The buy-vs-build framework for building defensible SaaS in AI era. | Only 99 of 619 Unicorns have exited. What changed?

Data shows it's getting hard to lauch a new VC fund. & The 3-Layer AI sales stack every founder should build.

👋 Hey, Sahil here - welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

Why is it getting harder than ever to launch a new VC fund?

Only 99 of 619 Unicorns have exited. What changed?

What does a fund-returning company actually look like?

Frameworks & insightful posts :

The buy-vs-build framework for building defensible SaaS in AI era.

Framework: The 3-Layer AI sales stack every founder should build.

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

FROM OUR PARTNER - GALACTIC FED

Marketing agency for fast-scaling companies and early startups…

The hidden team behind unicorn growth for Suno, Jeeves, and Picsart.

We’ve hired agencies. Most were bad. So we built one for founders like us.

Free growth plan for Venture Curator readers. We’ll show you the levers to scale fast in your niche over 6 months.

WORK WITH US

🤝 Partnership With Us

Get your product in front of over 125,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

Why is it getting harder than ever to launch a new VC fund?

Breaking into venture capital has always been difficult. But today, the challenge isn’t just proving you can pick great startups - it’s convincing LPs to back a new fund when most of the industry’s capital keeps flowing to the same established firms.

Dan Grey from Odin recently shared data showing that this shift isn’t a temporary consequence of the 2022 downturn. It’s a structural change that has been building for more than a decade.

The chart tells the story.

In 2015, emerging managers raised nearly 60% of all US venture capital.

By Q1 2026, that share had fallen to just 9.1%, meaning more than 90% of venture fundraising is now captured by experienced, incumbent firms.

Grey argues this happens because venture behaves asymmetrically during both booms and busts.

When capital floods into the asset class, most of it doesn’t create new managers - it simply makes the largest firms even larger. And when markets contract, LPs become more conservative, pulling capital away from first-time funds and concentrating it further among established brands.

That creates a structural “ratchet effect.” Every fundraising cycle pushes the industry toward greater concentration, but very little pulls it back.

Several forces reinforce this dynamic:

Large LPs naturally favour large funds. Pension funds, sovereign wealth funds and endowments need to deploy hundreds of millions of dollars efficiently. Writing a handful of large cheques to proven managers is operationally much easier than backing dozens of emerging funds.

Incumbents benefit from stronger fundraising flywheels. Bigger funds have longer track records, deeper LP relationships and larger teams, making each successive fund easier to raise - even during difficult markets.

Emerging managers face liquidity pressure first. As exits slow and distributions decline, the smaller LPs that traditionally back first-time funds often pull back the fastest.

The result is an industry where capital increasingly flows through a smaller group of firms.

Grey believes this matters because emerging managers have historically been the investors willing to back unconventional founders, explore overlooked markets and develop conviction before everyone else notices an opportunity.

As capital becomes more concentrated, investment decisions become more concentrated too. More firms end up competing for the same founders, the same AI companies and the same market narratives, while fewer investors have the flexibility to pursue ideas outside the consensus.

This doesn’t necessarily mean the largest firms will generate worse returns. But it does change how innovation gets financed. Venture has always relied on diverse opinions and independent conviction to discover outlier companies. When capital pools around fewer decision-makers, the industry risks becoming better at funding obvious opportunities while becoming less effective at discovering the unexpected.

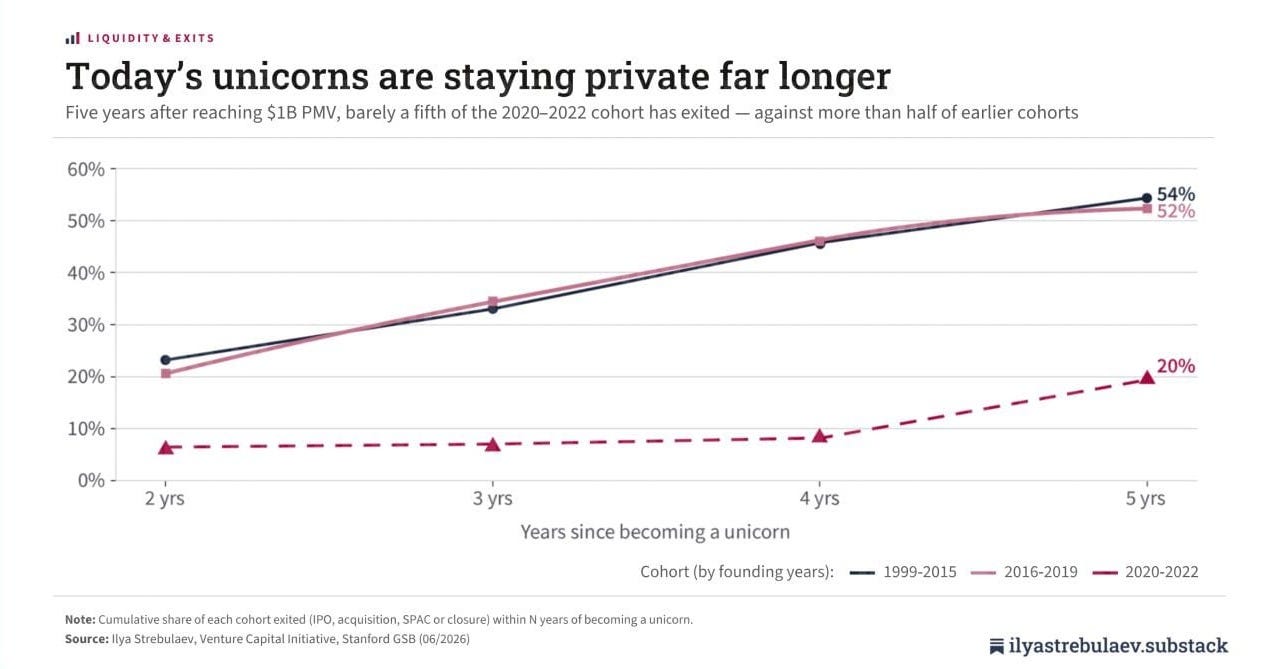

Only 99 of 619 Unicorns have exited. What changed?

Becoming a unicorn used to be the beginning of the exit journey. Within a few years, many companies would either go public or get acquired, returning capital to investors and allowing it to flow back into the startup ecosystem.

That cycle has broken down.

Stanford GSB professor Ilya Strebulaev recently shared new data showing that today’s unicorns are staying private far longer than any previous generation, deepening the venture industry’s liquidity crunch.

The numbers are striking.

Between 2020 and 2022, 619 companies reached unicorn status. Five years later, only 99 have exited, leaving 520 unicorns still private.

That’s an exit rate of just 20%.

Compare that with earlier generations of unicorns:

Companies that became unicorns between 1999 and 2015 reached a 54% exit rate within five years.

The 2016–2019 cohort reached 52% over the same period.

The 2020–2022 cohort has managed just 20%.

The slowdown appears almost immediately.

After two years, previous unicorn cohorts had already seen roughly 20–23% of companies exit. The 2020–2022 cohort was sitting at just 6%. Three years in it was 7%, and after four years, only 8% had exited.

This isn’t just about founders delaying IPOs.

Every delayed exit means founders wait longer for liquidity, employees hold stock options they can’t easily monetise, VCs struggle to return capital to LPs, and pension funds, endowments and family offices receive fewer distributions to reinvest into the next generation of startups.

It’s one reason why the venture industry is sitting on an estimated $3 trillion of unrealised value, while secondary markets have become an increasingly important source of liquidity as traditional IPOs and acquisitions remain scarce.

The venture ecosystem depends on capital constantly recycling from successful exits into new funds and new startups. When that recycling slows, the effects ripple across the entire market - from LP fundraising to founder financing.

Today’s unicorns aren’t disappearing. They’re simply staying private much longer than the venture industry was built to expect.

What does a fund-returning company actually look like?

Venture capital is built on one promise: wait long enough, and a single company can return an entire fund (power law).

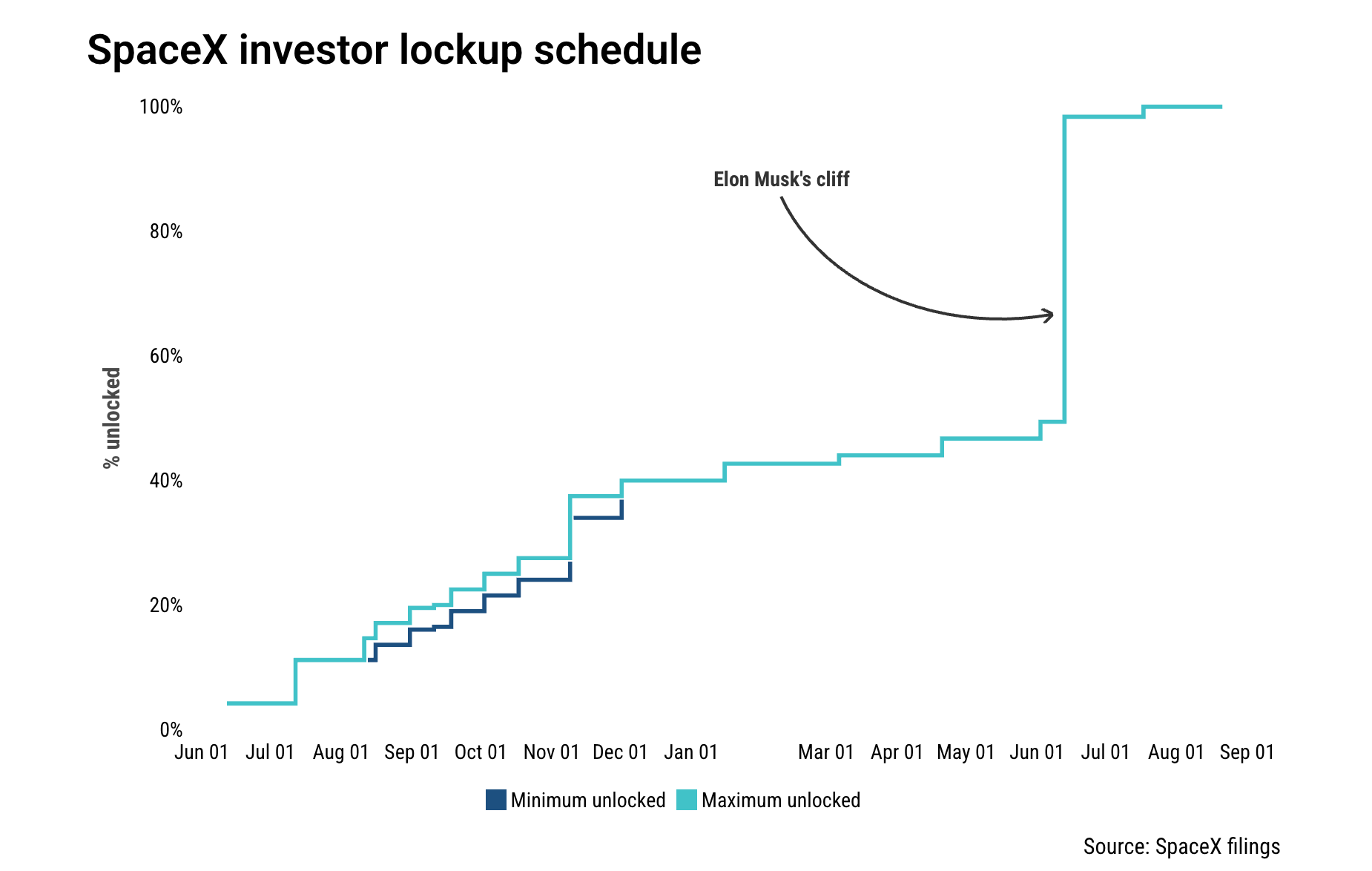

Few companies have ever demonstrated that better than SpaceX.

After spending 24 years as a private company, SpaceX has finally gone public, giving investors, employees and founders their first meaningful path to liquidity. The IPO valued the company at roughly $2.1 trillion, making it one of the world’s most valuable businesses.

The scale of the wealth creation is extraordinary.

SpaceX raised $30.8 billion across 61 financing rounds from more than 420 investors over its lifetime.

The company grew into a 22,000-person business before reaching the public markets.

Elon Musk’s stake is now worth roughly $1.03 trillion, while he continues to control 84.4% of the company’s post-IPO voting power.

But Musk isn’t the only winner.

Some of venture capital’s biggest firms are sitting on returns that could define entire decades of performance.

Valour Equity Partners, one of SpaceX’s earliest believers, now holds a stake worth approximately $81 billion after investing just a few hundred million dollars over the years—representing well over a 100x paper return.

Other major winners include:

Founders Fund, whose SpaceX stake is worth more than $50 billion.

Sequoia Capital has holdings exceeding $20 billion.

Andreessen Horowitz, which still owns roughly $10 billion worth of shares.

Luke Nosek, co-founder of Gigafund and one of SpaceX’s earliest institutional backers, whose personal stake alone is worth more than $5 billion.

The IPO also creates liquidity for thousands of employees who spent years building the company with stock compensation. Many of those newly wealthy operators are expected to become angel investors, founders or startup backers, injecting fresh capital into the next generation of aerospace, defence, and industrial technology companies.

But there is one important catch.

Almost none of these shareholders can sell immediately.

Like most IPOs, SpaceX has imposed lock-up restrictions that stagger when investors can exit. Most shareholders will only be able to gradually sell portions of their holdings over the coming year, while Elon Musk cannot sell any shares for 366 days after the IPO.

That means the paper wealth exists today, but the actual liquidity will arrive slowly.

For the venture industry, though, this is still a landmark moment.

After years of frozen IPO markets and delayed exits, one of venture capital’s greatest investments is finally beginning to return capital—providing long-awaited liquidity for funds, LPs and employees across the ecosystem.

FEATURED POSTS

📄 Must Read Post

How to Build Your Personal and Business AI Agents With Claude (No Coding Required).

👋 Hey, Sahil here - welcome to this edition of Venture Curator, where we break down how great startups grow, how top investors think, and what’s shaping the future of tech.

Below this price, AI products churn 3x worse. Most founders price below it.

👋 Hey, Sahil here - welcome to this edition of Venture Curator, where we break down how great startups grow, how top investors think, and what’s shaping the future of tech.

SOMETHING MORE

🧩 Frameworks & insightful posts

The framework for knowing whether customers will buy your SaaS in the AI era.

One question keeps coming up whenever people talk about building SaaS today.

“If AI can generate software in hours, why would anyone continue paying for it every month?”

It’s a fair question.

Every week, there are new stories of teams replacing expensive software with internal tools built using Claude or ChatGPT. Something that once required months of engineering can now be prototyped over a weekend, making many founders wonder whether traditional SaaS businesses are becoming harder to defend.

Recently, software engineer Brandur Leach shared one of the most thoughtful takes. Instead of asking whether AI will kill software companies, he asks a more useful question:

At what point does software become valuable enough that buying it still makes more sense than building it?

His answer revolves around something he calls the Minimum Viable Unit of Saleable Software.

AI has made software cheaper - but not free

It’s easy to assume that if AI writes code, companies should simply build every internal tool themselves.

In reality, that’s rarely how software gets built. Even with AI, someone still has to:

Review the generated code.

Test edge cases.

Fix bugs.

Maintain the product over time.

Keep improving it as business needs evolve.

AI dramatically reduces development time, but it doesn’t eliminate the ongoing cost of ownership.

That’s an important distinction.

A simple example explains the economics

A company was paying $400 per month for Jira and decided to replace it with an internally built version using Claude.

At first glance, the decision sounds obvious. Why keep paying every month when AI can build something similar?

But once you factor in engineering time, the picture changes.

Assuming an engineer earns around $200,000 per year, every hour spent maintaining that internal tool has a real cost. Even if AI handles most of the coding, someone still owns the product.

According to the rough math:

A $400/month subscription only justifies about 4 hours of engineering time per month.

After accounting for initial development and ongoing maintenance, it would still take roughly three years before rebuilding Jira actually breaks even.

For many companies, continuing to pay the subscription is simply the cheaper decision.

The equation changes as software becomes more expensive

Now compare that with something like Salesforce.

A larger company paying around $25,000 per month for CRM licenses is effectively spending the equivalent of more than one full-time engineer every month.

At that price point, building an internal alternative starts looking much more reasonable.

The interesting idea isn’t that companies should always buy or always build.

It’s that every product sits somewhere on a spectrum.

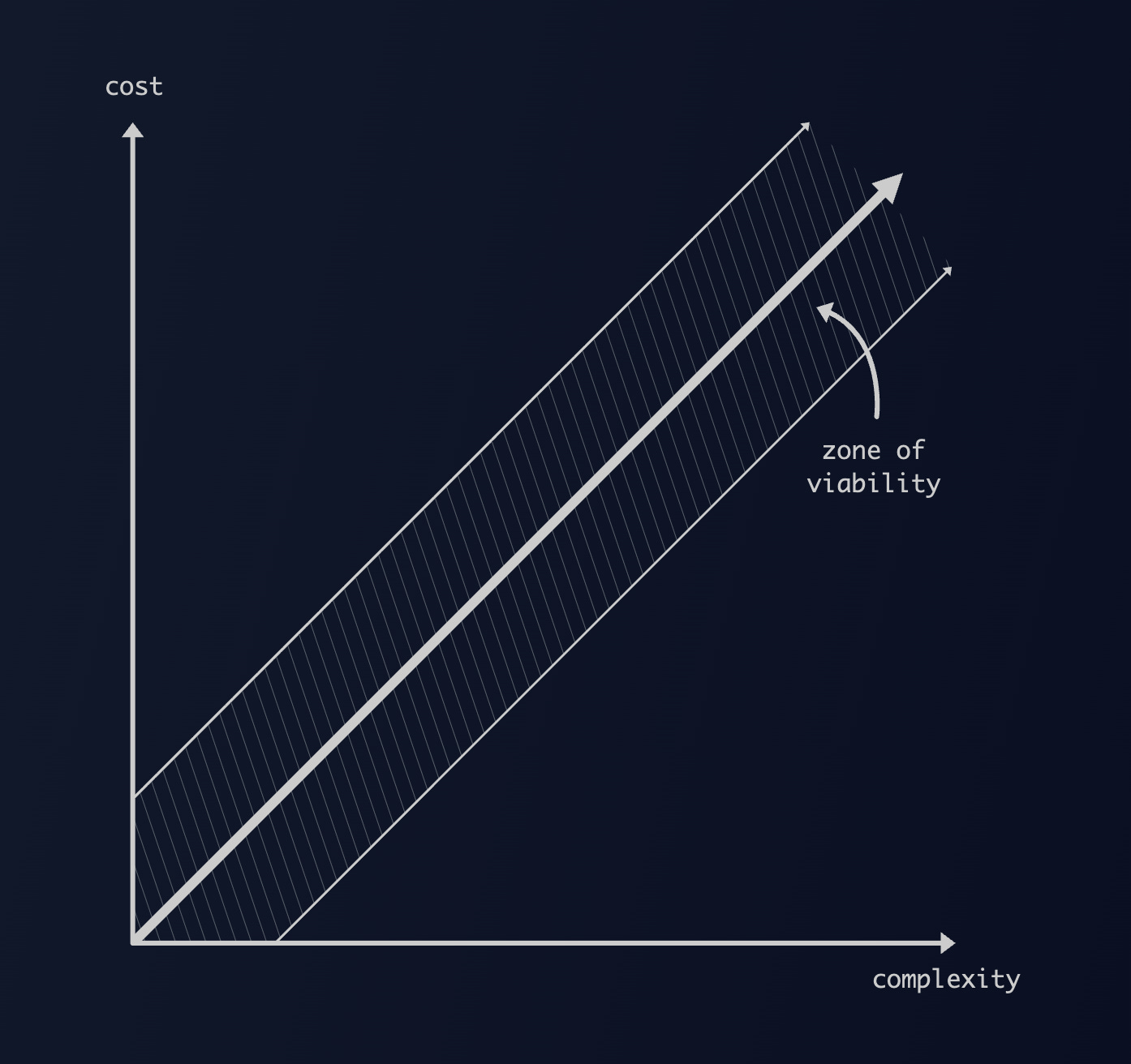

The “zone of viability”

One of the strongest ideas from the article is the concept of a zone of viability.

Software remains valuable when two conditions are true:

It solves problems that aren’t trivial for AI to recreate.

Its pricing stays reasonable enough that customers don’t feel compelled to build their own version.

Move outside that zone in either direction, and the economics change.

If the product is too simple, AI makes rebuilding it relatively easy.

If it’s priced too aggressively, companies become increasingly willing to invest engineering time instead of paying recurring subscription fees.

The winners are likely to be products that stay comfortably between those two extremes.

The new question every SaaS founder should ask

For years, founders mostly worried about whether customers wanted their product.

AI introduces a second question.

Is my product valuable enough that customers will continue buying it instead of building it themselves?

That doesn’t just depend on features.

It depends on how much expertise, maintenance, reliability, and continuous improvement your product provides customers without them having to own.

So, AI hasn’t eliminated the need for software businesses - it has simply raised the bar.

The companies that survive won’t necessarily have the most features. They’ll be the ones whose products remain more expensive to recreate than they are to buy. That may become one of the defining competitive advantages of SaaS in the AI era.

Framework: The 3-Layer AI sales stack every founder should build.

Almost every sales team has embraced AI.

Teams are using AI SDRs, email generators, account research tools, intent signals, call summaries, and automated prospecting. On paper, this should translate into more pipeline, higher conversion rates, and significantly more productive sales reps.

Yet for many companies, the results have been surprisingly average.

Reps still spend hours researching accounts. Prioritisation often feels like guesswork. And despite all the automation, buyers continue receiving cold emails that sound exactly like every other AI-generated message in their inbox.

So, where is AI actually falling short?

Recently, GTM leader Cam Wright shared one of the most practical explanations I’ve read. His argument isn’t that today’s AI models aren’t capable.

It’s that most companies are asking AI to make sales decisions without giving it the two things every great salesperson relies on: context and judgment.

Instead of improving decision-making, many companies are simply automating execution.

The biggest opportunity isn’t writing better emails

Most AI sales tools focus on the last step of the process. They help teams:

Write outbound emails

Generate call scripts

Summarize accounts

Draft LinkedIn messages

Automate repetitive tasks

Those are useful features, but according to Wright, they’re not where the real competitive advantage comes from.

The biggest gains happen much earlier. Before any email is written, someone has to answer questions like:

Which account deserves our attention?

Why is this company likely buying right now?

Which person inside the organisation actually feels the pain?

What business problem should we lead with?

If those decisions are wrong, even the best AI-written email won’t produce results.

Targeting and positioning matter far more than perfect copywriting.

AI knows signals. It doesn’t automatically understand what they mean.

Imagine two companies that both announce they’re hiring SDRs. Most AI tools see the same buying signal and recommend reaching out to both.

An experienced salesperson doesn’t. One company may:

Already use your biggest competitor.

Have recently signed a long-term contract.

Lack the integrations your product depends on.

The other might:

Be actively expanding its sales team.

Have recently hired someone who previously used your product.

Already use tools that fit naturally into your ecosystem.

Show multiple buying signals across CRM activity, website visits, and hiring trends.

On the surface, both companies look identical. In reality, one is a high-priority opportunity while the other is almost impossible to win.

The difference isn’t better AI.

It’s a better context.

Your competitive advantage isn’t the data - it’s how you interpret it.

Today, almost every GTM team can buy the same data. Everyone has access to:

Job posting data

Intent signals

CRM enrichment

Website visitor tracking

Contact databases

AI-generated messaging

Those inputs are becoming commodities.

The real edge comes from how your company combines and interprets those signals.

For example, a hiring announcement alone shouldn’t trigger outreach.

But combine that with recent website activity, a closed-lost opportunity from last year, a new RevOps hire, and a technology stack you integrate with—and suddenly the account tells a completely different story.

That’s not something an off-the-shelf AI model understands automatically.

That’s the knowledge your business has built over years of selling.

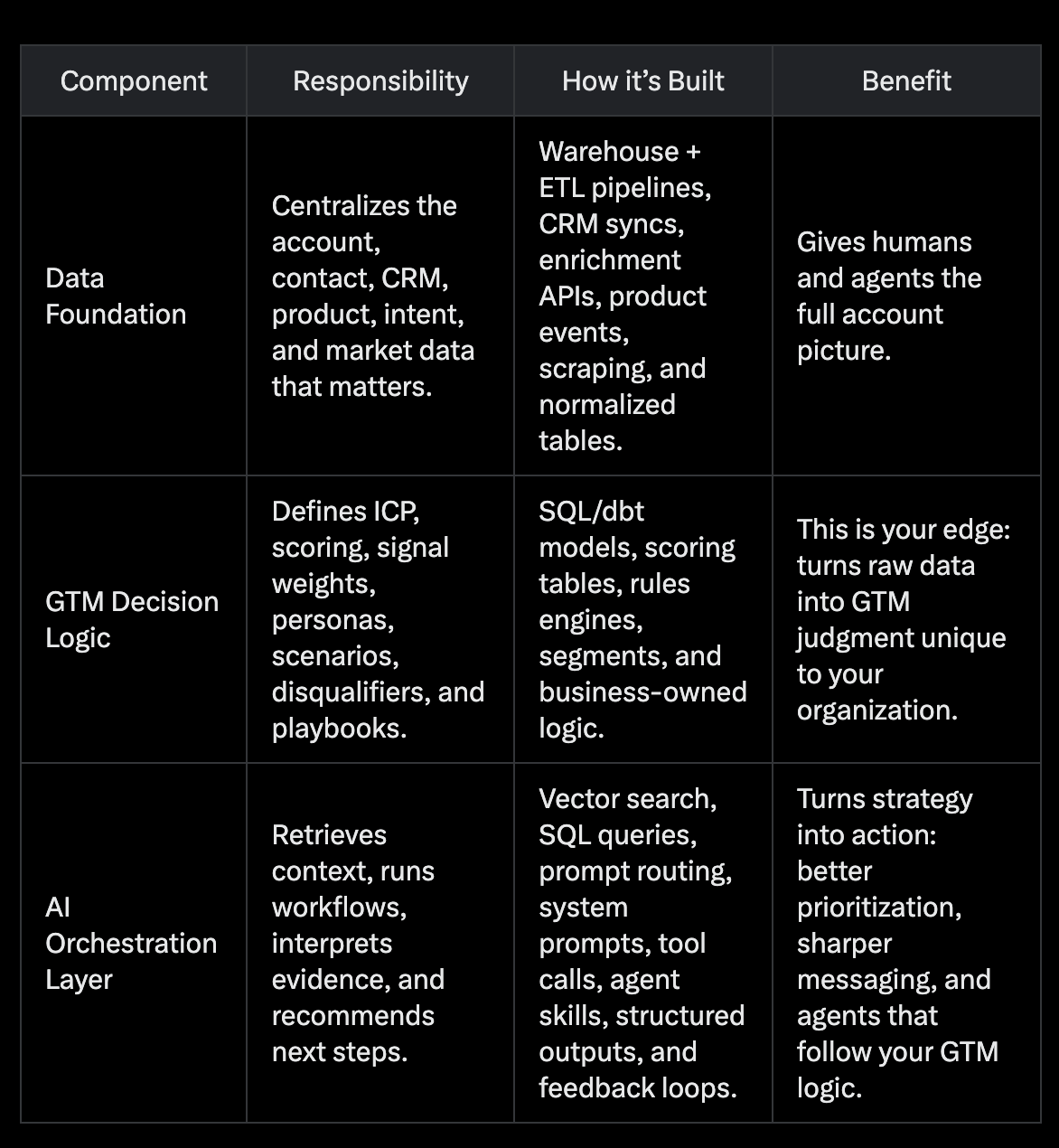

The companies seeing the biggest AI gains build three layers before they automate

The strongest GTM organisations don’t simply plug AI into their workflow. They first build the foundation AI needs to make better decisions.

Build a data foundation

Bring together everything your company already knows - CRM history, product usage, opportunity data, customer conversations, website activity, enrichment, job postings, and market signals, so both humans and AI work from the same source of truth.

Own your GTM decision logic

This is where your competitive advantage lives.

Define your ideal customer profile, account scoring, buying signals, personas, playbooks, disqualifiers, and prioritisation rules internally rather than outsourcing that thinking to an AI vendor.

Let AI orchestrate execution

Once the first two layers are in place, AI becomes dramatically more useful.

Instead of guessing who to contact, it retrieves the right context, applies your playbooks, recommends next steps, and generates messaging based on your company’s own decision-making framework.

The result is AI that follows your strategy instead of inventing one.

So, access to powerful AI models is no longer an advantage. Almost every company has access to similar models, similar data providers, and similar automation tools.

The real differentiation is moving upstream - building better judgment about which accounts matter, why they matter, and what your business uniquely understands about them. AI can execute that strategy incredibly well, but it still needs humans to define it first.

📬 Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Haun Ventures, a Menlo Park, CA-based venture capital firm, closed Fund II at over $1 billion. (Link)

Valour Equity Partners, the Chicago-based growth investment firm founded by Antonio Gracias, is looking to raise at least $2.5 billion for its new Fund VII. (Link)

Menlo Ventures, a Silicon Valley venture firm known for backing AI startups, has raised $3 billion across new funds, its largest fundraise in 50 years. (Link)

Los Angeles, CA-based Mantis VC is raising a fourth fund targeting $100m. (Link)

New Startup Deals

Valence AI, a San Francisco, CA-based emotional intelligence infrastructure company, raised an undisclosed Seed round, bringing total funding to $5M. (Link)

Seltz, a San Francisco, CA-based provider of a web retrieval infrastructure layer for LLMs and AI agents, raised $12.5M in Seed funding. (Link)

Timefold, a Ghent-based vehicle routing and shift scheduling platform, raised $13M in Series A funding. (Link)

Prosper AI, a New York-based AI platform for patient journey management, raised $30M in Series A funding. (Link)

Nura Bio, a South San Francisco-based neuroprotective therapeutics company, raised $73.8M in Series B funding. (Link)

Cargofy, a Chicago-based AI-powered freight operations platform, raised $11M in Series A funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: In partnership with a leading investor group, we have created an all-in-one guide for aspiring VCs. Don’t miss this. (Access Here)

Venture Investment Manager - AMD | USA - Apply Here

Partner 16, Partner 18 - a16z | USA - Apply Here

Portfolio Reporting Team Lead - Cerity Partner | USA - Apply Here

VC Investment Intern - First Momentum Venture | USA - Apply Here

Investment Associate - Antler | UK - Apply Here

Growth Intern (Merantix AI Campus) - Germany - Apply Here

VP — Finance & Compliance - Transition VC | India - Apply Here

Senior Associate - ICONIQUE CAPITAL | USA - Apply Here

Investment Associate / Analyst - Flashpoint | UK - Apply Here

Venture Capital Analyst - MicroVentures | USA - Apply Here

Hard Tech Investment Associate - Upfront Venture | USA - Apply Here

Associate - Engine Venture | USA - Apply Here

Senior Venture Studio Analyst - Atlantic Health System | USA - Apply Here

Talent Investor - Associate - Entrepreneur First | India - Apply Here

Partnership With Us

Get your product in front of over 125,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

(Subscribe to Venture Curator Premium and get 20% off forever.)

this is the stat that should scare the megafunds, not the seed managers haha