Where AI seed investors are most likely to find outliers. | Are you overpaying your first hire with equity?

a16z guide on building waitlists in 2026 & Things founder should know before signing a Shareholders Agreement.

👋 Hey, Sahil here — Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

Where AI seed investors are most likely to find outliers.

What 2025 data reveals about raising VC in 2026

Frameworks & insightful posts :

Are waitlists still worth building in 2026: a16z Guide?

What founders should know before signing a Shareholders Agreement - Free template.

Are you overpaying your first hire with equity without realising it?

Will AI raise the bar for junior engineers faster than anyone expects?

FROM OUR PARTNER - RING AI

🤝 Meet Rings: AI-powered deal flow for modern VCs

Rings is the proactive extended CRM (XRM) built for investors, by a former founder of a 9-figure VC.

The AI-native platform combines a powerful sourcing engine with relationship analytics and a comprehensive CRM.

Leading VCs are using Rings to get access to more deals, track deal flow and simplify fundraising.

Consolidate your tech stack with Rings →

🤝 PARTNERSHIP WITH US

Get your product in front of over 103,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

Where AI seed investors are most likely to find outliers.

Every AI cycle produces noise. What matters is where outcomes compound, not just where capital is flowing. A recent PitchBook analysis looked at AI subsectors through one narrow but revealing lens: IPO exit predictor scores, a signal for where venture-scale outcomes are statistically more likely.

A few patterns stand out.

First, agentic commerce infrastructure is quietly emerging as the strongest outlier candidate.

Commerce has historically been the on-ramp for every major platform shift, internet, mobile, cloud, and AI are following the same script. What changes this time is autonomy.

Payments, identity, fraud, loyalty, and inventory systems are being rebuilt so software can transact without humans in the loop. That makes the infrastructure layer, not consumer apps, the long-term value capture point.

Second, AI-driven drug discovery is moving from promise to economic inevitability.

As AI improves trial design and success rates, the bottleneck shifts downstream. More trials mean more demand for tooling, data infrastructure, and clinical operations software.

Analysts expect this to expand the total addressable market aggressively through the decade, not because drugs get cheaper, but because more drugs actually make it to market.

Third, AI protection and defence-adjacent systems are benefiting from a similar dynamic: Autonomy replaces humans in high-stakes environments.

Edge computing and real-time decisioning are enabling faster response systems, whether in cybersecurity or physical defence.

The complexity here is not a bug; it’s the moat.

Finally, autonomous drones and swarms represent a classic early-cycle opportunity.

Fully coordinated land, sea, and air swarms are still hard to execute, but that difficulty creates asymmetry. As AI-first players replace human-piloted systems, legacy hardware and sensor providers face margin and relevance pressure.

Taken together, the signal is consistent:

Outlier returns are clustering below the application layer

Infrastructure that enables autonomy, not just intelligence, is where durability lives

Complexity and regulation are acting as filters, not deterrents

For seed investors, the takeaway isn’t to chase what’s loud. It’s to focus on where AI changes system behaviour, not just user experience. That’s where platform-scale outcomes tend to form.

What 2025 data reveals about raising VC in 2026

Raising venture capital is no longer about whether money exists; it’s about whether you fit the narrow lanes capital is flowing into. 2025 data makes that clear. Capital was active, but increasingly selective, and the gap between winners and everyone else widened fast.

In a recent breakdown shared by Peter Walker using Carta data, a few structural shifts stood out that founders heading into 2026 should internalise early.

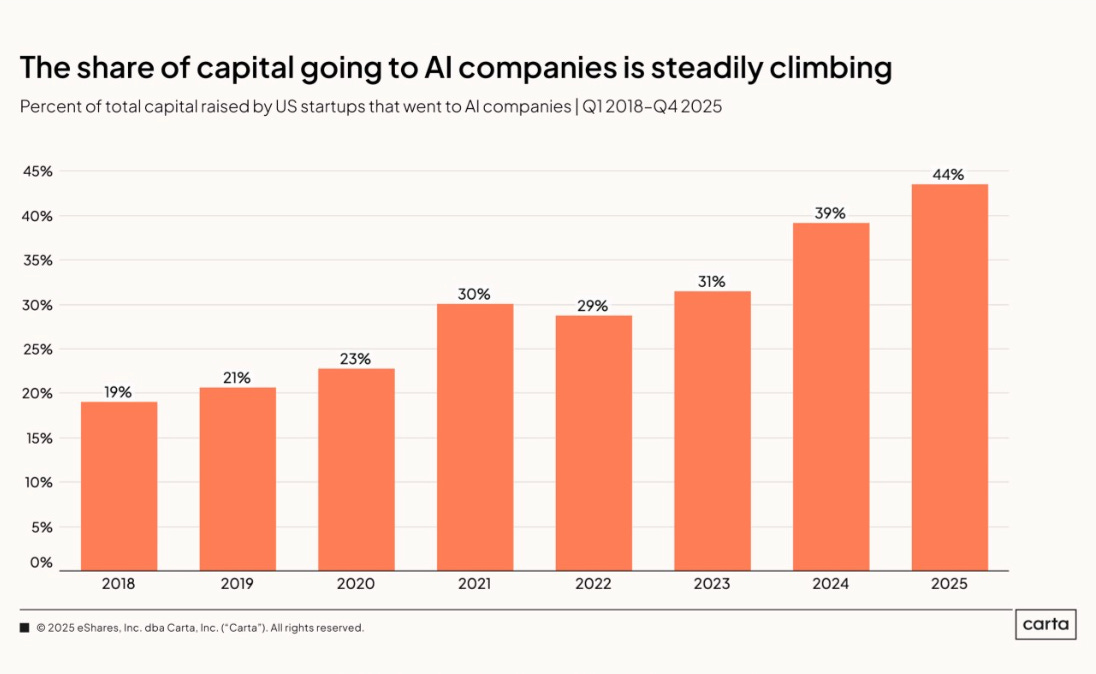

First, AI has become the default lens for venture decision-making.

About 44% of all capital deployed went into AI companies. Definitions vary, but the implication doesn’t. If you’re building software without a credible AI angle, investors now start from scepticism.

The question isn’t “why AI?” anymore, it’s “why not?”

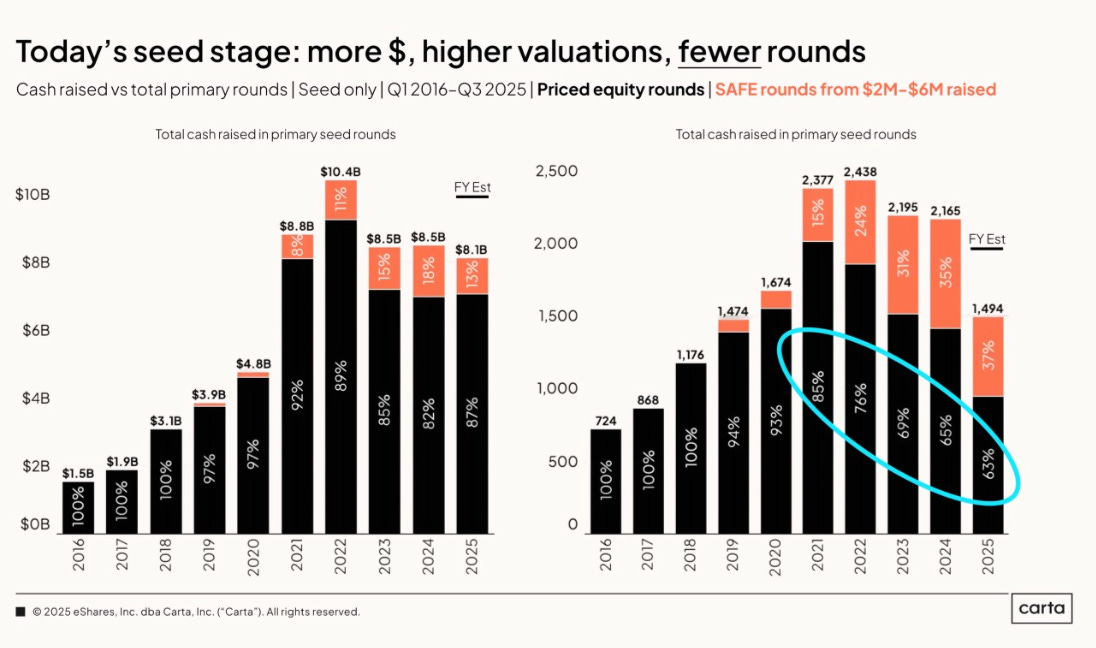

Second, more money moved, but to fewer companies.

Early-stage dollars increased year over year, yet fewer startups actually raised. VCs concentrated capital into a smaller number of high-conviction bets, often at aggressive prices.

This isn’t a cautious market; it’s a selective one.

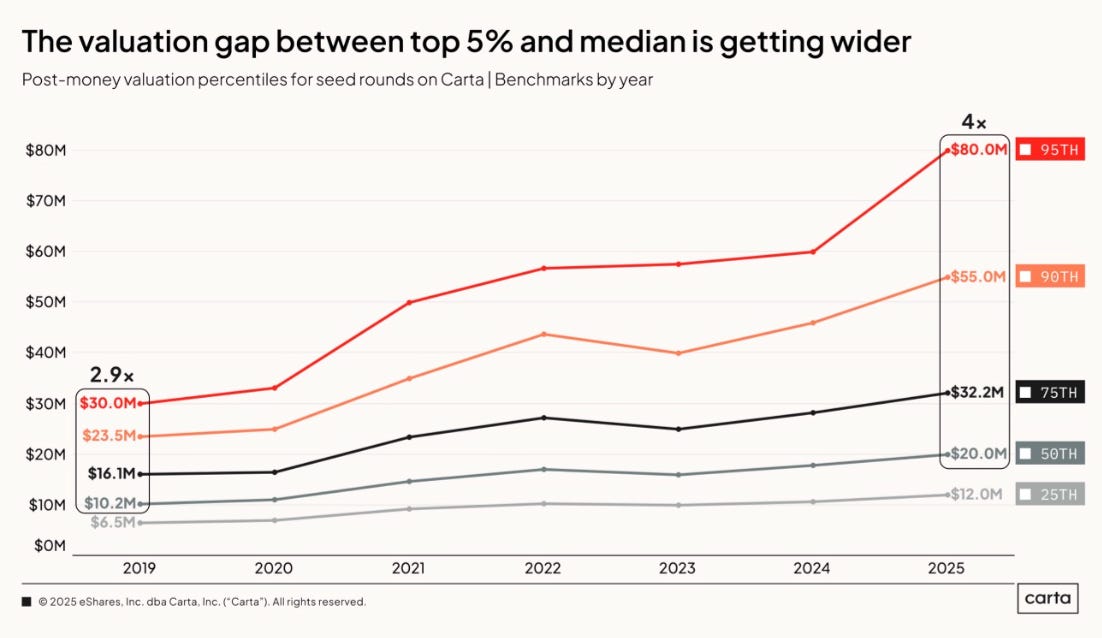

Third, valuation dispersion has reached extremes.

The gap between median seed valuations and the top 5% is wider than it’s ever been. Headlines about eye-watering seed rounds aren’t wrong; they’re just describing a tiny slice of the market.

For most founders, those numbers are irrelevant benchmarks.

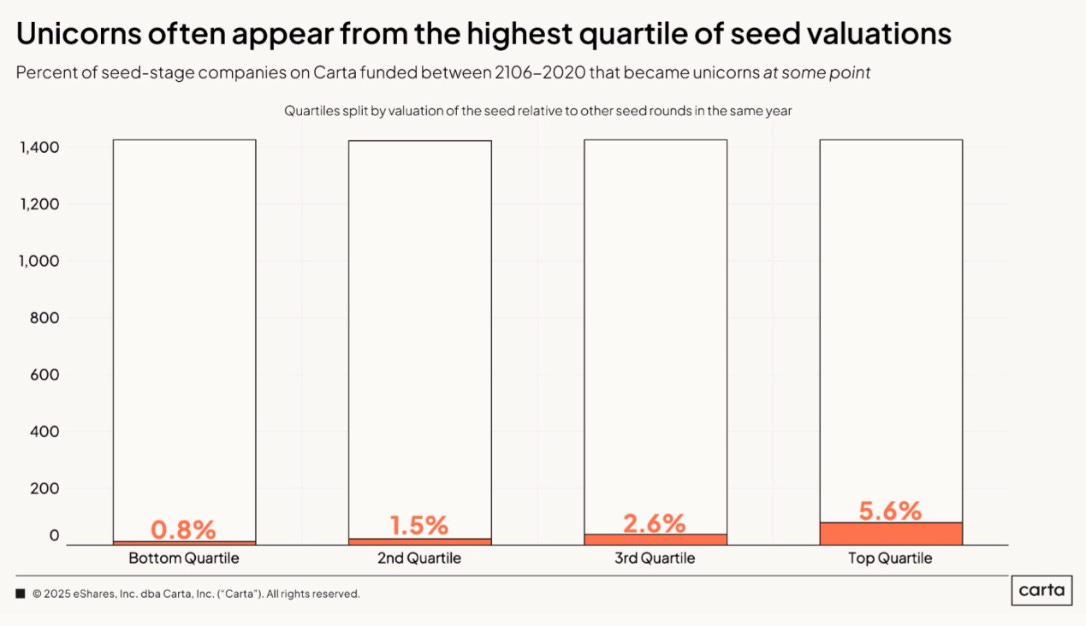

What’s often missed is that seed valuations still matter.

Looking at 5,700 seed rounds from 2016–2020, only 2.6% ever became unicorns. But companies in the top quartile of seed valuations were far more likely to reach that outcome.

High seed pricing isn’t random; it’s correlated with future valuation trajectories, even if it’s not causal.

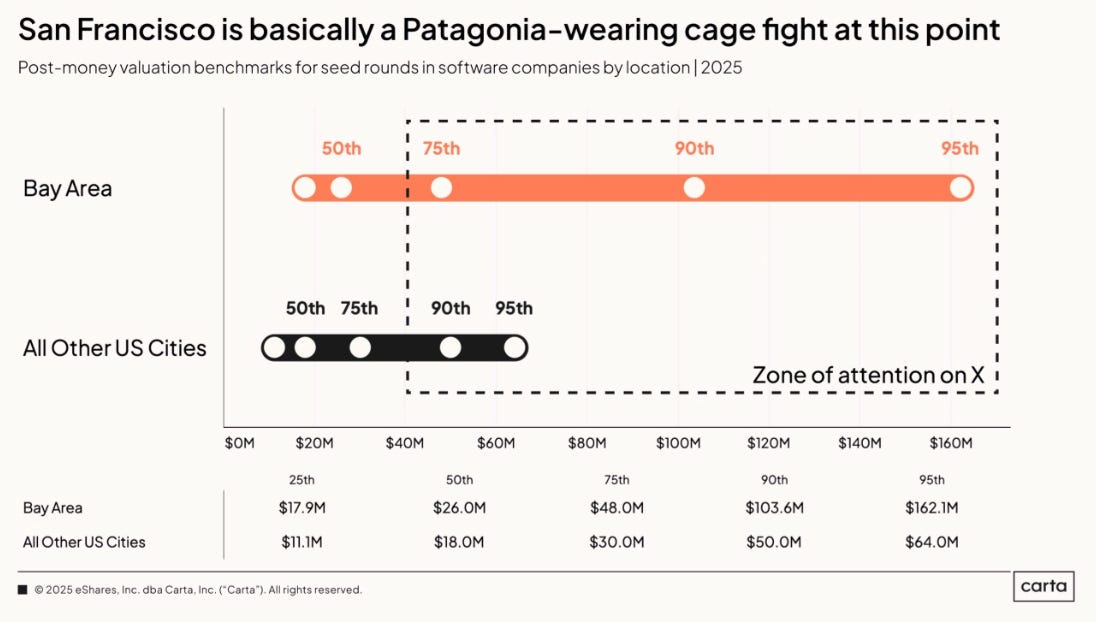

Finally, geography still shapes outcomes.

San Francisco operates on a different valuation curve entirely. The top-end numbers seen in the Bay simply don’t show up in most other markets.

That doesn’t mean great companies can’t be built elsewhere, but it does mean expectations, comps, and fundraising dynamics diverge quickly by location.

The 2026 fundraising environment is shaping up to reward sharp positioning, clear narratives, and structural alignment with where capital is already moving. The middle of the market is thinning, and outcomes are separating earlier than most founders expect.

INVESTMENT OPPORTUNITY WORTH EXPLORING

🚗 SchoolRyde is solving the $50B kids’ rideshare gap, and investors are paying attention

SchoolRyde is a ride platform purpose-built for children. It solves the daily pain point faced by millions of working parents: getting their kids to school and after-school activities safely and reliably.

By partnering with licensed taxi fleets and powering everything through its SaaS platform, SchoolRyde combines the safety of school buses with the flexibility of rideshare, all at a price families can afford.

Here’s why investors are excited:

Already live in Minneapolis with 250 drivers on the platform; next launch: Phoenix

Massive $50B+ market: $28B from school districts + $22B from private spend

Finalist out of 1,500 companies at GAMIC 2024 and PitchSF 2024

Backed by experienced founders from DocuSign, Turo, and Outschool, SchoolRyde is building the next major transportation network, starting with our kids.

There’s a massive market. There’s traction. And there’s still time to get in early.

SOMETHING MORE

🧩 Frameworks & insightful posts

Are waitlists still worth building in 2026: a16z Guide?

A few years ago, a waitlist meant hype. Ship a landing page, tweet a demo, collect thousands of emails, feel good. Today, that playbook is mostly broken. Attention is harder, inboxes are crowded, and “cool idea” signups rarely turn into revenue.

This shift was neatly unpacked by a16z speedrun in their breakdown on modern waitlists, and the core idea is simple but uncomfortable: a waitlist isn’t a vanity metric anymore. It’s a filter.

The founders who are winning in 2026 are using waitlists as a quality control system, not a popularity contest.

Here’s what actually matters now.

In the past, founders obsessed over list size. Today, the only thing that matters is what happens after someone joins.

Research shows that if you invite users within a month, waitlist-to-paid conversion can hit ~20%. Wait longer than three months, and it often drops below 10%. Big lists decay fast. Waitlists rot if you don’t activate them.

So the real question founders should be able to answer isn’t “how many people signed up?” It’s:

Who exactly joined

Why did they join now

What problem do they think you solve

And how many of them will actually take the next step

Anything else is just noise.

What does doing it right look like in practice?

The best founders now design waitlists backwards from intent.

Take Day AI. They didn’t launch early. They waited until they had a crisp story, then created a single “spike moment, a coordinated announcement across press, owned content, and social. Everything pointed to one conversion surface: the waitlist. The result wasn’t just volume, it was alignment with their sales capacity.

Another smart pattern came from Paid AI. They treated the waitlist as an intent ladder, not a dead end. Instead of stopping at an email, they progressively asked for more commitment:

email

role/industry context

booking a call

eventually, money

This is the key mental shift: your waitlist should qualify users, not just store them. Cash, even a small amount, is the strongest signal you’ll ever get.

And if you’re building hardware, this matters even more. Taya didn’t ask people to “stay tuned.” They asked for preorders. Real money. On launch day, they sold one unit every four minutes. That did two things at once: it validated demand before manufacturing, and it revealed exactly who the real customers were. That insight shaped everything that followed, from messaging to roadmap.

So a waitlist is no longer about hype signalling. It’s about learning faster and de-risking earlier. It should tell you who is serious, what they’re willing to do next, and how quickly you can move them forward.

If your waitlist can’t help you prioritise, segment, invite quickly, and measure conversion, it’s not an asset; it’s a distraction.

Build your waitlist like a machine, not a mood board.

What founders should know before signing a Shareholders Agreement - Free template.

Airtree shared a solid open-source SHA template, but most early founders still underestimate what the SHA controls. This isn’t a legal formality; it’s the document that decides who has power, who gets diluted, and who wins disagreements inside your company.

Here’s the compact founder-focused version.

What the SHA really does

A SHA is the private rulebook for how your startup runs. Your default constitution is generic; the SHA lets you define how decisions actually happen, who votes, who controls the board, how shares move, and how conflicts get resolved.

Board control and decision-making

Early teams blur the lines between founders and board, but once investors come in, the SHA locks that structure. A few things it typically settles:

How directors are appointed or removed

Who gets a board seat

How many seats exist

What vote is required to change board composition

Get this wrong and you can lose control long before Series A.

Who decides what

Founders often assume they can make most decisions themselves. The SHA decides otherwise.

Generally:

Shareholders vote on big structural matters (remove directors, amend the constitution, wind up the company)

The board handles hiring, budgets, financing, issuing shares, and approving a sale

Some investors also ask for specific veto rights. Understand every veto before you sign; one line can change the power dynamic for years.

Voting thresholds

This is where many founders sleepwalk into giving minority investors blocking power.

Common thresholds:

50% for standard decisions

≥75% for major decisions

100% (unanimous) for a small set of sensitive matters

The fewer decisions that require 75% or 100%, the safer you are.

Share rules that matter most - Most real conflicts happen around new funding, exits, or someone selling shares. Three clauses determine how that plays out:

Pre-emptive rights - Existing shareholders get the first right to buy new shares or buy a selling shareholder’s shares. This protects everyone from unexpected dilution, but it also slows down deals if written poorly.

Drag-along rights - If the majority wants to sell the company, the minority can be forced to sell too. It keeps an acquisition clean. The key thing for founders:

Check the drag threshold. If it’s too low, you can be forced into a sale you don’t want.Tag-along rights - If the majority shareholders sell, minority shareholders can join and sell on the same terms. This stops control from shifting to a stranger without everyone being protected.

Handling disputes

Good SHAs try to prevent legal battles from exploding. Usually, the process is simple:

founders + shareholders try to negotiate

If that fails, a neutral mediator steps in

Only after that can anyone take legal action

This saves time, money, and relationships.

You can also check out our Startup Legal Document Pack – Essential Legal Docs for Founders.

Are you overpaying your first hire with equity without realising it?

One of the easiest ways founders quietly mess up their cap table is very early. The first few hires feel equally risky, equally important, and emotionally, you want to treat them the same. But real data shows that equity should drop much faster than most founders expect.

This insight comes from Jason Lemkin, based on Carta’s State of Seed data covering ~50,000 startups. And the pattern is sharper than most pitch-deck math assumes.

Here’s the part most founders miss: only your very first hire truly belongs in the “founding team economics” bucket.

Everyone after that moves into a different risk-reward zone much faster than intuition suggests.

What the data actually shows when you zoom out.

Your first hire sits at a median of ~1.5% equity. That already feels lower than what many founders assume. But the real surprise is what happens next.

The second hire drops to ~0.85%. By hire #3, you are already around ~0.5%. By hire #5, the median is ~0.33%.

This is not a gentle slope. It is a cliff.

In practice, this means:

The equity drop from hire #1 to hire #2 is about 43% for the very next person who joins.

Only the very first hire reliably crosses the 1% mark at the median.

By the fifth hire, you are already in what investors mentally bucket as normal early employee equity.

Why this matters more than founders think.

Most early cap table damage doesn’t come from one huge mistake. It comes from flattening this curve. When founders give 1-1.5% to multiple early employees, they unknowingly burn future flexibility.

Later, when you need to hire a VP of Engineering or CFO at Series A or B, those roles often need meaningful equity. And suddenly, there is nowhere clean for it to come from without painful reshuffling.

There’s also a psychological angle here. The first hire is taking an existential risk. They are joining when there is no product, no traction, and often no salary stability. Hire #4 or #5 is joining something that already exists. The data reflects that reality, even if founders emotionally don’t.

A quick note on advisors, because this is where founders often leak equity quietly.

Advisor equity is dramatically lower than what most founders assume. At the seed stage, the median advisor grant is around ~0.12%. Only the top 10% of advisors cross 0.5%, and almost nobody should touch 1% unless they are delivering something truly existential.

A useful gut check:

If this advisor disappeared tomorrow, would your company materially suffer in the next 6 months? If the honest answer is no, they should not be anywhere near 1%.

So, think of early equity as a decaying asset. It loses value fast as certainty increases. Treat your first hire as a special case, because they are. But do not let that logic spill over to hires two through five.

If you want a simple mental model:

Hire #1 is almost a co-founder substitute.

Hire #2 is a major early bet, but already less so.

Hire #3 onward is execution talent, not existential risk-taking.

The data doesn’t tell you what is right for your company. But it does tell you what normal looks like. And most founders who regret equity decisions later regret being too generous too early, not the other way around.

Use this as a calibration point before you send that next offer letter.

You can also check out out Equity dilution decisions: ownership, control, and negotiation guide for founders.

Will AI raise the bar for junior engineers faster than anyone expects?

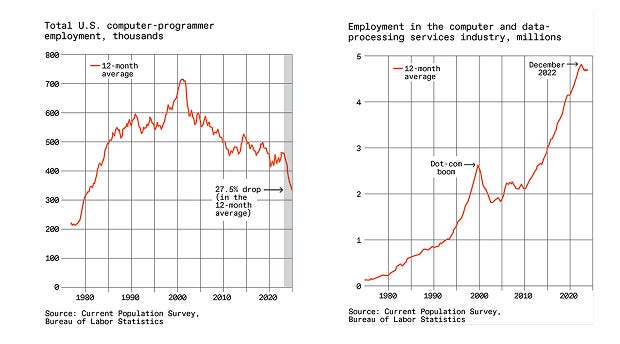

If you’re early in your engineering career, the anxiety is understandable. Entry-level hiring is down, AI tools are everywhere, and the old promise of “learn on the job by doing grunt work” is quietly disappearing. But the real shift isn’t that AI is replacing junior engineers. It’s that the definition of a junior engineer is changing.

This piece, shared by Gwendolyn Rak (with reporting by Dan Page), cuts through the noise with data and on-the-ground insight from hiring managers, universities, and labour economists.

Here’s what actually matters.

AI is hollowing out tasks, not careers. Traditional “programmer” roles, highly structured, solitary, repetitive, have taken the biggest hit. In the US, programmer employment fell 27.5% between 2023 and 2025, while software developer roles barely moved.

That distinction is important. Writing code line-by-line is easier to automate than designing systems, understanding users, or making tradeoffs across the product lifecycle.

That’s why employers now expect juniors to operate at a higher altitude from day one. Less “ticket executor,” more “problem solver who understands context.”

What smart early-career engineers are doing differently:

They treat AI like an exoskeleton, not a shortcut. Using copilots to move faster is table stakes. Knowing when not to trust them is the differentiator.

They invest in end-to-end understanding. Employers increasingly value familiarity with the full software development lifecycle from requirements to deployment, not just syntax.

They build proof, not resumes. Side projects, internships, apprenticeships, and shipped work matter more than grades alone. AI can ship code; humans are judged on judgment.

They double down on human skills AI can’t fake. Communication, negotiation, client context, and cross-functional thinking are now career accelerators, not “soft” extras.

One uncomfortable truth the article surfaces: AI is removing the safe sandbox where juniors used to learn slowly. If machines handle the basics, humans are expected to contribute value sooner.

That puts pressure on education systems too. Apprenticeships and hands-on models may matter more than traditional coursework in closing the experience gap.

Ao AI doesn’t lower the ceiling for early-career engineers, it removes the floor. There’s less room to hide, but far more upside for those who adapt early.

If you learn to think in systems, use AI deliberately, and build real things in public or on teams, you won’t be competing with AI. You’ll be competing with people who refuse to evolve, and that’s a much easier race to win.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Niko Bonatsos, known for early bets on Discord and Mercor, has departed General Catalyst after years of leading its seed strategy to launch a new early-stage VC firm. (Link)

Lux Capital, based in the U.S., focuses on frontier science, AI, and defence tech, and has raised a $1.5 billion ninth fund — its largest to date. (Link)

AppWorks, a Taipei-based startup accelerator, has closed Fund IV at $165 million, less than half its original $360 million target. (Link)

New Startup Deals

Autonomous Technologies Group (ATG), a NYC- and San Francisco, CA-based AI research lab focused on solving complex financial problems, launched with $15m in pre-seed funding. (Link)

i10X, a Singapore-based unified AI platform, closed a USD$1m pre-seed funding round. (Link)

AgileRL, a London, UK-based startup accelerating the development of reinforcement learning for training AI models, raised a seed funding round. (Link)

Moto Finance Inc., a NYC-based financial technology company, raised $1.8m in pre-seed funding. Backers included Cyber Fund and Eterna Capital. (Link)

Tesoro XP, an Austin, TX-based provider of a rewards platform that enables retailers to fund in-game currency for gamers, raised $5.4m in seed funding. (Link)

Coinbax, a NYC-based programmable trust layer for stablecoin payments, raised $4.2m in seed funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Ventures Analyst/Associate - Plug and Play Tech Centre | USA - Apply Here

Investment Fellowship - H7 Bio Capital | Remote - Apply Here

Analyst - BDC Capital | Canada - Apply Here

Program Manager - gener8tor | USA - Apply Here

Associate - Health Velocity Capital | USA - Apply Here

Associate - Mana Venture | USA - Apply Here

Summer Fellowship 2026 - Coastanova Venture | USA - Apply Here

Portfolio Management Intern - LVL1 Accelerator | India - Apply Here

Associate, Growth Equity - Adam Street Partner | USA - Apply Here

Venture Relations Associate - Angellist | USA - Apply Here

VC Fellowship - 1752 VC | USA - Apply Here

Investor - First Round Capital | USA - Apply Here

Analyst - Griffin Gaming Partner | USA - Apply Here

Partnership Manager - Sixthirty | USA - Apply Here

VC Associate - Proglobal Search | UAE - Apply Here

Visiting Analyst - Seedcamp | UK - Apply Here

PARTNERSHIP WITH US

Get your product in front of over 102,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator