This 20,000+ organization report exposes the biggest gap in AI today. | Google’s 20-year secret is now available.

Is AI quietly eliminating customer support jobs? & Real edge in VC picking the best startup or picking the right category early?

👋 Hey, Sahil here - Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

Is raising at a high valuation actually putting your startup at risk?

Is AI quietly eliminating customer support jobs?

Frameworks & insightful posts :

What surprising results from 20,000+ organisations reveal about AI’s real shift.

Google’s 20-year secret is now available to every enterprise.

Is the real edge in VC picking the best startup or picking the right category early?

FROM OUR PARTNER - FRAMER

🚀 Launch fast. Design beautifully. Build your company’s website on Framer

Framer helps teams design, build, and launch their marketing sites lightning fast. With the ability to publish hundreds of CMS pages in a single click, operate at a global scale with seamless localisation, and even host unified content across multiple domains, teams have never been able to ship faster. Trusted by companies like Miro, Bilt, and Perplexity

Speed without chaos: ship pages and updates faster without turning the site into a fragile set of one-off hacks

Reduce dependency: shift routine brand and marketing work out of product engineering queues.

Production-grade foundation: Run real marketing systems (CMS, SEO, performance optimisation) with governance and collaboration

Build your company’s site on Framer today →

🤝 PARTNERSHIP WITH US

Get your product in front of over 115,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

Is raising at a high valuation actually putting your startup at risk?

There’s a growing feeling in venture right now that things have gone a bit… irrational.

That feeling isn’t random.

It comes from data shared by Carta’s Head of Insights, Peter Walker, who analysed nearly 14,000 seed rounds across U.S. companies. His latest breakdown shows that the top 5% of seed valuations have reached ~$115M - a number that would have seemed unrealistic not too long ago.

At the same time, investors like Bryce Roberts have openly said they “can’t relate” to where the VC world is heading.

And when you look at the data, you understand why.

Because what looks like a single market from the outside is actually splitting into two very different realities.

On one end, you have a small group of companies - mostly AI-driven, where everything is moving faster than ever:

Top-tier founders are raising at record speed, sometimes in days

Large funds are entering at seed, competing aggressively

Valuations are being set based on future dominance, not current traction

$100M+ seed rounds are becoming more common in this segment

This is the part of the market everyone sees, shares, and talks about.

But it’s not the full picture.

Because for the remaining 95% of companies, the environment looks very different.

The median seed valuation is still around ~$24M, which tells you that most startups are still raising in a relatively grounded range. Investors are still asking the same core questions around traction, market, and execution.

In other words, discipline hasn’t disappeared—it’s just not evenly distributed.

This creates a misleading narrative.

When people talk about “seed valuations going crazy,” they’re often looking at blended numbers that combine:

A small set of extreme outliers is pulling valuations up

A much larger base of companies is operating normally

And that gap between ~$24M (median) and ~$115M (top 5%) is where the confusion comes from.

The deeper insight here is about the AI cycle itself.

AI can absolutely be a transformational shift and at the same time, behave like a classic hype cycle where capital floods in faster than outcomes materialize.

Both can exist together. That’s what this data is showing.

For founders, the biggest mistake right now is anchoring to the wrong benchmark.

It’s easy to see these headline valuations and feel like you need to match them. But those companies are exceptions, not the standard.

What actually matters is much simpler:

Are you building something that can justify your valuation over time?

Are you optimising for long-term outcomes or short-term optics?

Can you grow into the expectations you’re setting today?

Because high valuations don’t remove risk. They just delay when it shows up. And in this kind of market, the real advantage isn’t raising at the highest price.

It’s knowing which market you’re actually playing in.

Is AI quietly eliminating customer support jobs?

For years, AI replacing jobs felt theoretical. Now we’re starting to see clean data.

Jason Lemkin recently shared hiring numbers from Pave covering 386,500 new hires, and the shift in Customer Support is dramatic. In Q4 2023, support roles accounted for 8.30% of new hires. By Q3 2025, that number fell to 2.88%.

That’s a roughly 65% decline in two years. And almost half of that drop happened in just the last three quarters.

This isn’t gradual automation. It’s an accelerating adoption curve.

Lemkin also shared a concrete operating example:

one company went from 20+ support employees to just 3 humans supported by AI agents, while revenue swung from -19% to +47% YoY during the transition. AI now handles the majority of inbound volume.

But the real story isn’t that support is disappearing. It’s being redesigned.

What’s actually happening inside companies:

AI is now Tier 1 support.

Basic ticket routing, FAQs, account updates, policy explanations, these are increasingly handled by AI at 40–60%+ deflection rates without degrading quality.

Entry-level ticket roles are shrinking.

The classic $50K generalist support rep high-volume, repetitive tasks, is fading.

Higher-skilled human roles are expanding.

What remains requires judgment: technical escalations, implementation, complex integrations, revenue-sensitive accounts. These roles often pay $100K+ and look more like hybrid Customer Success positions.

Support is merging upward into CS.

When AI handles half the tickets, the remaining human work becomes proactive:

onboarding

expansion conversations

churn prevention

relationship building

That’s not elimination. That’s elevation. The more interesting implication is strategic.

Support is simply the easiest category to automate first:

high volume

structured queries

well-documented answers

low tolerance for long response times

It’s the cleanest training ground for AI agents. And that makes it a leading indicator.

The same pattern is likely to come for:

SDR roles handling repetitive outbound

Parts of marketing ops and content workflows

QA and testing functions

Mid-level product ops work

Any function where AI can reliably handle 40-60% of structured volume without degrading output quality becomes vulnerable to redesign.

For founders, the takeaway isn’t “cut headcount.” It’s this:

If AI can handle the repetitive layer of your function, redesign the human layer above it.

Companies that simply reduce costs miss the upside. The real leverage shows up when:

Response times collapse

Coverage becomes 24/7

Humans shift to revenue-impacting work

Cost per ticket drops while CSAT improves

The 65% drop in support hiring doesn’t mean companies care less about customers. It means the best ones have figured out a new operating model.

The window to adapt is shrinking. Support was first because it was easiest. It won’t be the last.

SOMETHING MORE

🧩 Frameworks & insightful posts

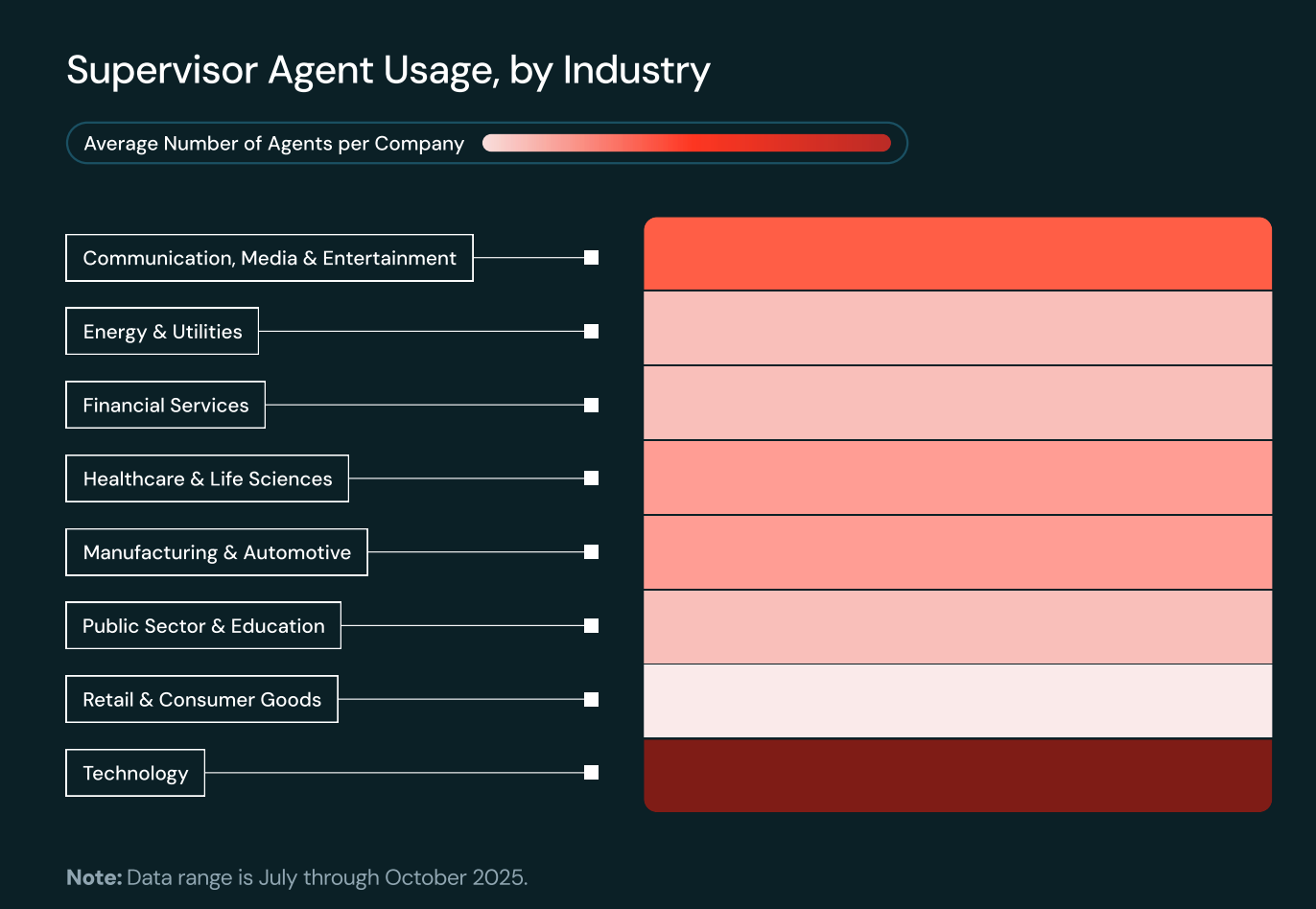

What surprising results from 20,000+ organisations reveal about AI’s real shift.

Most people still think AI is in its “assistant phase” - helping write, summarise, or speed things up.

But inside enterprises, something much bigger is already happening.

A report covering 20,000+ organisations (including over 60% of the Fortune 500) shows a clear shift: companies are moving from using AI as a tool → to building systems where AI actually executes work end-to-end.

This shift isn’t gradual - it’s accelerating fast.

Multi-agent systems usage grew 327% in just 4 months

80% of databases are now created by AI agents

97% of database testing environments are handled by agents

This is the key change: AI is no longer sitting on top of workflows - it’s starting to run the infrastructure those workflows depend on.

What’s interesting is how practical the adoption looks.

Despite all the hype, enterprises aren’t starting with bold reinvention. They’re starting with replacing repetitive, necessary work at scale.

Around 40% of use cases today are focused on customer-facing operations like support, onboarding, and personalisation, while others focus on tasks like classification, routing, and summarisation.

In other words, the first wave of AI is not disruption - it’s operational efficiency.

But underneath this, a deeper shift is happening in how systems are built.

Traditional enterprise infrastructure was designed for humans - predictable workloads, manual provisioning, and structured inputs.

Agentic systems break all of these assumptions. They continuously create and destroy environments, generate high-frequency real-time queries, and run multi-step reasoning loops across systems.

That’s why a new infrastructure layer is emerging - systems built not for humans, but for autonomous agents operating continuously.

At the same time, the way software gets built is changing.

The rise of “vibe coding” (describe → generate) is turning software creation into a natural language problem. More than 50,000 AI apps have already been created in a short period, growing at ~250% in just six months. Even non-technical users can now build working prototypes.

This massively increases the speed of building - but also introduces a new problem.

Most AI never makes it to production.

~95% of GenAI pilots fail to ship

Only ~2% of companies report meaningful business results

So the real bottleneck isn’t building AI. It’s operationalising it. And the data shows very clearly what separates teams that succeed:

Companies using evaluation systems → 6x more AI projects reach production

Companies investing in governance → 12x more projects reach production

Evaluation ensures quality and reliability. Governance ensures control, safety, and compliance.

Without these, AI stays stuck in demos.

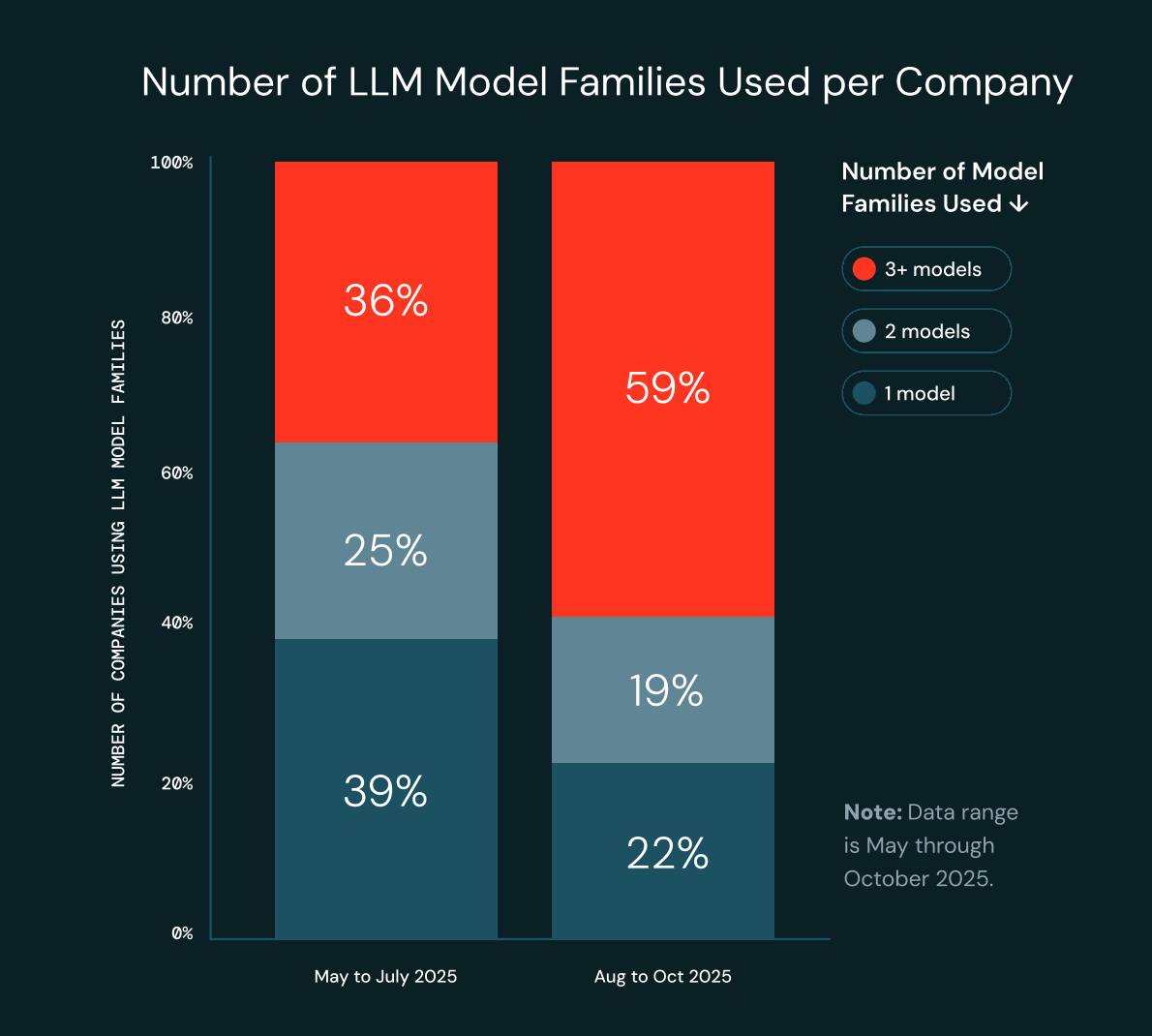

Another subtle but important shift is happening at the model layer.

Enterprises are no longer betting on a single provider - they’re going multi-model by default.

Around 78% of companies now use two or more LLM families, and the share using three or more is rising quickly. This is less about experimentation and more about optimising performance, cost, and flexibility.

Finally, one of the clearest signals of where things are headed: AI is becoming real-time infrastructure.

Nearly all requests (~96%) are processed in real time, not batch. This matters because AI is no longer just analysing data after the fact - it’s becoming part of live systems that directly impact decisions and outcomes.

So -

We’ve moved past “AI as a feature.” We’re entering a phase where AI becomes part of how companies actually operate.

But the winners won’t be the ones using the most AI. They’ll be the ones who figure out how to turn it into reliable, production-grade systems with the right guardrails.

Because in this phase, the edge isn’t access to AI - it’s execution.

Google’s 20-year secret is now available to every enterprise.

For the last 20 years, the biggest consumer companies have built a simple but powerful advantage:

Every user action made the product smarter.

Google, Amazon, Netflix, TikTok - they didn’t just track outcomes. They captured behaviour. What you clicked, ignored, hovered on, and abandoned. That data compounded over time into better recommendations, better products, and ultimately, massive defensibility.

Ashu Garg (Foundation Capital) points out something interesting: Enterprise software never had this loop.

Not because enterprise decisions don’t matter - but because they were almost impossible to capture.

In B2C, decisions happen inside a clean interface. One user, one action, fully observable.

In B2B, decisions are messy.

They happen across sales, finance, legal, ops, and management - each with different incentives. A pricing decision isn’t a click. It’s a negotiation. A contract isn’t a forml it’s a series of trade-offs.

And most importantly, enterprise systems only captured the outcome, not the reasoning behind it.

A discount field tells you the number, not why it was given

A contract shows the final clause, not what was negotiated

A support ticket shows resolution, not the decision path

So while consumer companies built compounding data moats, enterprise software mostly didn’t. That’s starting to change now.

The shift is from behavioural data → decision data.

And this is where things get interesting.

Enterprise work today increasingly happens on “instrumentable surfaces”- Slack threads, docs, tickets, calls, approvals. What used to live in someone’s head is now partially visible across systems.

But visibility alone wasn’t enough. The data was unstructured. Now, AI changes that.

LLMs can extract reasoning from emails, transcripts, and comments

Agents introduce structured checkpoints (propose → edit → approve)

Every human correction becomes a signal of judgment

Example: An AI agent suggests a pricing proposal. The sales rep adjusts it and adds context: “competitive pressure from X.”

That edit is not noise. It’s a decision trace - what the system missed and what actually mattered.

And as more workflows become agent-driven, this kind of signal becomes unavoidable.

What used to be implicit (intuition, experience, judgment) starts becoming explicit, structured, and learnable.

This creates something enterprise software never had before: a compounding loop of decision-making.

But here’s the important part - most incumbents won’t capture this.

Because they sit in the wrong place.

Systems like Salesforce store the current state, not the decision context

Warehouses like Snowflake see data after decisions are made

Neither sits at the moment where decisions actually happen

The real opportunity sits in the write path - the point where decisions are made, modified, and approved.

That’s where reasoning still exists.

And that’s why a new category is emerging: systems that don’t just store data, but capture how decisions are made across an organisation.

If this works, the implications are massive:

Enterprise value shifts from features → proprietary decision history

Systems move from “what happened?” → “Why did it happen?”

Eventually → “What should we do next?” (prediction layer)

And unlike model capabilities, this kind of data compounds uniquely for each company.

The takeaway is simple: Consumer companies built moats by understanding user behaviour. Enterprise companies will build the next generation of moats by capturing how decisions are made.

And for the first time, that data is actually becoming visible.

Is the real edge in VC picking the best startup or picking the right category early?

Most people think venture capital is about selection.

Finding the best founder.

Backing the strongest product.

Winning access to the top deal.

But a widely shared thread by Bessemer investor Aditya Nidmarti flips that idea completely. His argument is simple, but uncomfortable:

The biggest returns in venture don’t come from picking the best company.

They come from being early to the right category.

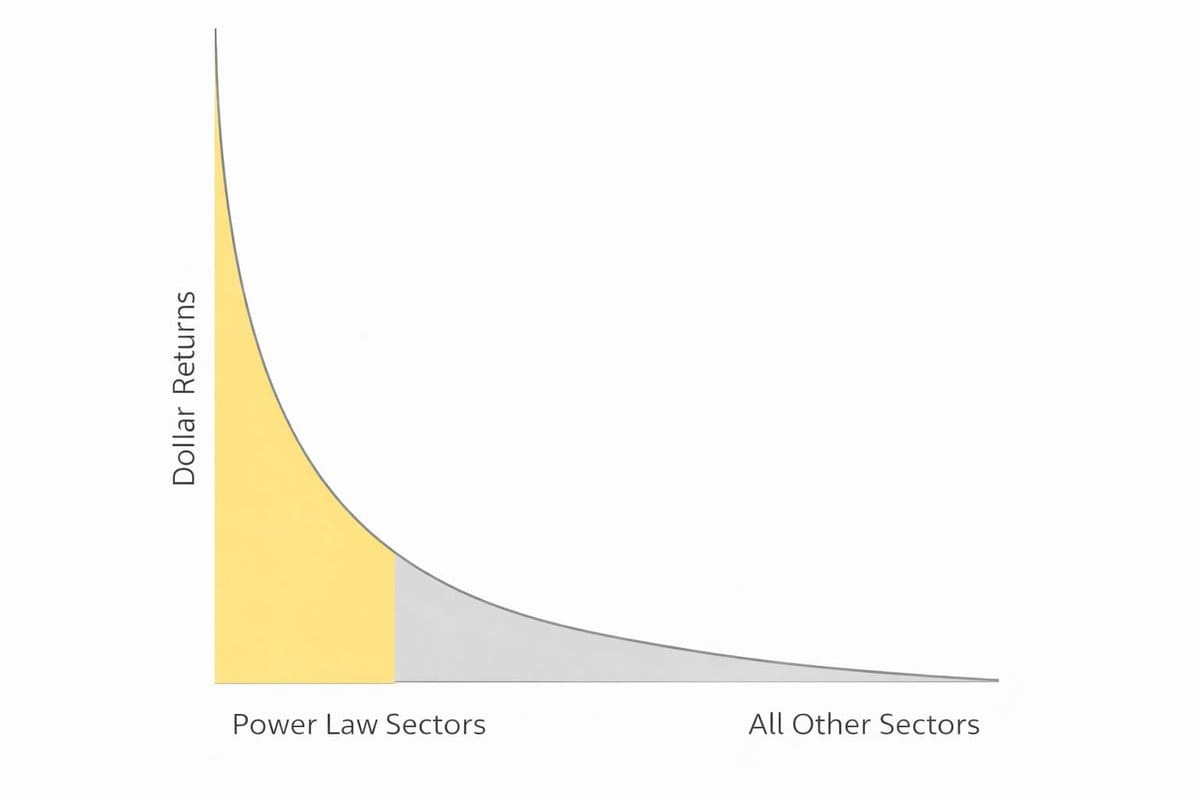

If you look at how venture returns actually play out, this starts to make sense. Returns don’t distribute evenly - they follow a power law. A small number of sectors end up driving a disproportionate share of outcomes, while everything else contributes marginally.

That’s what the chart above is really showing. A few “power law sectors” generate most of the dollars. The rest of the market matters far less than we like to believe.

And historically, these sectors weren’t hidden. They were visible - but ignored or underestimated.

In the early 2000s, internet media and marketplaces were clearly emerging

Around 2010, cloud and mobile were already showing strong signals

By 2020, AI was visible to anyone paying attention to frontier research

The investors who captured the most value didn’t just pick winners within these categories. They concentrated on the category before consensus formed.

That distinction matters more than it seems.

Because once a category becomes obvious, the game changes:

More capital flows in

Competition increases

Entry prices rise

Outcomes get diluted across more players

At that point, selection starts to matter more - but the biggest alpha has already been captured.

One of the most interesting things is around the time horizon.

Trying to predict 10 years out is mostly speculation. Trying to invest based on what’s already obvious is too late.

The real edge sits in a narrower window. Around 5 years out. This is where things get interesting:

Early signals are visible (research, prototypes, early startups)

Adoption curves are starting to take shape

But capital hasn’t fully crowded the space yet

It’s early enough to be ahead of consensus, but grounded enough to not be guesswork.

And when you get this right, it changes how you build a portfolio. Instead of asking, “Which is the best company in this category?” You start asking, “Is this category going to matter massively?”

A great example of this is Neil Shen.

In the early 2010s, he developed a strong conviction that e-commerce in China would become even more important than retail had been in the U.S. Instead of trying to pick a single winner, he built exposure across the category by investing in roughly 15 e-commerce companies.

The result wasn’t dependent on one perfect bet. He ended up capturing multiple winners because he was right about the category itself.

That’s the deeper shift this idea points to. In venture, selection still matters - but it’s often secondary.

The first question is: Are you in a category that can produce power-law outcomes?

Only after that does it make sense to optimise for: Founder quality, Product differentiation and Execution.

Because if the category itself doesn’t produce outsized returns, even great companies can lead to average outcomes. And that’s the part most people underestimate.

They spend time trying to pick the best company in a category that may never matter.

Instead of stepping back and asking: Is this a category where outsized outcomes are even possible?

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Collide Capital, a U.S.-based venture firm founded by Brian Hollins and Aaron Samuels, has raised a $95M Fund II to back early-stage startups. (Link)

Eclipse, a Palo Alto, CA-based venture capital firm, raised $1.311 billion for two funds. (Link)

Futurepresent, a NYC, Berlin, and Munich, Germany-based venture capital firm backing AI startups in the US and Europe, launched with its first $300M vehicle. (Link)

Zero Shot, a U.S.-based VC fund founded by former OpenAI leaders, has raised $20M in its first close toward a $100M target to invest in early-stage AI startups. (Link)

Gateway Capital Partners, a Milwaukee, Wisconsin-based venture capital firm, held the first close of its $25m targeted second fund. (Link)

New Startup Deals

Ridge AI, a Seattle, WA-based AI dashboard and data agents platform, raised $2.6M in Pre-Seed funding. (Link)

Satellites on Fire, a Buenos Aires, Argentina-based fire protection startup, raised $2.7M in Seed funding. (Link)

Trent AI, a London, UK-based agentic security company, raised $13M in Seed funding. (Link)

Cyberhill Partners, an Austin, TX-based enterprise AI services firm, received a strategic investment of up to $11M from Baleon Capital. (Link)

Insight Health, a NYC-based clinical AI platform for healthcare, raised $11M in Series A funding. (Link)

Mezza, a Dubai, UAE-based hospitality platform, raised an undisclosed amount in Seed funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Partnerships & Community Manager - Pear VC | USA - Apply Here

Investment Analyst Intern - NAV Capital | Dubai - Apply Here

Finance Associate - RA Capital | USA - Apply Here

Vice President, Investor Relations - General Atlantic - Apply Here

PE & VC Partner Manager - Dealhub | UK - Apply Here

Associate / Senior Associate - Stepstone Group | Italy - Apply Here

Investment Analyst - Lunicorn Venture | UK - Apply Here

Program Manager - a16z | USA - Apply Here

Chief of Staff - Greycroft | USA - Apply Here

Associate or Senior Associate - AI - BVP | USA - Apply Here

Venture Fellow - age1 | USA - Apply Here

Investment Associate - 500 Global | USA - Apply Here

Associate, Flagship Europe - Energy Impact Partner | USA - Apply Here

Venture Capital Associate - Sky9 Capital | USA - Apply Here

Investment Summer Associate - AI Tooling - M13 | USA - Apply Here

Event Marketing Manager - AI Fund | USA - Apply Here

PARTNERSHIP WITH US

Get your product in front of over 115,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

by the time everyone agrees AI is the play the best entry prices are already gone

I built a model that sits between the decision and execution layer!