how clear your data is.

Investors look for:

Strong retention cohorts

Organic expansion inside accounts

Revenue that isn’t disguised consulting or short-term pilots

Clear definitions of ARR and usage

A $1M ARR company with obvious product-market fit can look stronger than a $10M ARR company with fuzzy numbers.

Ambiguity kills conviction.

Momentum over magnitude

A smaller company growing 30% month-over-month is often more fundable than a larger one growing slowly.

Investors read trajectory:

Is growth accelerating?

Are customers using more over time?

Is expansion happening without heavy sales pressure?

Flat quarters now require a very strong explanation. “We’re launching a big feature” is no longer enough.

Economics that make sense for AI

AI margins don’t look like old SaaS. Gross margins of 50–60% (sometimes lower) are normal when inference and GPU costs are real.

The key question is not “Are your margins high enough?”

It’s:

Do you deeply understand your unit economics?

Can you explain how they improve at scale?

Does usage growth correlate with real value creation?

Investors want fluency, not perfection.

A clear wedge

Most AI pitches fail here.

Either founders show metrics with no long-term arc, or they pitch a massive vision with no evidence that they can reach it.

Strong companies:

Solve one urgent, painful problem today

Use that wedge to expand naturally into adjacent workflows

Show traction that already supports that expansion

If the wedge, roadmap, and metrics align, the story feels inevitable.

The new filter: durability

Because AI products can grow fast and collapse fast, investors now focus heavily on durability.

During diligence, they ask customers a simple question:

“What happens if this product disappears tomorrow?”

If the answer is:

“We’d switch.” → weak position.

“We’d be in trouble.” → strong position.

Durability signals include:

Deep workflow integration

Data locked into your system

Organic expansion

Increasing dependence over time

This is where many AI startups fall short.

The real shift

The fundraising bar isn’t lower. It’s just different.

Investors no longer rely on pattern-matching ARR benchmarks. They’re making judgment calls about whether your growth is structural or temporary.

So the better question for founders isn’t: “Are we big enough to raise?”

It’s: “If someone studies our numbers and speaks to our top customers, will they believe this company compounds for years?”

That’s the standard now.

The 3 curves that quietly decide if your startup scales or collapses.

Most founders obsess over one curve: growth.

But as Swizec shared in his thread, scalable businesses are really about managing three curves at the same time. If you get their shape wrong, growth will crush you instead of compounding for you.

Here’s the framework and what it means in practice.

The exponential curve: users & revenue

This is the dream curve. Users and revenue should compound. Not just grow steadily but bend upward over time.

That only happens when:

Retention improves, not just acquisition

Usage per customer increases

Word-of-mouth starts doing real work

The product becomes embedded in workflows

Features bring users in. Reliability and habit keep them there.

A lot of startups hit early spikes especially in the AI era but the curve flattens because the product is interesting, not indispensable. If your best customers would feel real pain if you disappeared tomorrow, your exponential curve has a chance to hold.

If they’d “figure something else out,” you’re still fragile. The growth curve is not a marketing story. It’s a retention story.

The linear curve: bugs & complexity

Here’s the part nobody glamorizes. As users grow, bugs grow. Edge cases grow. Exceptions multiply. Things that used to happen once a month become daily fires.

This curve should scale linearly with usage, not faster.

If bugs grow faster than users, your system architecture is already cracking.

What keeps this curve healthy?

Clean abstractions

Automated testing

Strict code reviews

Static typing & linters

CI/CD pipelines

Clear state management

All the “boring” engineering discipline that feels slow early on is what saves you at scale.

At 1,000 users, duct tape works. At 100,000 users, duct tape becomes chaos.

Reality at scale is a pile of edge cases. If your system can’t absorb them predictably, growth turns into technical debt with interest.

The logarithmic curve: support & operational burden

This is the real scalability test. If your users grow 10x and your support team also needs to grow 10x, you don’t have leverage, you have headcount expansion.

Support and operational load should grow logarithmically relative to users.

That happens when you:

Build self-serve onboarding

Create strong documentation

Automate repetitive workflows

Reduce manual approvals

Eliminate unnecessary clicks

Fix root causes instead of replying to tickets

This applies internally too. Engineering effort per release should decrease over time, not increase. If every feature requires more meetings, more coordination, more Slack threads, your internal support burden is scaling linearly.

That’s a warning sign.

The geometry of a scalable company

A truly scalable business looks like this:

Users & revenue → exponential

Bugs & complexity → linear

Support & ops burden → logarithmic

When those curves align, you build an asset. When they don’t, growth exposes weakness.

Many startups don’t die because demand was weak. They die because their systems couldn’t handle success.

Building features is exciting. Designing systems that survive exponential growth is harder and far more valuable.

The real question isn’t “Are we growing?” It’s “Are our curves shaped correctly?”

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Primary Ventures, a New York-based early-stage VC firm, has raised $625M for Fund V to double down on seed and pre-seed investing across the U.S. (Link)

2048 Ventures, a NYC and Boston, MA-based thesis-driven earliest-stage venture capital firm, closed its third fund at $82M. (Link)

Kembara, a Madrid-based deep tech and climate-focused fund under Mundi Ventures, has raised €750M in its first close led by the European Investment Fund. (Link)

New Startup Deals

Smart Bricks, a San Francisco, CA-based AI startup building agentic AI infrastructure for real-estate investing, raised $5M in Pre-Seed funding. (Link)

Birch Hill Holdings, a NYC-based developer of institutional digital asset infrastructure for on-chain lending and tokenised markets, raised $2.5m in Pre-Seed funding. (Link)

ThrowMeNot, a Dubai, UAE-based sustainability-focused online food marketplace, raised $550K in Pre-Seed funding. (Link)

Alcove, a NYC-based developer of private Pods for neighbourhoods or hotels, raised $1m in pre-seed funding. (Link)

Feltsense, a San Francisco, CA-based AI agent services company, raised $5.1M in Seed funding. (Link)

SENAI, a Washington, DC-based provider of an online video intelligence platform, raised $6.2M in Seed funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Analyst - Plug and Play Tech Centre | Italy - Apply Here

Associatie - Root Venture | USA - Apply Here

Director - NICE | USA - Apply Here

Fund Controller - NFX | USA - Apply Here

Partner 16 - a16z | USA - Apply Here

Investor Relations - SC Founders Fund | India - Apply Here

Ventures Associate - Plug and Play Tech Centre | USA - Apply Here

VC Analyst - Alstin Capital | Germany - Apply Here

Analyst - Infrastructure & Real Assets - Stepstone Group | Australia - Apply Here

Social Media Freelancer - Initialised Capital | USA - Apply Here

Analyst / Associate - Saints Capital | USA - Apply Here

Investment Analyst Intern - NAV Capital | Dubai - Apply Here

PE & VC Partner Manager - Dealhub | UK - Apply Here

VC Platform & Events Manager - 1001 VC | USA - Apply Here

MBA Venture Capital Intern - Cerity Partners | USA - Apply Here

PARTNERSHIP WITH US

Get your product in front of over 102,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator