Why are even great startups still struggling to raise capital despite record venture funding?

Data reveals: the rise of the barbell market, why venture capital is concentrating and an experienced VC's playbook for raising in 2026.

👋 Hey, Sahil here - welcome to this edition of Venture Curator, where we break down how great startups grow, how top investors think, and what’s shaping the future of tech.

P.S. Get access to 100+ startup & VC resources, investor databases, fundraising templates, 150+ premium archive posts and exclusive startup research - all in one place.

FROM OUR PARTNER - LEGION M

🎬 Investors are backing Legion M, the world’s first fan-owned movie studio

Hollywood is controlled by a handful of studios and executives. The people who actually watch, promote, and pay for movies rarely have any ownership in what gets made.

Legion M is building the world’s first fan-owned movie studio, allowing everyday investors to own equity in a company that develops, finances, produces, and distributes films.

Why investors are paying attention:

Raised over $25M from 60,000+ investors

1.96x Revenue Growth from 2024 to 2025.

Worked on 15+ film projects with upcoming releases, including Nimrods and Coyote vs. ACME

Founded by Emmy-winning entrepreneurs behind MobiTV, one of the pioneers of mobile streaming

The company has spent nearly a decade building its community, film pipeline, and distribution capabilities. With record revenue, upcoming releases, and one of the largest investor communities in entertainment, it is entering its next phase of growth.

This is the time to back the future of fan-owned entertainment, and there are three ways to get involved:

Invest In Legion M (the studio)

When you invest in Legion M, you join over 60,000 other investors who own shares in Legion M and a stake in all of our projects. You don’t get direct royalties from any single project, but you do get an early-stage stake in the first movie studio built to be owned by fans.

Invest In The Film Fund

The Legion M Film Fund currently has a limited allocation available for NIMRODS, the comedy from Green Day & Live Nation Studios. A Film Fund investment allows you to receive returns directly from the release of NIMRODS – with the option to roll over any returns into our next film.

Get On The List

Not sure about investing? Join the Legion M community (it’s FREE) to get on the list for updates about our upcoming films Coyote vs. ACME and NIMRODS, future projects, and fan exclusives!

Legion M’s Reg CF offering is made available through StartEngine Primary, LLC, member FINRA/SIPC. Startup investments like Legion M are speculative, illiquid, and involve a high degree of risk, including the possible loss of your entire investment.

📜 DEEP DIVE

Why are even great startups still struggling to raise capital despite record venture funding?

In February 2026, U.S. startups raised $62.5 billion across 462 deals. It was the largest single month of venture funding in recorded American history.

And it wasn’t a one-off. You’ve watched a version of that headline land every few weeks since - another record quarter, another ten-figure round, another “venture is back” victory lap - right up to the month you’re reading this. The drumbeat hasn’t stopped. If anything, it’s gotten louder.

If you’re a founder and then opened your own pipeline - the four VCs who ghosted you after the second call, the term sheet that’s been “with the partners” for three weeks and felt a quiet, specific kind of crazy.

Because the numbers say it’s the best funding environment in a decade. Your bank account says otherwise.

You’re not imagining it. And you’re not bad at fundraising.

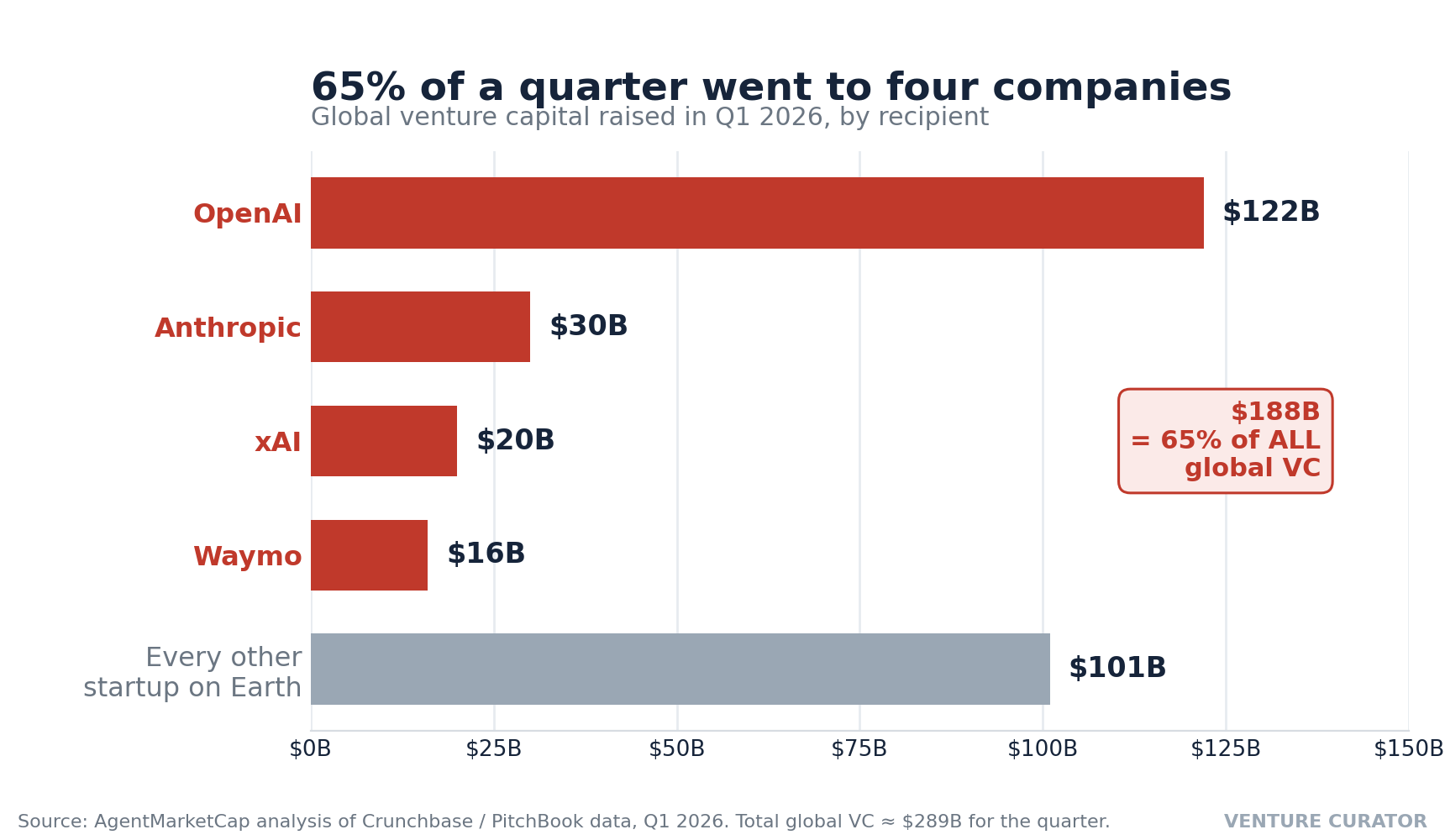

That $62.5 billion was almost entirely two companies. Anthropic raised $30 billion. Waymo raised $16 billion. Two names took roughly three-quarters of the biggest funding month in history before the other ~460 startups split what was left.

This is the story nobody tells you cleanly: venture capital is having its best year on paper and one of its hardest years in practice - at the same time. The headline number and the founder’s reality have completely decoupled.

The market has become a barbell. Enormous weight on one end. A thinning bar in the middle, where almost every real company actually lives.

This edition is about that gap. Specifically:

The anatomy of the barbell - exactly how concentrated the money has become, with the numbers

Why it’s happening - the mechanics pulling capital toward a handful of names (it’s not a fad; it’s structural)

The famine on the other end - what the data says about your raise: seed, Series A, the graduation cliff

What to actually do about it - a positioning playbook for founders who will never be the $30B headline, and don’t need to be

The opportunity hiding in the barbell - where the fleeing capital leaves white space: cheaper talent, the wide-open application layer.

What to watch - the live signals that tell you when the bar is about to widen back out.

If you raise in the next 18 months, the difference between understanding this market and fighting the last one is the difference between a clean round and a slow death by “we’d love to see more traction.”

Let’s get into it.

The anatomy of the barbell

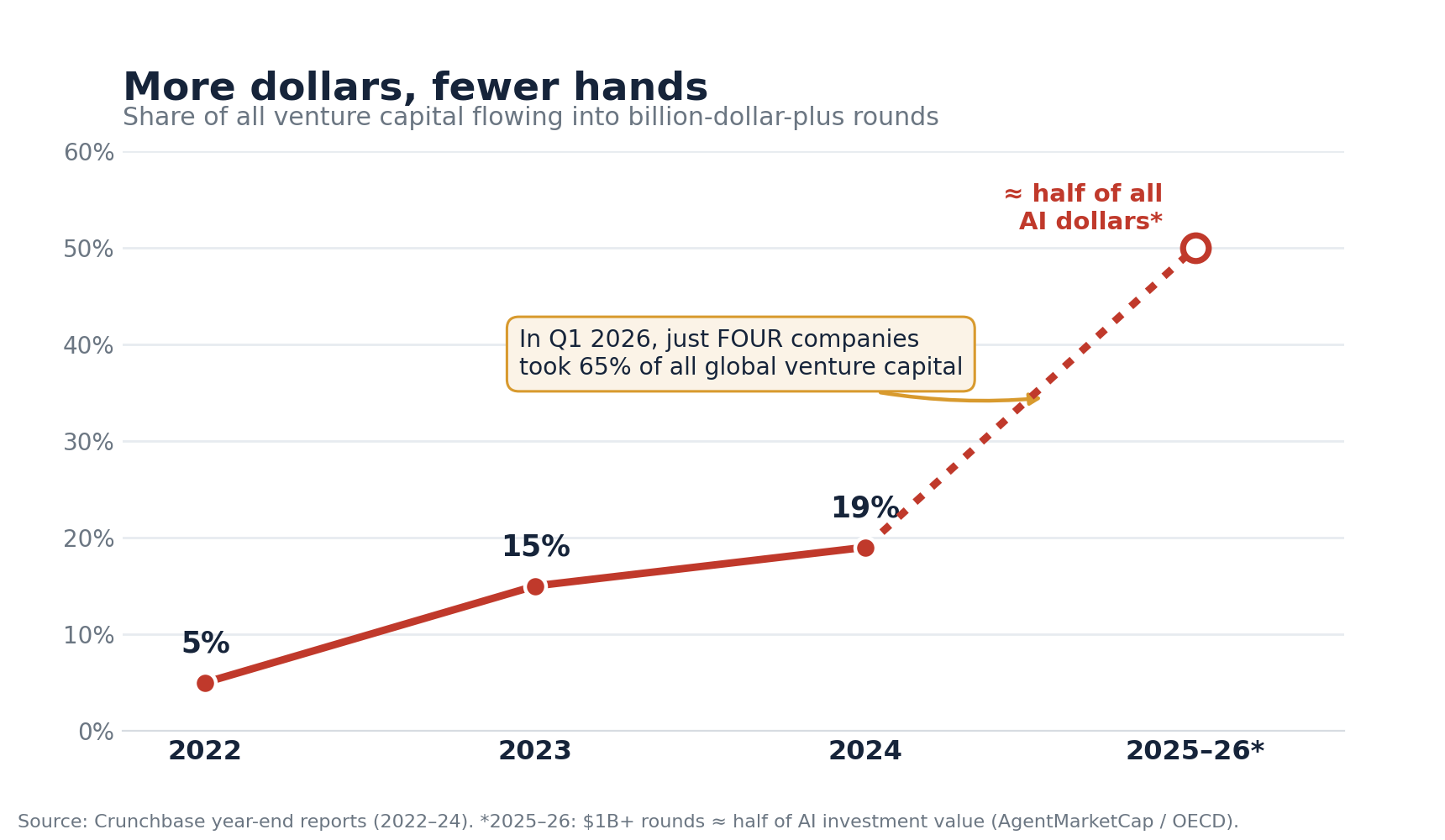

In Q1 2026, just four companies - OpenAI, Anthropic, xAI, and Waymo - raised $188 billion between them. That was 65% of all global venture capital for the quarter. Sixty-five per cent. To four companies.

Everyone else on the planet - every SaaS startup, every biotech, every fintech, every consumer app, every climate company, in every country - split the remaining third.

This isn’t a one-quarter fluke. It’s the steep end of a curve that’s been bending for years.

Go back to 2022: rounds of $1 billion or more made up just 5% of all venture dollars. By 2023, that share hit 15%. By 2024, 19%. Into 2025 and 2026, billion-dollar rounds came to represent roughly half of all the money invested in AI - and AI is now most of the market. The money didn’t shrink. It pooled.

The concentration is geographic too.

In 2025, the San Francisco Bay Area pulled in $126 billion of global AI funding - but $113 billion of that went to just 92 companies raising rounds of $100 million or more. A few dozen addresses within a few square miles absorbed more capital than most countries’ entire startup ecosystems.

So when you read “record venture funding,” translate it. It does not mean capital is widely available. It means a small number of companies are absorbing staggering sums, and the average reported deal is being dragged upward by a handful of giants. $62.5 billion across 462 deals is an average of $135 million per deal - a number that describes almost no real company’s actual round.

The barbell is real. Now the more useful question: why?

Why this is happening (and why it won’t reverse soon)

(Subscribe to Venture Curator Premium and get 20% off forever.)