Which AI sectors are most likely to produce venture-scale exits?| The competitive strategy AI companies are copying from Google.

Framework to study new market and build expertise shared by Twitter PM turned healthcare founder.

👋 Hey, Sahil here - Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Which AI sectors are most likely to produce venture-scale exits?

The competitive strategy AI companies are copying from Google

How to study a new market and build expertise - tactics from a Twitter PM turned healthcare founder.

FROM OUR PARTNER - ACCIO

Accio Work: your agentic team for real business

Meet Accio Work, the workspace for business owners and solopreneurs. Our AI agents handle sourcing, supplier negotiation, store management, and marketing on autopilot.

With verified skills and APIs, it executes while you stay in control. Powered by Alibaba.com data, it manages execution seamlessly. No setup, just results.

Try Accio Work now - 7 Days Free →

📜 DEEP DIVE

Where AI seed investors are most likely to find outliers.

Every AI cycle produces noise. What matters is where outcomes compound, not just where capital is flowing. A recent PitchBook analysis looked at AI subsectors through one narrow but revealing lens: IPO exit predictor scores, a signal for where venture-scale outcomes are statistically more likely.

A few patterns stand out.

First, agentic commerce infrastructure is quietly emerging as the strongest outlier candidate.

Commerce has historically been the on-ramp for every major platform shift, internet, mobile, cloud, and AI are following the same script. What changes this time is autonomy.

Payments, identity, fraud, loyalty, and inventory systems are being rebuilt so software can transact without humans in the loop. That makes the infrastructure layer, not consumer apps, the long-term value capture point.

Second, AI-driven drug discovery is moving from promise to economic inevitability.

As AI improves trial design and success rates, the bottleneck shifts downstream. More trials mean more demand for tooling, data infrastructure, and clinical operations software.

Analysts expect this to expand the total addressable market aggressively through the decade, not because drugs get cheaper, but because more drugs actually make it to market.

Third, AI protection and defence-adjacent systems are benefiting from a similar dynamic: Autonomy replaces humans in high-stakes environments.

Edge computing and real-time decisioning are enabling faster response systems, whether in cybersecurity or physical defence.

The complexity here is not a bug; it’s the moat.

Finally, autonomous drones and swarms represent a classic early-cycle opportunity.

Fully coordinated land, sea, and air swarms are still hard to execute, but that difficulty creates asymmetry. As AI-first players replace human-piloted systems, legacy hardware and sensor providers face margin and relevance pressure.

Taken together, the signal is consistent:

Outlier returns are clustering below the application layer

Infrastructure that enables autonomy, not just intelligence, is where durability lives

Complexity and regulation are acting as filters, not deterrents

For seed investors, the takeaway isn’t to chase what’s loud. It’s to focus on where AI changes system behaviour, not just user experience. That’s where platform-scale outcomes tend to form.

THIS WEEK’S TOP STARTUP DEAL (CLOSING SOON)

🧩 Investors are backing an impactful platform reshaping a $900B global market…

For decades, most artisans have been locked out of global commerce. Middlemen take the margins. Platforms are fragmented. Growth is limited.

That’s changing.

NOVICA has already helped send $142M+ directly to makers worldwide - building the infrastructure, trust, and global network others don’t have.

Now, with their new wholly owned division – Handmade.com – the next phase begins.

Handmade.com is a creator-first platform where artisans can easily list products using AI tools and sell globally. No complexity. No gatekeepers. Just access.

Why investors are leaning in:

$900B+ global handmade market, projected to reach USD $1.94 trillion by 2033

$20M+ revenue and $142M+ paid to artisans

Global fulfilment and infrastructure already built

AI-driven platform designed for exponential growth

A mission-driven model delivering fair trade impact and changing lives at scale

This is the moment where global commerce shifts from middlemen to creators, and the platform enabling that shift is here.

With the campaign closing in the next few days, this is your final opportunity to invest in NOVICA.

PARTNERSHIP WITH US

🤝 Get your brand in front of 120,000+ audience.

Our newsletter is read by 120,000+ tech professionals, founders, investors (VCs / Angel Investors) and managers around the world. Get in touch today.

📃 QUICK DIVES

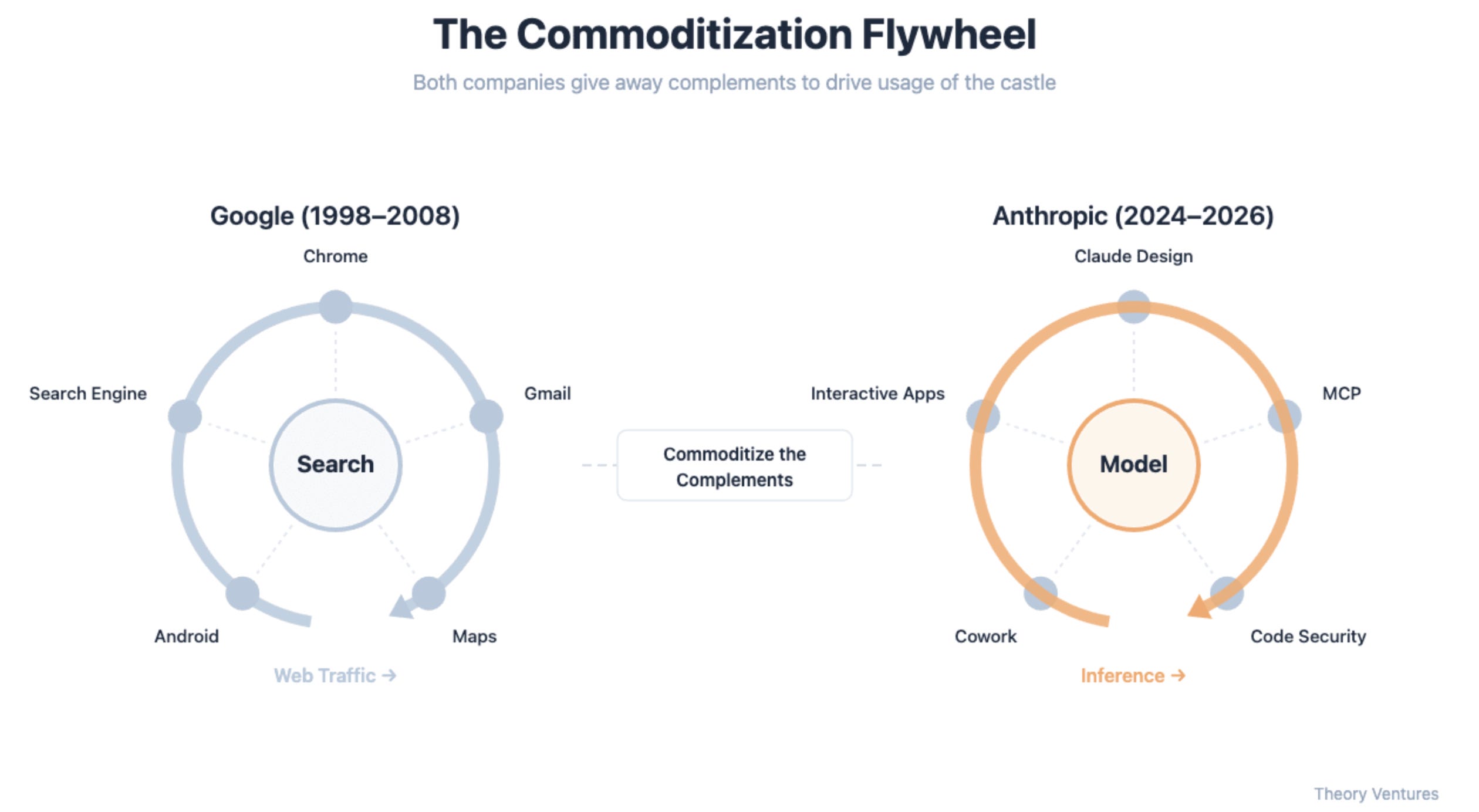

The competitive strategy AI companies are copying from Google.

There’s a pattern that quietly built one of the most dominant companies in tech.

Google didn’t just win because search was better. It won because it removed every layer between the user and search - and then made sure nothing could sit in between again.

Tomasz Tunguz from Theory Ventures recently shared this idea again in the context of AI, and once you see it, you can’t unsee it.

How Google actually built its moat

At its core, Google was always a simple business: Search → data → better results → ads → revenue.

Everything else - Gmail, Maps, Chrome, Android - was never the business. It was a distribution.

Instead of monetising these products directly, Google used them to expand the surface area of search.

Gmail made storage free → more users stayed in Google’s ecosystem

Maps removed the need for paid navigation → captured local intent

Android ensured Google wasn’t blocked on mobile

Chrome increased browsing speed → more searches per user

This wasn’t a random expansion. It was systematic. Each product removed a friction point and pushed more activity back into search.

Over time, this created a self-reinforcing loop: More usage → more data → better search → more usage.

That loop became the moat.

Anthropic (and AI companies) are doing the same thing

Now replace “search” with “model.” The playbook looks almost identical, but the surface area is much broader.

Anthropic isn’t just building a chatbot. It’s quietly surrounding the model with tools that expand where and how it gets used.

Claude Design → turns prompts into UI systems

Claude Cowork → manages files and workflows

Code Security → scans and fixes vulnerabilities

MCP → connects AI directly to data systems

Interactive apps → bundle productivity inside the model

Individually, each of these looks like a product. Collectively, they act as a distribution for the model.

The strategy is simple: the more tasks the model can handle, the more central it becomes to how work gets done.

The new flywheel: usage → data → intelligence

What made Google powerful was not just usage - it was the compounding effect of usage. AI companies are building the same loop, but with a different input.

More use cases lead to more interactions. More interactions generate more data. More data improves the model. A better model drives more usage again.

The important shift here is that AI isn’t competing for a single action like search queries. It’s competing for entire workflows.

That makes the upside - and the risk much bigger.

Why this strategy quietly kills categories

One of the most misunderstood parts of this strategy is that it doesn’t require building the best product. It only requires building something good enough and bundled.

That’s usually enough to change user behaviour. We’ve already seen this movie before.

Gmail made paid email irrelevant.

Google Maps killed standalone navigation tools.

Chrome weakened third-party browsers.

Now the same pressure is showing up again, but across a much wider set of categories.

design tools becoming features inside AI

Basic coding tools are being replaced by agents

workflow tools getting absorbed into copilots

Security checks are becoming automated layers

The shift doesn’t happen overnight. It starts slowly, then becomes default.

Where this gets more interesting (and overlooked)

Here’s something most people miss: Commoditization increases usage… but it also reshapes where value lives.

When complements become free, the value doesn’t disappear - it moves. In the AI stack, we’re already seeing this happen.

Value is shifting upward into distribution, brand, and trust. And downward into infrastructure, compute, and proprietary data.

The middle layer - tools that don’t own either- is where things get squeezed. This is why many AI wrapper products feel fragile. They sit exactly in the middle.

What this means for founders

If you’re building today, the real question isn’t “is this a good product?” It’s: where do I sit in the flywheel?

Because that determines whether you benefit from this shift or get absorbed by it.

Horizontal tools → face direct pressure from AI platforms

Deep, niche workflows → more defensible

Proprietary data or distribution → real leverage

API-dependent products → replaceable over time

The opportunity hasn’t gone away. It has just become more specific.

How to study a new market and build expertise - tactics from a Twitter PM turned healthcare founder.

Most founders try to “study” a new industry with research reports, Statista charts, or high-level TAM decks. Othman Laraki (ex-Google/Twitter PM, now co-founder/CEO of Colour, a billion-dollar healthcare company) took a different path: he learned healthcare by building into it.

Here’s a framework you can use if you’re breaking into a market you don’t know.

1. Map how money really flows (don’t stop at the buyer).

In healthcare, the patient isn’t the buyer. The insurer or employer often pays. Clinicians influence decisions, but administrators handle approvals. Laraki sat down with claims adjusters, procurement managers, and even lab operators to understand:

Who influences the decision?

Who signs the contract?

Who sets the price?

Who actually pays (and when)?

Do this for your own market. Draw a flowchart from first touch → payment collected. Until you see each actor and their incentive, you don’t understand the market.

2. Run a unit economics teardown.

Instead of guessing, Laraki decomposed the cost of delivering a genetic test, line by line. He set a target price ($250 vs. the $4,000 incumbents charged) and worked backwards:

Negotiate with suppliers (“ask for a discount” was a rule, not a hope).

Unbundle inputs (suppliers often add hidden buffers).

Spot timing incentives (end-of-quarter discounts, prepayment benefits).

Try the same: build a spreadsheet of every cost driver. Then ask, for each line item: “How can I bend this?”

3. Test whether your wedge is a feature or a solution.

Colour’s first wedge was low-cost testing. But insurers didn’t care; they priced by median cost across labs, not the cheapest option. A $250 test was just a feature. The solution buyers actually wanted? A vertically integrated cancer care clinic that reduced overall spend.

Apply this lens: if your product is a “better part,” ask who needs a “whole car.” Sometimes you need to bundle your tech into a broader solution to unlock budgets.

4. Talk to operators, not celebrities.

Instead of chasing famous doctors or regulators, Laraki reached out to genetic counsellors, lab managers, and non-famous scientists. These were the people actually running the processes Colour needed to integrate into.

Advisors were compensated simply (hourly rate, research sponsorship), not with vague equity promises.

Your move: make a list of the doers in your industry. Cold email them with a mission-driven story. They’ll tell you how transactions really happen.

5. Treat pivots as progress, not failure.

Laraki cycled through:

DTC tests (failed: CAC too high, LTV too low).

Selling via physicians (failed: billing friction too high).

Employer health plans (worked: aligned with budgets).

Expanded into a full clinic (big unlock).

Don’t cling to your first model. Every failed buyer segment is data that sharpens where the incentives align.

6. Don’t mistake false positives for traction.

Colour scored early deals because of influence (warm networks, Stripe founder referral). But those didn’t generalise. Laraki’s test: could a stranger buy this product on standard terms? If not, you don’t yet have PMF.

Run the same filter: strip away influence. Would the product still close deals?

Mini checklist founders can run this week

Map one real transaction in your target market from first touch to cash collected. Name each actor and their incentive.

Identify your product’s current status on the buyer’s ladder: feature, component, or solution. If it’s a feature, who can you bundle with to become a solution?

List the top three cost drivers and one concrete action to bend each (renegotiate, alternate supplier, process change).

Book five calls with non-celebrity operators who move money or approvals. Ask them to redline your transaction map.

Write your “no influence” test: how would a cold buyer discover, evaluate, purchase, and activate without your network?

TODAY’S JOB OPPORTUNITIES

💼 Venture Capital & Startup Jobs

Most aspiring VCs struggle with interviews, unclear expectations, no structured prep, and generic advice that doesn’t actually help. So we partnered with a leading investor group to build an all-in-one VC Interview Preparation Guide that gives you real clarity and frameworks. (Access Here)

Assistant Vice President - Temasek | Singapore - Apply Here

Investment Intern - DTCP | UK - Apply Here

Associate, Life Sciences - General Atlantic | USA - Apply Here

Analyst, Global Investment Team - 500 Global | USA - Apply Here

Associate, Data Operations - Iconiq Capital | USA - Apply Here

Investor - AI - Samsung Next | USA - Apply Here

Finance Associate - RA Capital | USA - Apply Here

Fund Controller - NFX | USA - Apply Here

Vice President, Investor Relations - General Atlantic - Apply Here

Senior Associate - RA Capital | USA - Apply Here

PE & VC Partner Manager - Dealhub | UK - Apply Here

Partner 22 -a16z | USA - Apply Here

Infra / Platform Engineer - Pear VC | USA - Apply Here

Associate / Senior Associate - Stepstone Group | Italy - Apply Here

Investment Analyst - Lunicorn Venture | UK - Apply Here

Investor (Senior Associate/Principal) - Square Peg | USA - Apply Here

Program Manager - a16z | USA - Apply Here

PARTNERSHIP WITH US

🤝 Get your brand in front of 120,000+ audience.

Our newsletter is read by 120,000+ tech professionals, founders, investors (VCs / Angel Investors) and managers around the world. Get in touch today.

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator