The Founder's Guide to Secondaries: Getting Liquid Before the Exit.

$61B left startups last year, more than every IPO combined. What a secondary is, how to run one, the tax break most miss, and the strategy founders get wrong.

👋 Hey, Sahil here - welcome to this edition of Venture Curator, where we break down how great startups grow, how top investors think, and what’s shaping the future of tech.

P.S. Get access to 100+ startup & VC resources, investor databases, fundraising templates, 150+ premium archive posts and exclusive startup research - all in one place.

FROM OUR PARTNER - CYTONICS

500M+ Have Been Waiting for This Biotech Breakthrough

Musculoskeletal conditions are the leading contributor to disability worldwide.* One of the foremost causes is osteoarthritis, which affects 500M+ people.*

Cytonics aims to change that with the first and only potential cure for this $560B disease.

Their drug, CYT-108, targets the root cause of joint degradation. And it just cleared Phase 1 clinical trials.

Historically, like when GSK acquired Bellus for $2B, Big Pharma’s made its move on biotech targets near the next phase, when efficacy data is established but no valuation is set.

While nothing’s guaranteed, Cytonics is preparing for that imminent phase.

Invest in Cytonics before it begins.

Source: World Health Organization*

Source: The Lancet Rheumatology*

This is a paid advertisement for Cytonics Regulation CF offering. Please read the offering circular at https://cytonics.com/

Forward-looking statements are subject to risks and uncertainties. There is no guarantee of performance. Past performance does not predict future results. All investments involve risk, including loss of principal

📜 DEEP DIVE

The Founder’s guide to secondaries: getting liquid before the exit.

A founder I’ll keep anonymous crossed $40 million in net worth two years ago, on paper. Her company had just closed a Series C, the 409A (the formal appraisal that decides what her shares are officially worth) had caught up to the new round, and on a spreadsheet she was rich. That same month she was running the numbers on whether to renew her apartment lease or move somewhere cheaper, because her actual bank balance was a founder’s salary minus rent in a major city.

That gap - wealthy on the cap table, tight in the checking account - used to be the toll you paid to build something big. You accepted it going in. Build for a decade, wait for the IPO or the acquisition, and somewhere on the far side the paper turns into money.

The waiting was the deal.

The deal has changed. Quietly, and a lot faster than most of the people writing about startups have noticed.

Why does $40 million on paper still leave a founder broke?

Because the old clock broke: companies are staying private far longer than the model assumed. Of the roughly 1,920 unicorns in the world as of March 2026, 59% were founded more than ten years ago, and 20% more than fifteen years ago, according to World Economic Forum / Jay Ritter data.

The five-to-seven-year round trip from seed to liquidity that defined venture for thirty years is gone. Top companies now meet their capital needs privately and stay there, sometimes skipping the public markets entirely.

Which leaves a strange new problem at the centre of a “successful” startup:

enormous created value, locked inside shares nobody can spend. Founders feel it. Early employees feel it worse - they took below-market salaries for equity that, for years, has been a number on a screen they can’t touch.

And the longer the private window stretches, the longer that money stays frozen.

For a while, there was no release valve. Now there is one, and it’s swallowing the market whole.

What actually replaced the exit?

Here’s the number that should reframe how you think about your own equity.

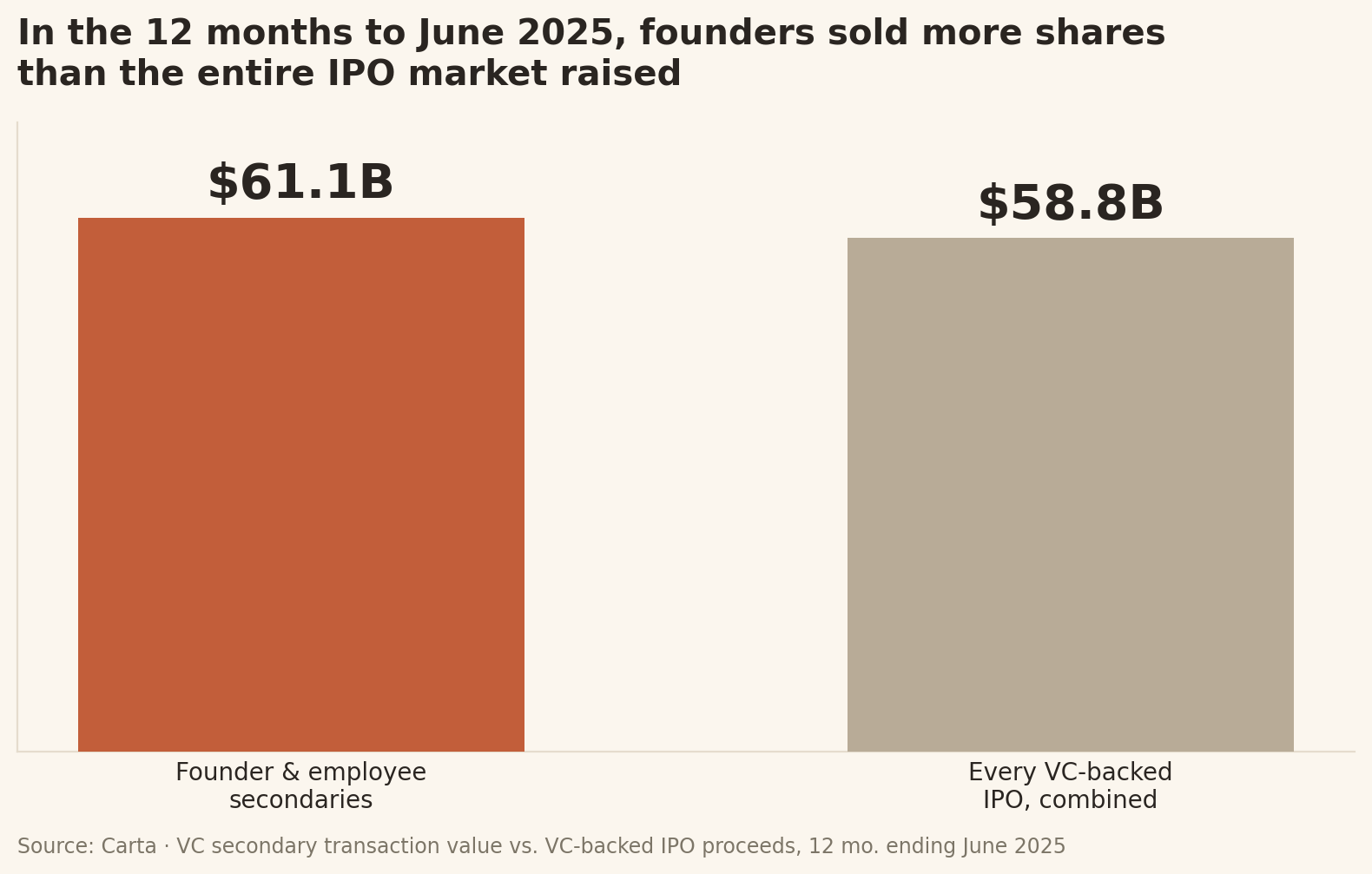

In the twelve months ending June 2025, founders, employees and early investors sold $61.1 billion of existing shares on the secondary market (selling your already-owned shares to another investor, instead of the company issuing new ones to raise money) - more than the $58.8 billion raised by every single VC-backed IPO over the same period, according to Carta.

Selling your shares privately, without an exit, is now a bigger source of liquidity than the entire IPO market.

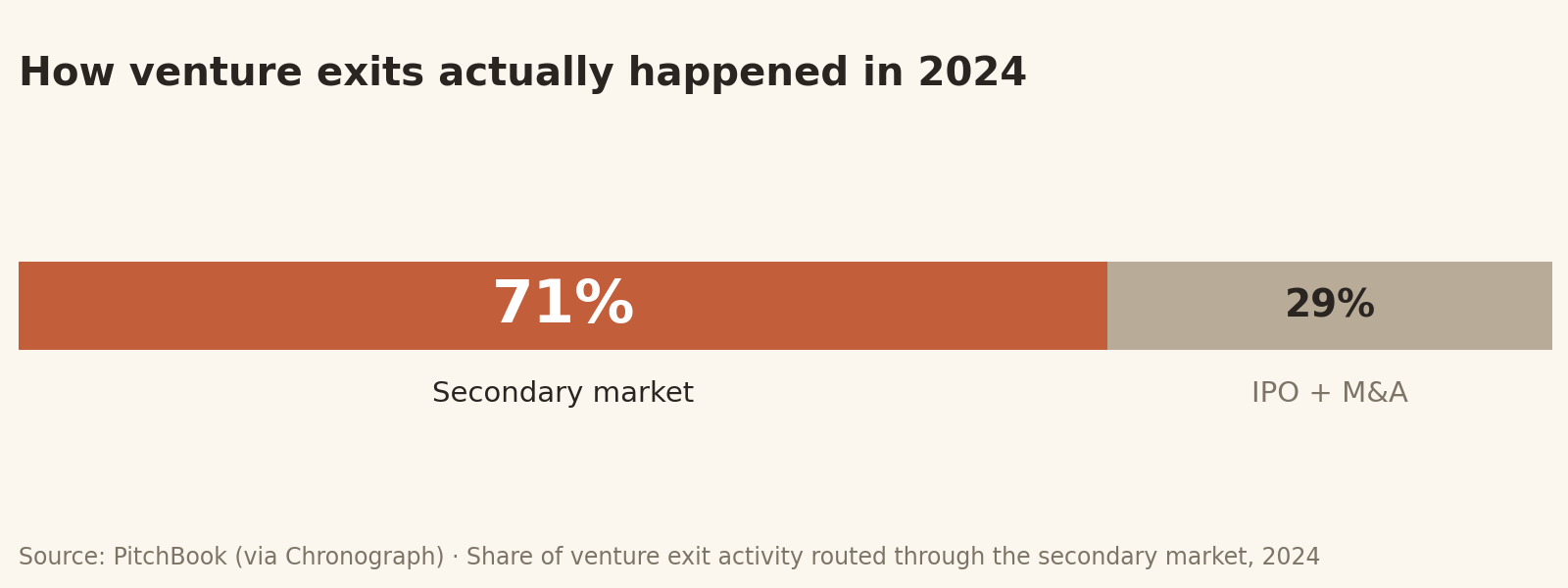

It’s not a one-quarter blip, either. Step back to the full picture of how money actually left venture-backed companies in 2024, and the old playbook looks almost quaint: an estimated 71% of all venture exits ran through the secondary market rather than IPOs or acquisitions (PitchBook, via Chronograph).

The trajectory is the loud part. Annualised direct secondary value climbed from roughly $50 billion at the end of 2024 to about $91.7 billion a year later - an 83% jump in five quarters, per The State of Venture.

Across the whole market (venture plus fund-level), total secondary volume ballooned to about $160 billion in 2024 and is projected to have cleared $210 billion in 2025. And it hasn’t cooled in 2026 - the US venture secondary market hit fresh record levels in the first quarter of 2026, per PitchBook. There is now a deep, well-capitalised bid waiting for private startup stock.

The clearest sign this has gone from rare event to routine plumbing: the average gap between tender offers at a given company collapsed from 899 days in 2022 to just 132 days by 2025 (PitchBook, via Crowdfund Insider). Companies used to open a liquidity window once every two and a half years. Now it’s roughly every four months.

So the finish line moved. The thing you assumed you’d wait ten years for - turning equity into spendable money - is now something that happens during the build, on a repeatable schedule, for a growing list of companies.

But the headline number hides three things that decide whether you get any of it.

The first is that $61 billion is not spread evenly. A startling share of it flows to a tiny handful of names, and whether you make that list depends on factors most founders have never been told to optimise for.

The second is that the mechanics have traps - a wrong move can blow up your 409A, spook your board, or kill the deal before it clears.

And the third is timing: there’s a specific window in a company’s life when this is possible, and a specific way to open it without looking like you’re heading for the door.

That’s what the rest of this issue is for.

What you’ll find below the line

How does a founder actually get a secondary done - the two real paths, and how much of your stake you can realistically sell?

What’s the catch the headline number hides, and why 86% of the money is locked to just twenty companies?

What are the three traps - ROFR, 409A, and the signalling problem, that quietly kill founder secondaries before they close?

What do you actually keep after tax, and why did a 2025 law quietly hand founders a much bigger break on exactly this kind of sale?

When is the window actually open, and how do you time a sale around a round so it reads as confidence, not exit?

If you’re building right now, what do you do this quarter to put yourself on the right side of all of this?