The Hidden VC Scorecard That Decides Your Next Round.

Every fund sorts its portfolio into three buckets and five observable signals reveal which one you're in, months before you raise.

👋 Hey, Sahil here - welcome to today’s edition of Venture Curator, where we break down how great startups grow, how top investors think, and what’s shaping the future of tech.

P.S. Get access to 100+ startup & VC resources, investor databases, fundraising templates, 150+ premium archive posts and exclusive startup research - all in one place.

🤝 FROM OUR PARTNER - FRAMER

Launch your site faster than ever with Framer - now with Agents that make every part of your workflow effortless…

Framer is the pro website builder for creators, teams, and businesses that care enough to get every detail right.

Now with Agents that work alongside you across the full website workflow: designing new pages, managing your CMS, editing content, and adding SEO all without leaving the tool where the real site lives. Trusted by teams at companies like Miro and Perplexity

Agents bring speed and scale; you bring taste, judgment, and control. Together you can:

Build and iterate faster: generate sections, refine layout and styling, and ship updates in minutes.

Scale content with confidence: update CMS collections, localise copy, and keep metadata consistent across pages.

Stay production‑ready: reviewable changes, collaboration, and safeguards that help teams ship without handoffs.

Launch your site with Framer today →

📜 DEEP DIVE

The Hidden VC Scorecard That Decides Your Next Round.

There’s a meeting your investors hold that you will never be invited to.

It usually happens quarterly. The partners sit down, pull up the portfolio, and go through the companies one by one. Not to review your board deck.

To answer one question: if this company raises again, do we put in more money?

Every name gets a mark. At some funds it’s a formal score. At others it’s shorthand in a reserves model. But the output is the same everywhere: your company gets sorted into one of three buckets.

Back the truck up. The fund will defend its ownership at any reasonable price, take super pro-rata if it can get it, and pre-empt your round if you let them.

Hold. The fund will do its pro-rata if a credible new lead shows up and sets the price. It won’t lead. It won’t stretch.

Quiet zombie. The fund has mentally written you down. It will keep taking your board calls, keep saying encouraging things, and will not wire another dollar. You just haven’t been told.

Here’s what makes this uncomfortable: the sorting isn’t a reaction to your next fundraise. It happens before your next fundraise, continuously, whether you’re raising or not. By the time you send that “excited to share we’re opening our Series A” email, the most important investors on your cap table decided their answer months ago.

Most founders don’t know this system exists. They think of their investors as people who made a decision once, at the seed, and will make a fresh decision later, at the A. That’s not how a fund works. A fund is a portfolio machine that re-underwrites you every quarter, and the machine’s output determines more about your next round than your pitch will.

This issue is about that machine - how it works, the five observable signals that tell you which bucket you’re in, and the six-month playbook to change buckets before you raise.

Half the fund was never for you (well - not automatically)

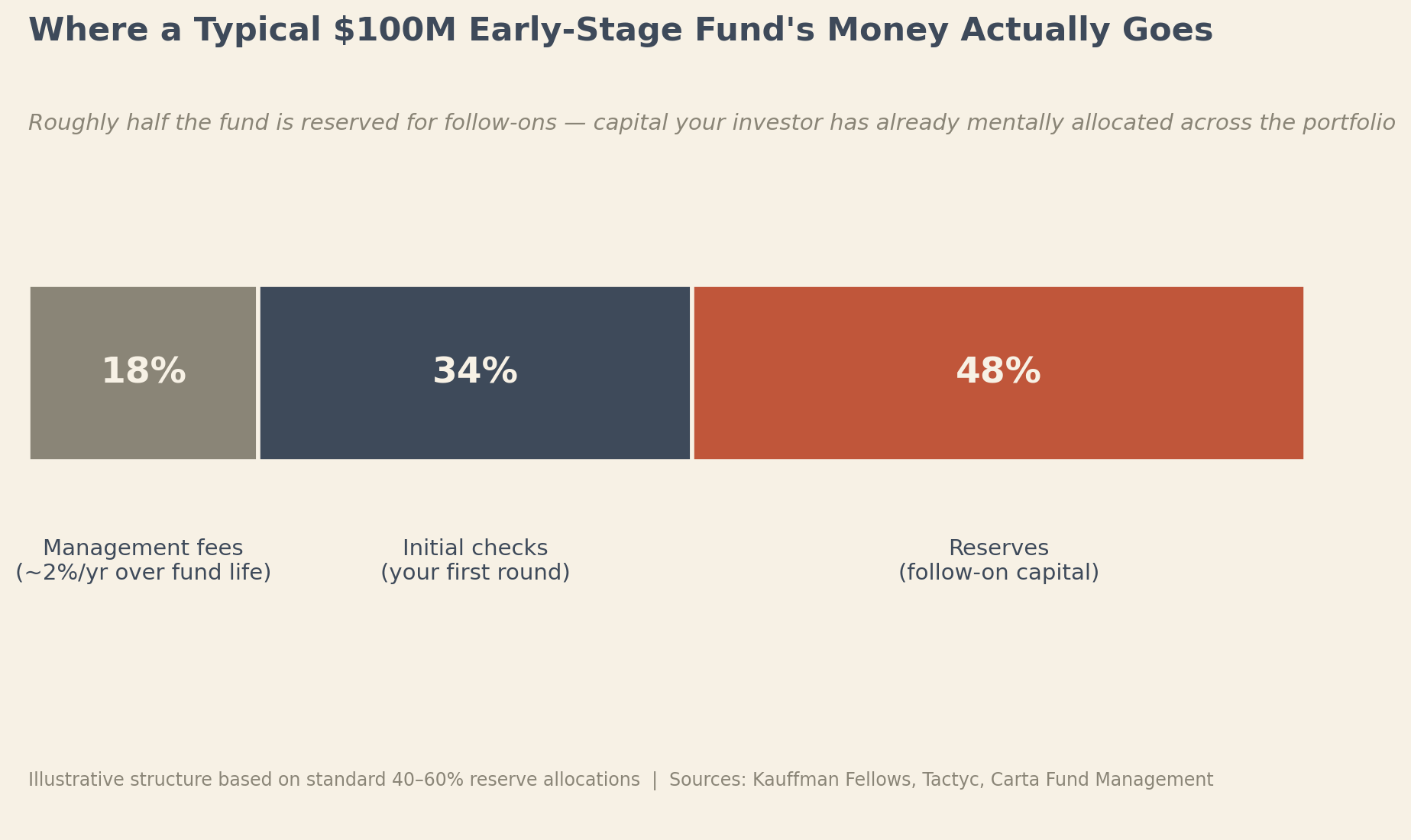

Start with a number most founders have never thought about: the reserve ratio.

When a VC raises a $100M fund, they don’t have $100M to hand out to new startups. Management fees eat roughly 15-20% over the fund’s life.

Of what remains, funds typically hold 40-60% back as reserves - capital earmarked for follow-on investments into companies already in the portfolio. Fund construction guides from Kauffman Fellows and Tactyc both put the standard follow-on allocation at 40-60% of the fund, and analyses of fund performance consistently find that top-quartile managers reserve 40-50%.

Sit with that for a second. The check your investor wrote you at seed came from the smaller half of their fund. The bigger pool of money - the reserves - is sitting there right now, and the entire job of a venture partnership between fundraises is deciding which portfolio companies get it.

That decision is not sentimental, and it’s not evenly spread.

Reserves exist for one reason: to concentrate more capital into the handful of companies that will return the fund.

Sophisticated funds literally calculate a “follow-on MOIC” - the expected return on the next dollar into your company, modelled separately from the first dollar. If that number doesn’t clear the bar, the model says pass, no matter how much the partner likes you.

So when your investor says “we’re saving reserves for our best companies,” understand the precise meaning: there is a live, internal ranking, you are on it, and your position on it is the single most important fact about your next fundraise that you don’t know.

The market just made the buckets brutal

This sorting always existed. What’s changed is how much it now decides.

Three numbers from the current market, and they stack into one picture.

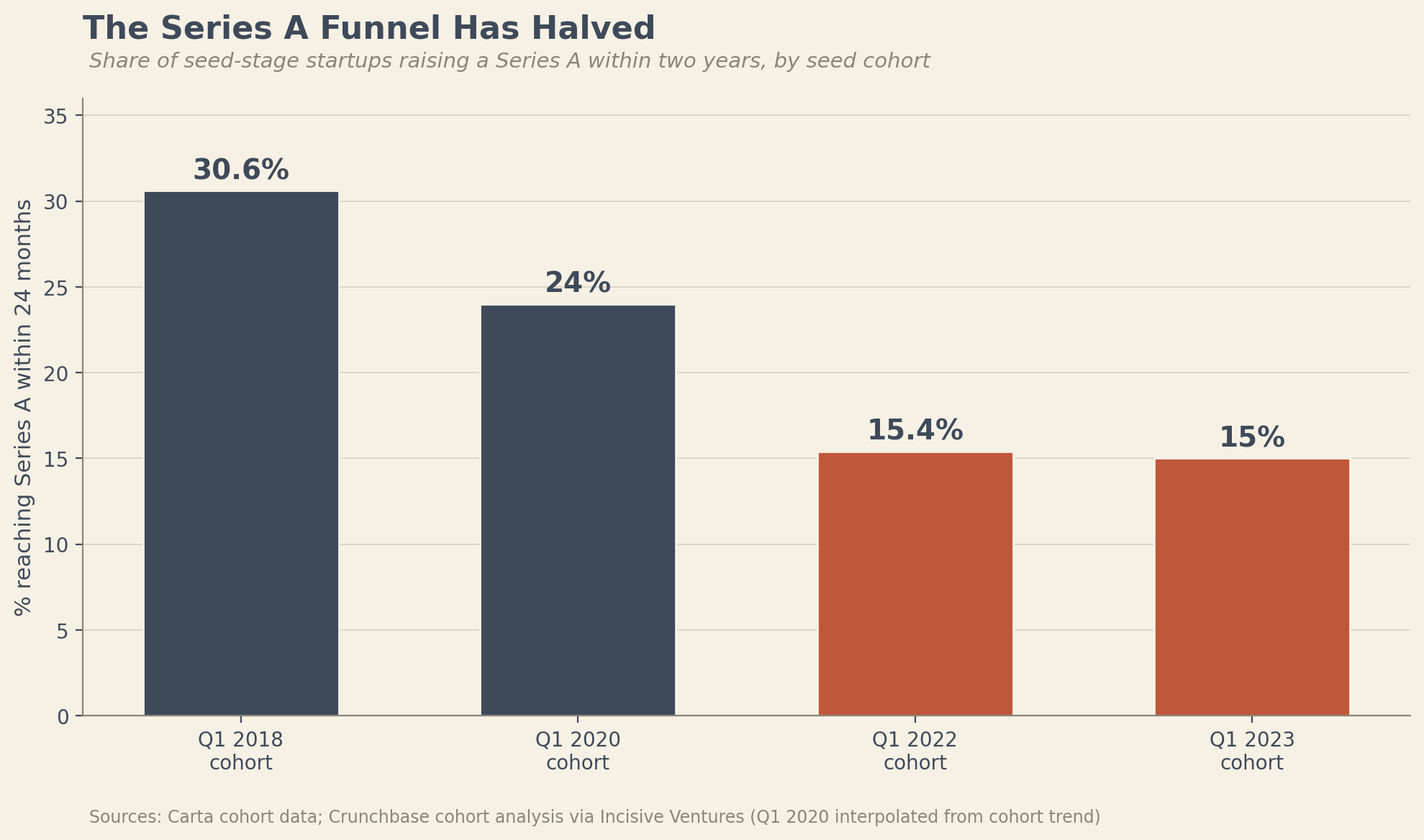

First: graduation rates have halved.

Carta’s cohort data shows that 30.6% of companies that raised a seed round in Q1 2018 reached a Series A within two years. For the Q1 2022 cohort, that figure was 15.4%. Early reads on the 2023 cohort land around 15% as well. The median time from seed to A has stretched past two years, up from roughly 1.7 years in 2019.

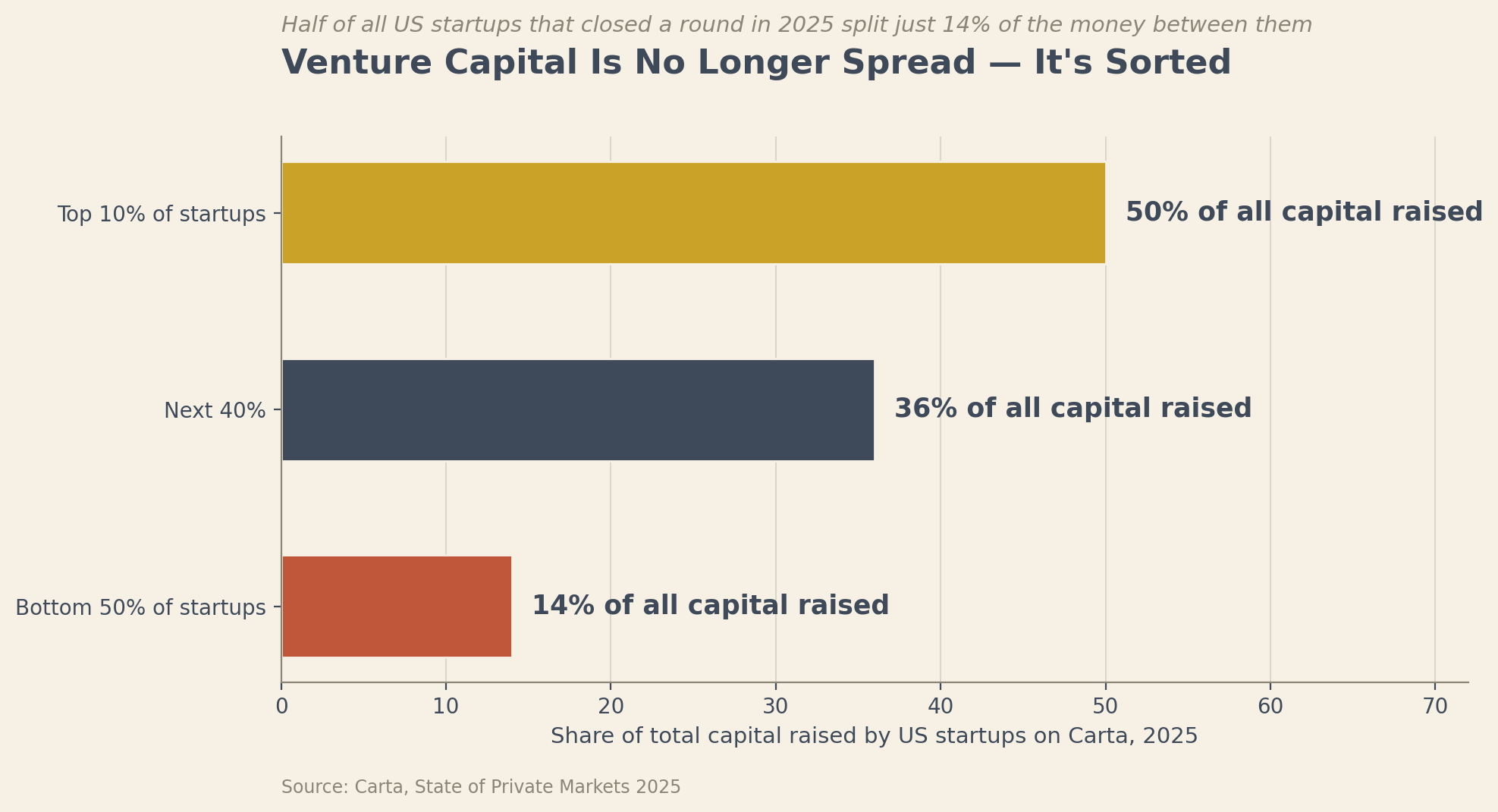

Second: capital has sorted, not spread.

In 2025, per Carta, the bottom 50% of US startups that successfully closed a round split just 14% of all capital raised between them. The top 10% took roughly half. That’s among companies that raised - the sorted-out companies aren’t even in the denominator.

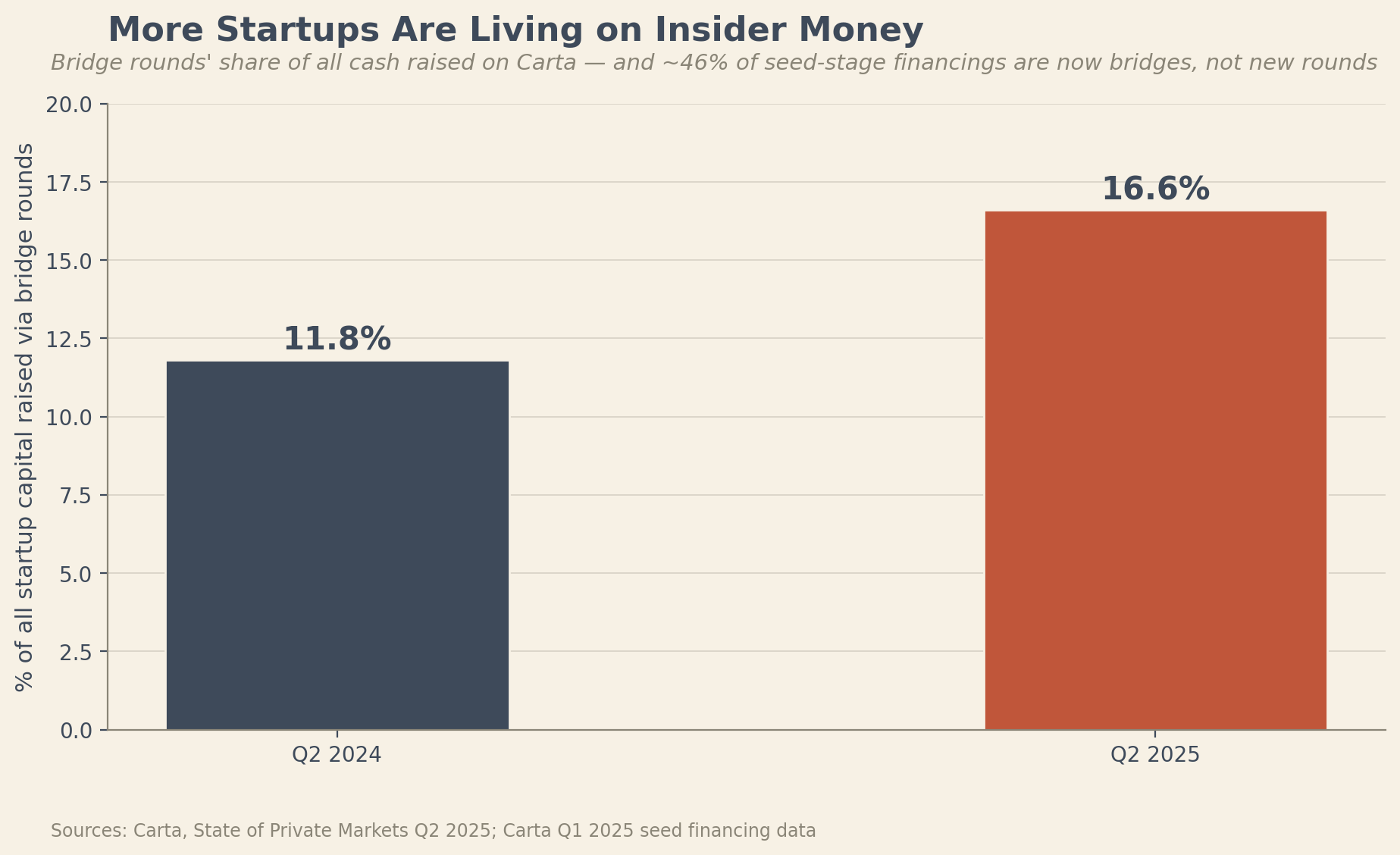

Third: more companies are living on insider money.

Bridge rounds accounted for 16.6% of all cash raised on Carta in Q2 2025, up from 11.8% a year earlier. At the seed stage it’s starker - roughly 46% of seed-stage financings in early 2025 were bridge or extension rounds rather than new-priced rounds.

Put the three together, and the picture is this:

The gap between rounds has stretched to 2+ years, most companies won’t clear it, and the thing keeping companies alive across the gap is insider capital - which is to say, reserves - which is to say, the bucket you’re in.

In 2021, the buckets barely mattered. Growth-stage tourists would fund your A whether your seed investors showed up or not. In 2026, the bucket decision is the fundraise. If your insiders are in, you get a bridge that buys you 12 months and a warm co-sign that de-risks your round for new leads. If they’re out, you’re raising into the hardest Series A market in a decade with a silent cap table behind you, and every new investor you pitch will notice the silence.

Which raises the obvious question. Your investors know your bucket. New investors will infer it. The only person operating blind is you.

The rest of this issue fixes that. Below the line:

How the reserve decision actually gets made (including the factor that has nothing to do with your metrics)

The five observable signals that reveal your bucket with surprising precision

A decoder for what investor language actually means, and

The six-month playbook for changing buckets before you raise.