Why are Investors betting billions on a technology despite an adoption problem?| How Anthropic builds its sales organisation?

Nearly half of America’s unicorn founders were born outside the US & VC Jobs

👋 Hey, Sahil here - Welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

Has Venture Capital quietly become a bigger-fund game?

What 500 unicorns reveal about where great founders come from?

Frameworks & insightful posts :

Why are Investors betting billions on Brain-computer interfaces despite an adoption problem?

Why the next billion-dollar sales companies won’t own the database.

How Anthropic builds its sales organisation?

FROM OUR PARTNER - STRATIFIND

🧬 Investors are backing STRATIFIND, a precision oncology company focused on helping oncologists make better cancer treatment decisions.

Despite major advances in cancer genomics, treatment selection often remains a trial-and-error process. Physicians receive large genomic reports filled with complex DNA and RNA data, but those reports do not always clearly indicate which therapy is most likely to benefit the patient first.

STRATIFIND is developing RainDanceEQ™, an AI-assisted precision oncology platform designed to translate complex tumour biology into clinically actionable treatment insights. Its platform integrates DNA and RNA data to generate structured reports that help oncologists evaluate and prioritise therapeutic options.

Why investors are paying attention:

Targeting an initial $1.0B market opportunity with a potential path toward a broader $2.1B U.S. precision oncology market

Built on algorithms trained using 20,000+ tumour samples and supported by more than 15 years of foundational research

Asset-light business model focused on the high-value clinical interpretation and decision-support layer

Led by a multidisciplinary team spanning oncology, diagnostics, pathology, radiation oncology, and healthcare finance

Positioned at the intersection of AI, multiomics, and precision medicine

As precision medicine becomes increasingly integrated into routine cancer care, oncologists face growing complexity in treatment selection.

STRATIFIND aims to provide clearer, more clinically relevant insights to help guide therapy decisions and improve patient outcomes.

Invest in STRATIFIND crowdfunding campaign here →

START WITH

🧠 Big idea + report of the week

Has Venture Capital quietly become a bigger-fund game?

For years, emerging managers could build successful venture firms with relatively modest fund sizes.

A $20M-$50M fund could write meaningful seed checks, reserve capital for follow-ons, and still maintain ownership in the best companies.

That math is becoming much harder.

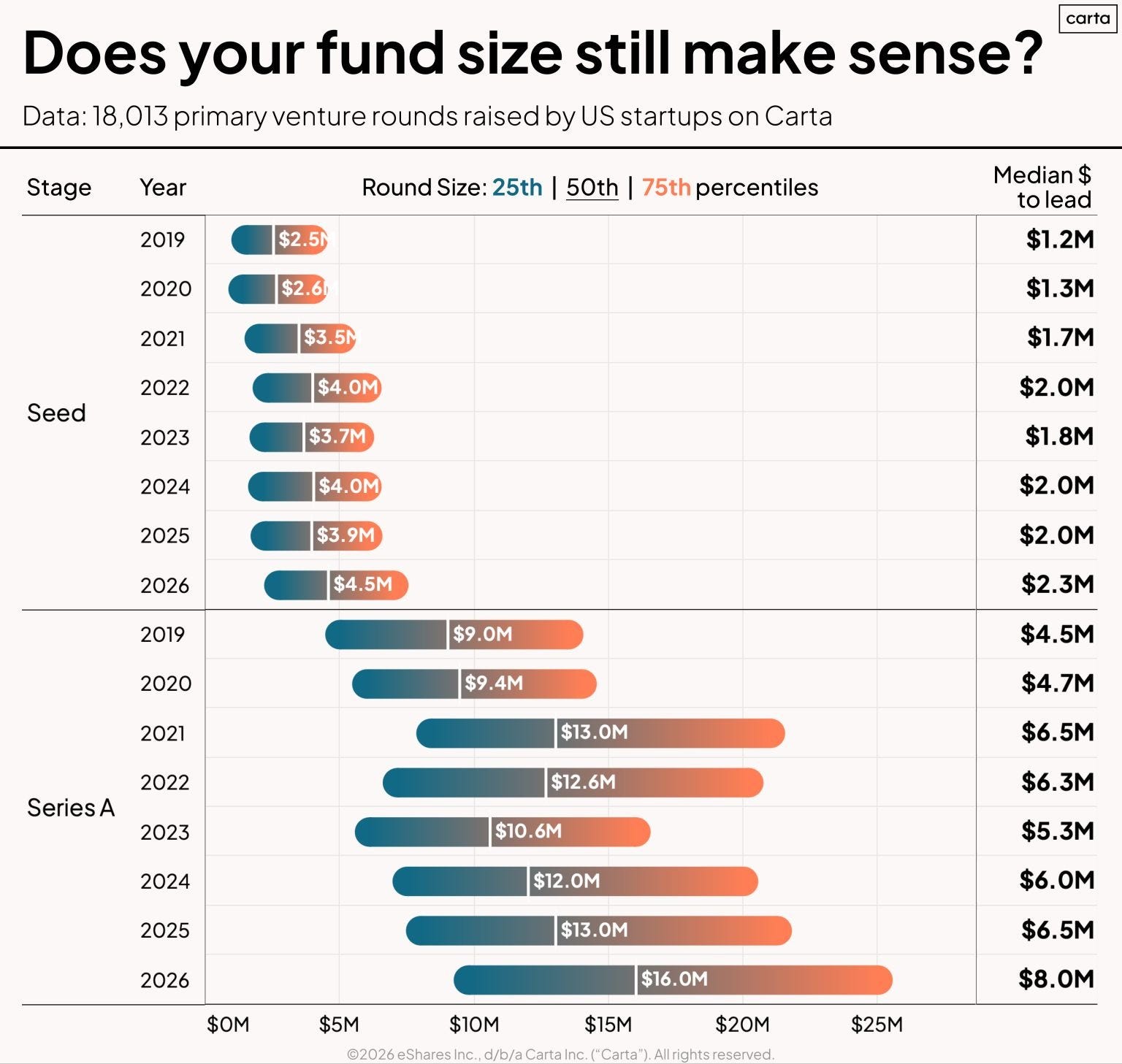

Peter Walker, Head of Insights at Carta, recently shared data from more than 18,000 venture rounds that highlights a structural shift happening across the venture ecosystem: startup round sizes are getting bigger, lead checks are getting bigger, and the amount of capital required to execute the same strategy is rising almost everywhere.

The question many managers now face is simple: Does your fund size still match the market you’re investing in?

Startup round sizes have expanded significantly

The numbers are striking. In 2019, the median seed round was roughly $2.5M. By 2026, it had reached $4.5M.

Series A rounds have grown even faster. The median Series A was approximately $9M in 2019. Today, it sits at $16M.

This isn’t simply a story about higher valuations.

It means investors who want to maintain the same ownership percentages they achieved five or six years ago must deploy substantially more capital into each company.

And that creates pressure throughout the entire fund model.

Leading rounds are becoming more expensive

One consequence of larger rounds is that lead investors need much larger checks.

According to Carta’s data:

Median seed lead checks increased from $1.2M to $2.3M.

Median Series A lead checks increased from $4.5M to $8M.

For managers who position themselves as lead investors, this dramatically changes fund construction.

A fund that could comfortably lead multiple rounds a few years ago may suddenly find itself stretched thin if it wants to maintain the same pace of investing.

The result is that many firms either need larger funds or need to accept smaller ownership positions.

Follow-on investing has become harder, too

The challenge doesn’t stop after the first check.

Many venture firms want to double down on their best-performing companies as those businesses raise larger rounds at higher valuations.

But when startups are raising more capital every round, reserve requirements grow alongside them.

Maintaining ownership in winners requires increasingly large follow-on checks, particularly in today’s AI-driven market, where companies often scale valuations rapidly between financings.

What used to be a manageable reserve strategy can quickly become a capital allocation problem.

Bridging portfolio companies creates another layer of pressure

The third challenge involves bridge rounds. When portfolio companies need additional capital between financings, managers face difficult choices.

Every bridge check competes directly with: New investments, Follow-on investments and Future reserves.

As round sizes increase, supporting existing portfolio companies becomes more expensive, forcing firms to make harder tradeoffs than they did during previous venture cycles.

Why are many managers being pushed toward larger funds

Taken together, all three forces point in the same direction.

Larger rounds require larger lead checks. Larger lead checks require larger reserves. Larger reserves require larger funds.

That is one reason many venture firms have steadily increased fund sizes over the past several years.

The logic is understandable. If the market itself requires more capital to execute the same strategy, managers naturally feel pressure to raise more money.

The hidden risk behind bigger funds

Just because the market encourages larger funds does not mean larger funds are always the right answer.

A fund size should reflect:

A manager’s sourcing advantage

Their ownership targets

Their stage focus

Their ability to deploy capital effectively

When a firm raises significantly more capital than its strategy can support, performance can suffer.

The danger is that larger funds often feel rational in the short term because LPs generally welcome growth. But a mismatch between fund size and actual investment strategy can create problems that take years to become visible.

So many venture firms are still operating with assumptions built for the market of 2019.

The market of 2026 looks very different.

Round sizes are larger. Ownership is more expensive. Follow-ons require more capital. Bridging companies cost more. Everything points toward deploying larger amounts of money.

But the lesson isn’t simply “raise a bigger fund.”

The real lesson is that every manager should periodically revisit the assumptions behind their fund model.

Because in today’s venture market, the most dangerous strategy may be running yesterday’s playbook with tomorrow’s capital requirements.

What 500 unicorns reveal about where great founders come from?

The narrative around American innovation is often framed as a domestic success story. But the data tells a different story.

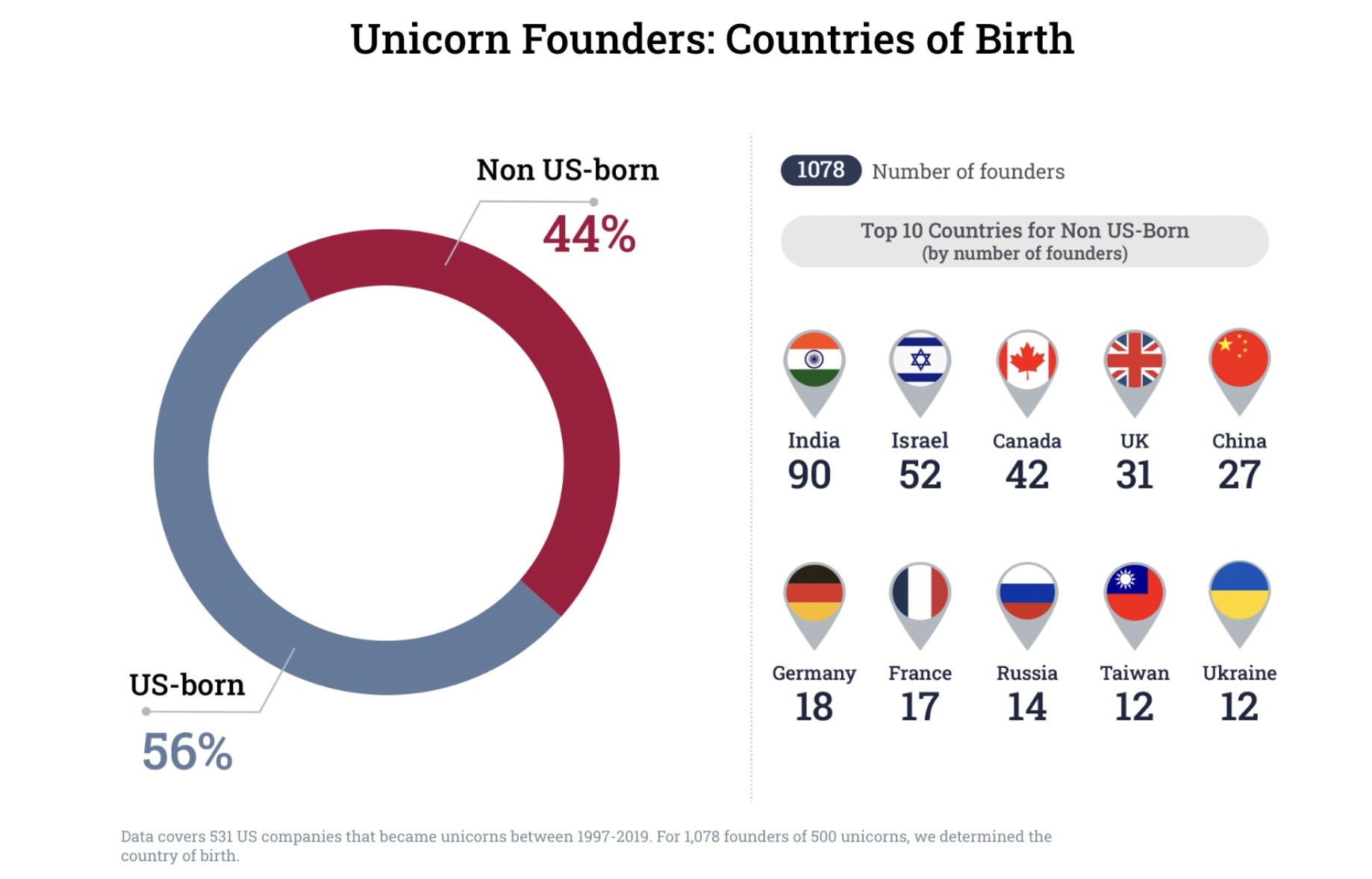

Research from Stanford professor Ilya Strebulaev, covering 500 US unicorns and 1,078 founders, found that 44% of all US unicorn founders were born outside the United States.

Nearly half of America’s most valuable startups were built by entrepreneurs who started their journey somewhere else.

The implication is hard to ignore: immigrant talent isn’t just participating in the US startup ecosystem - it is one of its core growth engines.

India leads the global unicorn founder pipeline

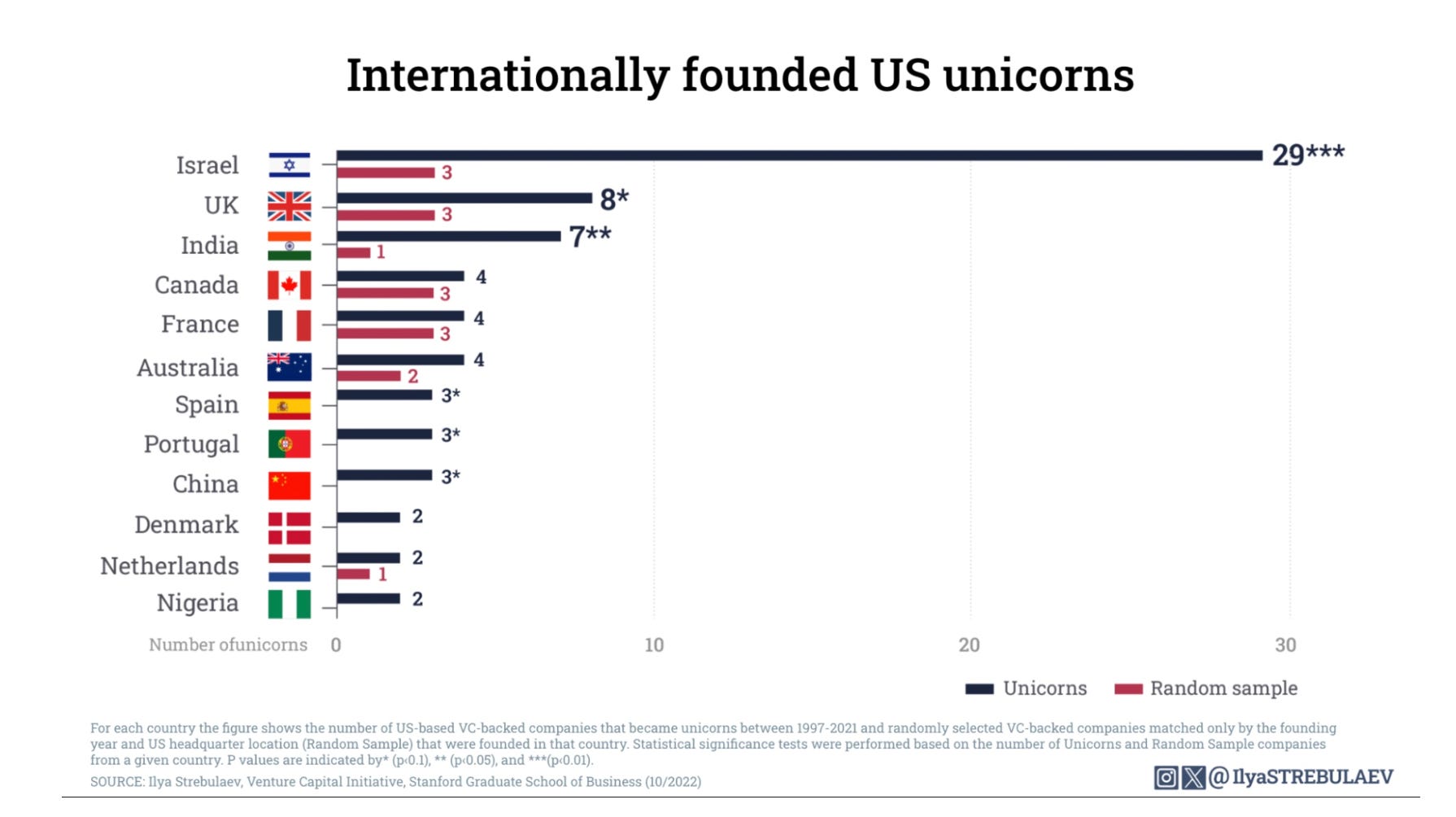

Among foreign-born founders, India ranks first by a wide margin.

The study identified 90 Indian-born founders behind US unicorn companies, making India the largest source of immigrant unicorn entrepreneurs in America.

Israel ranked second with 52 founders, followed by Canada (42), the United Kingdom (31), and China (27).

What’s notable is the breadth of countries represented.

The dataset includes founders from 65 different countries across six continents, reinforcing that breakthrough entrepreneurship is increasingly global, even when the companies themselves are ultimately built in the US.

Moving to America dramatically increases the odds of success

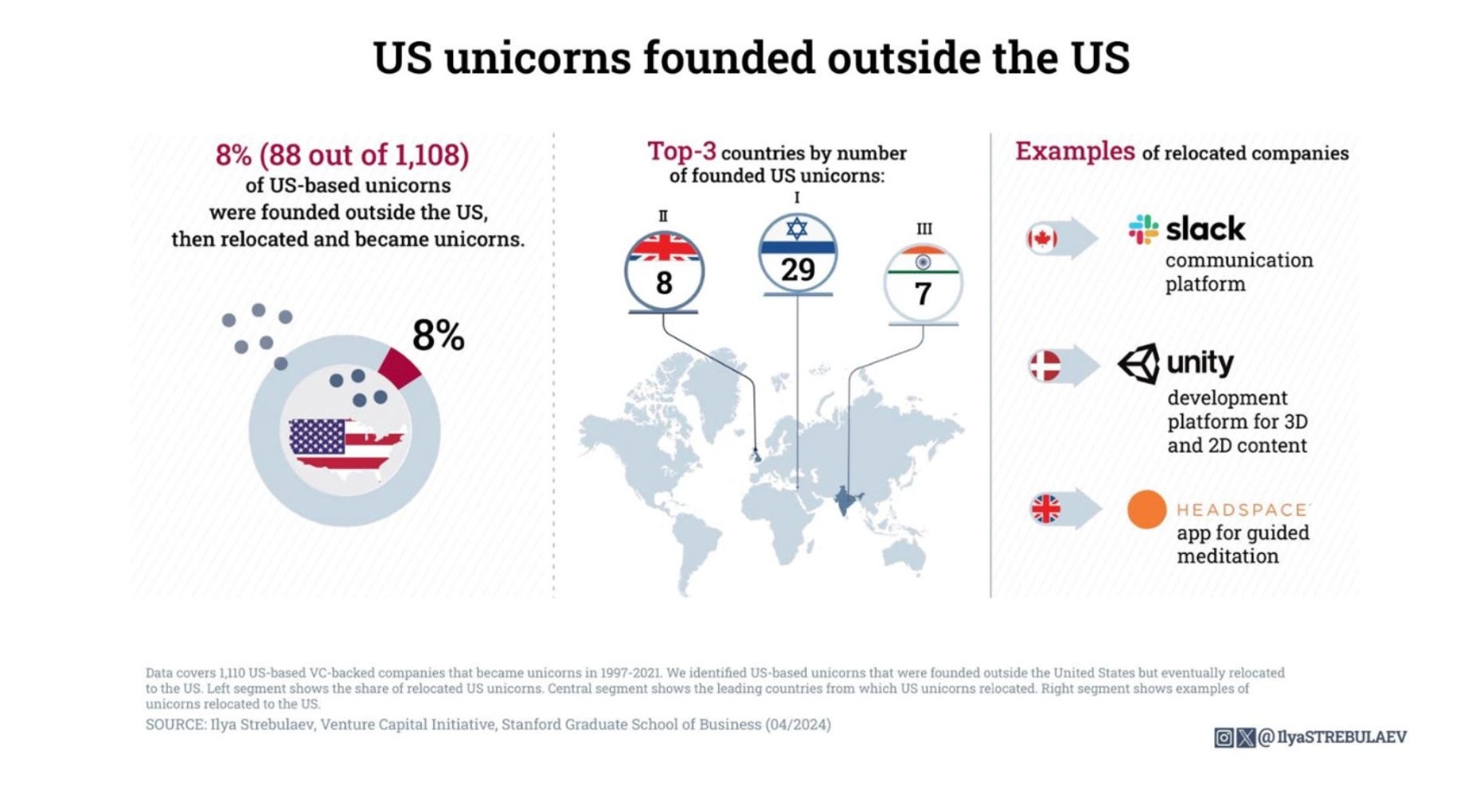

One of the most interesting findings isn’t about founders - it’s about companies.

Roughly 8% of US unicorns were originally founded outside the United States before relocating.

And the relocation effect appears significant.

According to the research:

Israeli startups that moved to the US were about 9x more likely to become unicorns.

Indian startups saw roughly a 6.5x increase in unicorn outcomes after relocating.

UK startups experienced approximately a 2.5x advantage.

The pattern suggests that while great companies can be started anywhere, the US continues to offer unique advantages in capital access, talent density, customer reach, and scaling infrastructure.

California remains the centre of gravity

When international founders relocate, most still gravitate toward California.

The state continues to function as the primary destination for ambitious startups looking to scale globally.

However, the research also highlights interesting regional patterns.

Israeli-founded unicorns, for example, often choose New York over California, while other founders increasingly spread across ecosystems such as Massachusetts and Texas.

In total, around 15% of US unicorns changed headquarters at least once between founding and achieving unicorn status.

Location remains a strategic decision, not simply a logistical one.

Israel produces the most unicorn founders per capita

While India leads in total founder count, Israel stands out on a per-capita basis.

When adjusted for immigrant population size, Israel generated approximately 43.4 unicorn founders per 100,000 first-generation immigrants, the highest rate among all countries studied.

For comparison:

New Zealand: 37.3 founders per 100,000 immigrants

Belgium: 24.4

Canada: 5.3

India: 2.5

America’s advantage is attracting global talent

America’s startup leadership isn’t solely a result of domestic talent or capital. It comes from being a magnet for ambitious people worldwide.

Nearly half of US unicorn founders were born elsewhere.

Some arrived as students. Some are engineers. Some founders are looking for a larger market.

What they found was an ecosystem capable of turning global talent into globally significant companies.

The lesson for policymakers, investors, and founders is straightforward: America’s startup dominance isn’t built only on what happens inside its borders. It’s built on its ability to attract exceptional people from outside.

Featured Posts

FROM OUR PARTNER - ROCKET

🔎 Stop Reacting to Competitors. Start Predicting Them.

Most competitive tools surface raw data and leave the interpretation to you. Rocket Intelligence monitors companies across 9 signal pillars, hiring, pricing, ads, tech stack, exec moves, reviews and tells you what it means for your role specifically.

A pricing page change plus a hiring surge in enterprise sales means something. Rocket connects the dots so you don't have to.

📬 Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

SOMETHING MORE

🧩 Frameworks & insightful posts

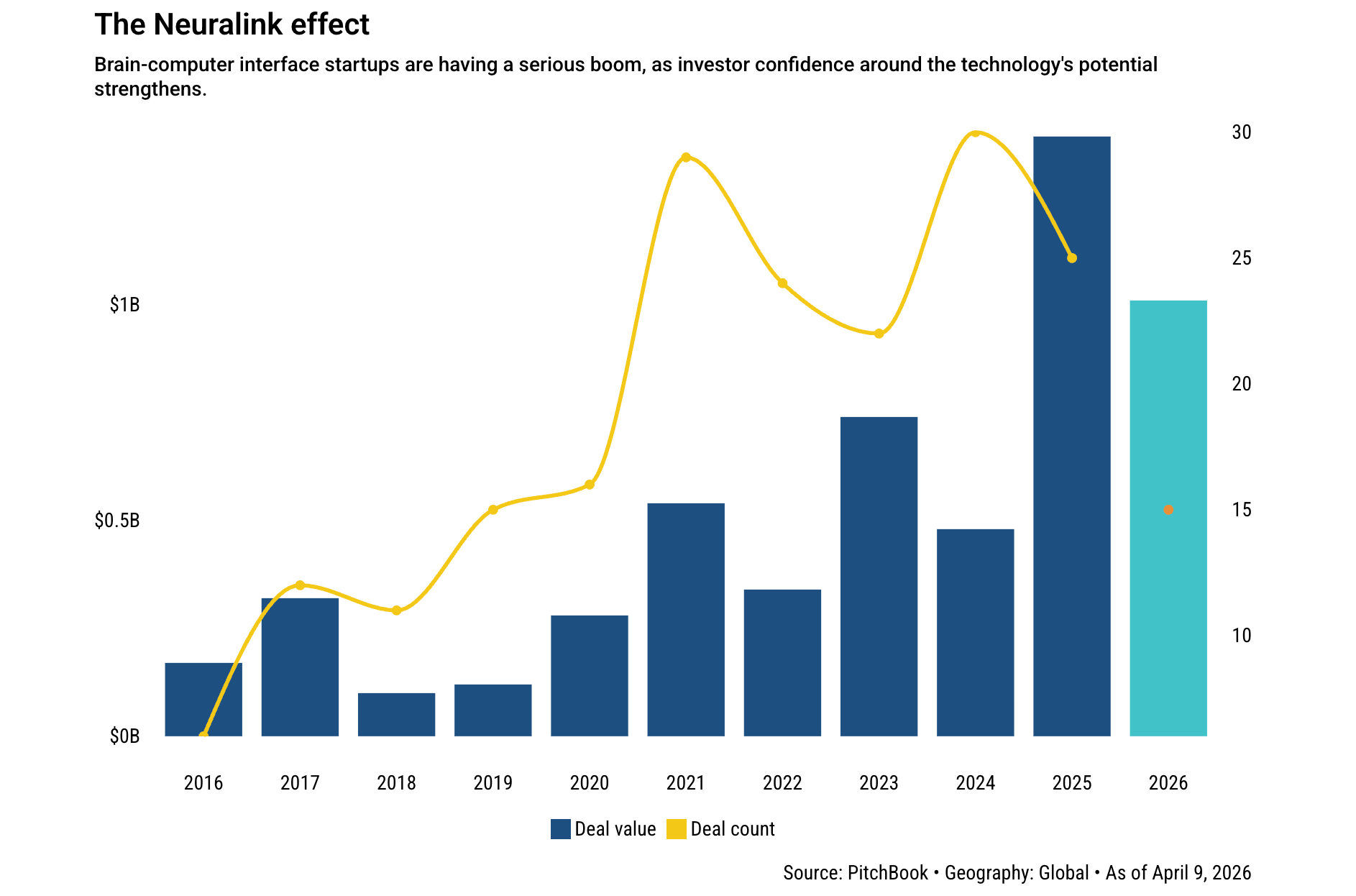

Why are Investors betting billions on Brain-computer interfaces despite an adoption problem?

Brain-computer interfaces may become one of the most important technologies of the next few decades.

The vision is enormous: restoring movement to paralysed patients, helping blind people see again, treating neurological diseases, and eventually giving humans new ways to interact with computers.

Investors are betting heavily on that future. More than $3 billion has flowed into brain-computer interface startups since 2024, with companies like Neuralink attracting billions in funding and reaching multi-billion-dollar valuations.

Rosie Bradbury from PitchBook recently explored one of the biggest unanswered questions in neurotechnology: even if brain-computer interfaces (BCIs) work, how many people will actually want them?

Investor enthusiasm is clearly accelerating. Since 2024, more than $3 billion has flowed into BCI startups, helped largely by the progress and visibility of Neuralink.

But behind the excitement sits a much tougher challenge: adoption.

Today, the technology remains highly invasive. Neuralink, for example, requires surgery to implant electrodes into the brain. Despite raising over $1.3 billion and achieving a valuation above $9 billion, the company reportedly had just 21 clinical trial participants worldwide as of early 2026.

That highlights a reality many investors acknowledge privately: building the technology may be easier than convincing millions of people to use it.

Researchers studying patient behaviour continue to find hesitation around brain implants. Even among people suffering from serious neurological conditions, many are reluctant to place foreign devices inside their brains unless symptoms become severe.

A useful example is deep brain stimulation, one of the most established forms of brain-computer interface technology. Despite proven medical benefits for certain Parkinson’s patients, only a small percentage of eligible patients undergo the procedure each year.

The hesitation is understandable.

Unlike wearing a smartwatch or carrying a smartphone, BCIs (Brain-Computer Interface) involve surgery, long-term safety considerations, and psychological questions about identity and autonomy. For many people, the brain feels fundamentally different from any other part of the body.

Still, the healthcare opportunity alone is enormous. Potential patient populations include:

More than 90 million stroke survivors globally

Over 11 million people live with Parkinson’s disease

20-25 million people with non-cataract blindness

Millions of people are suffering from paralysis and motor disabilities

For many of these patients, BCIs could restore lost capabilities rather than simply enhance existing ones. That’s why most investors underwriting the category today are focused on medical applications first.

The more ambitious vision comes later.

Some investors believe BCIs could eventually become consumer products used by healthy individuals to improve memory, cognition, productivity, or even keep pace with increasingly powerful AI systems.

The argument is that humanity may eventually augment itself in the same way smartphones augmented communication.

In that world, brain implants would evolve from medical devices into mainstream computing platforms. But there are several hurdles before that becomes reality:

The technology must prove safe over long periods.

Surgical procedures need to become simpler and less invasive.

Costs need to decline significantly.

Clear consumer benefits must emerge.

Regulatory approval pathways must mature.

Perhaps most importantly, people need a compelling reason to undergo surgery.

As one expert quoted in the article noted, technology adoption doesn’t happen simply because something is possible. The assumption that “if you build it, they will come” rarely works in healthcare.

That’s why even bullish investors are careful about timelines.

Most aren’t investing based on a future where healthy consumers rush to implant brain chips. They’re investing because they believe hospitals, rehabilitation centres, and patients with severe neurological conditions represent a realistic first market.

The broader lesson is one that founders often forget when evaluating frontier technologies: Technical breakthroughs don’t automatically create mass markets.

The history of technology is filled with products that worked but never achieved widespread adoption because user behaviour, trust, regulation, or economics lagged.

Neurotechnology may ultimately transform medicine, computing, and even human cognition. But the companies that win won’t just solve engineering challenges.

They’ll solve distribution, trust, safety, and user adoption as well.

And in many ways, those may be the harder problems.

Why the next billion-dollar sales companies won’t own the database.

For the last two decades, most of the value in sales software has accumulated around one simple idea: own the database.

Salesforce built a $140B company. HubSpot built a $9B company. Thousands of startups came and went, but the winners owned the system of record - the place where customer data, deal history, contacts, and company knowledge lived.

Recently, a16z shared an interesting perspective: AI isn’t replacing the CRM. It’s changing where work happens.

The shift feels similar to what happened in social media.

Years ago, Facebook’s most valuable asset was the friend graph. Then the News Feed became the primary experience. The graph still existed, but it became an input powering something more valuable.

The same thing may be happening to CRM systems.

Instead of spending their day inside Salesforce or HubSpot, sales teams are increasingly working through AI-powered intelligence layers that sit on top of those systems.

A sales rep’s day is starting to look very different:

AI researches accounts before meetings.

AI summarises earnings calls and company filings.

AI drafts outbound emails.

AI updates CRM records automatically after calls.

AI identifies which deals need attention.

AI surfaces risks before managers notice them.

The CRM remains the database, but the AI layer becomes the interface where decisions are made.

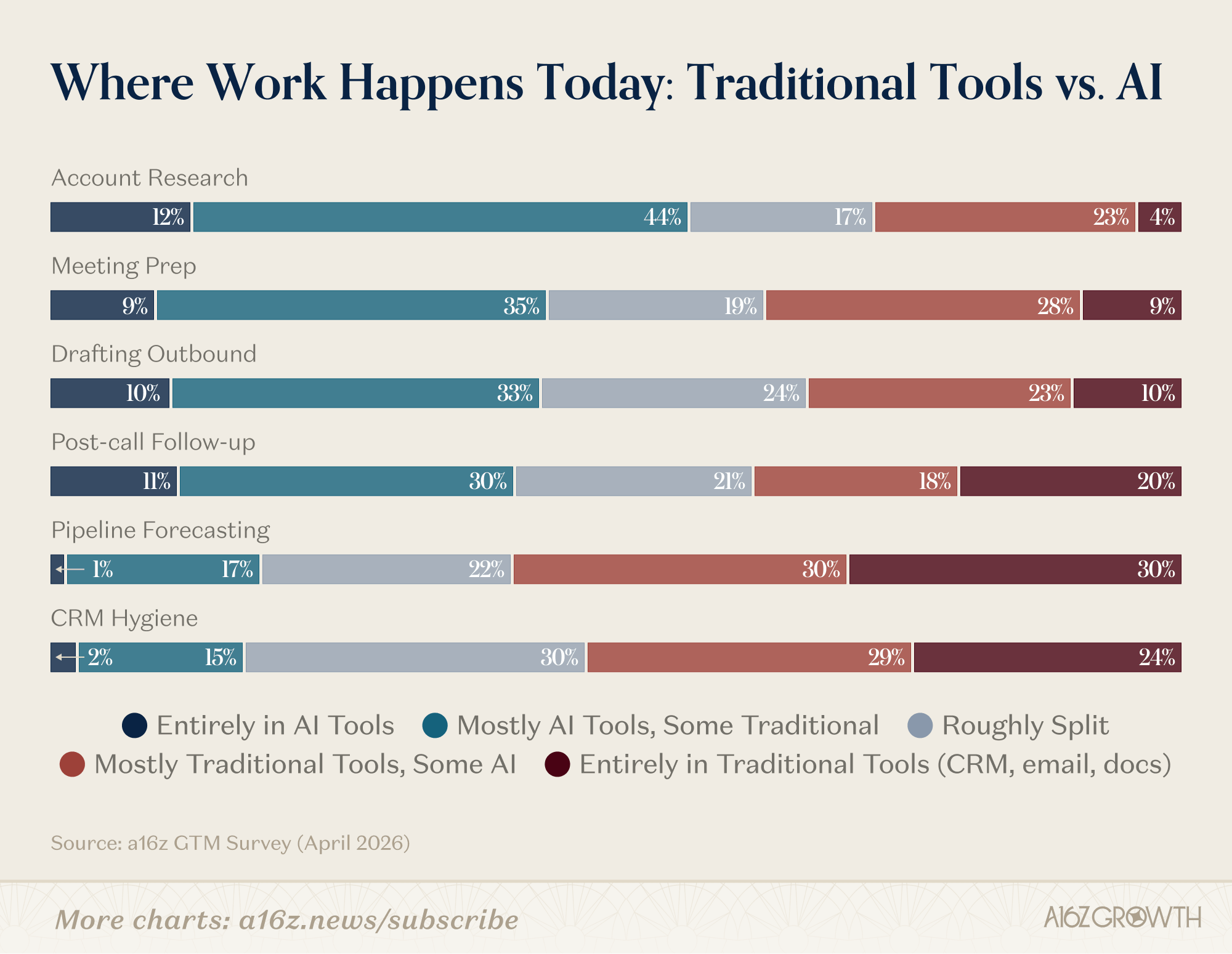

One chart from a16z’s GTM survey illustrates this clearly.

Today, account research, meeting preparation, outbound drafting, and follow-ups are already heavily shifting toward AI tools. Pipeline forecasting and CRM management still lean more heavily on traditional systems, but even those workflows are beginning to move.

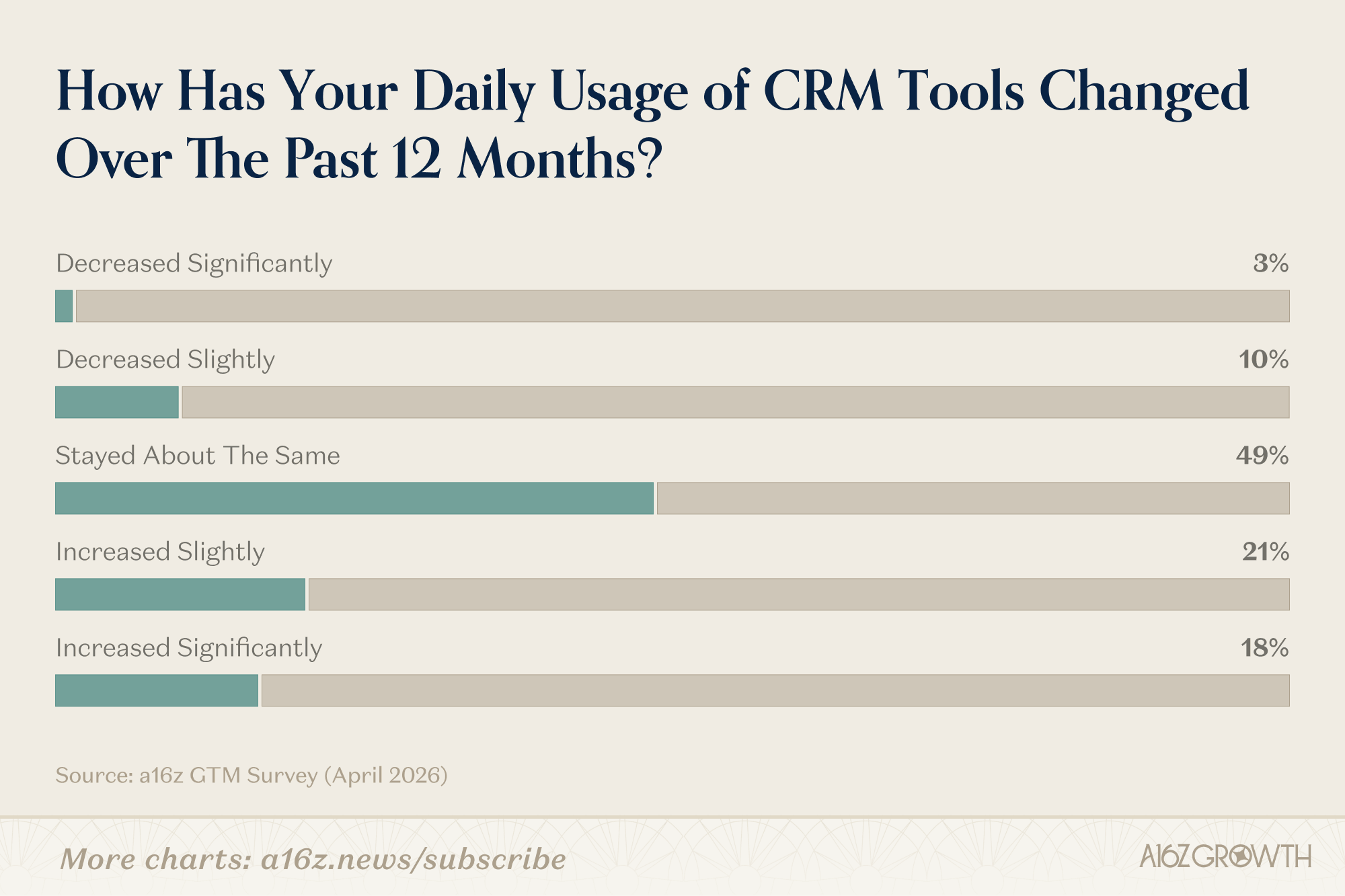

The interesting part is that CRM usage hasn’t collapsed. In fact, CRM usage has slightly increased.

Nearly half of respondents said their CRM usage stayed the same over the past year, while 49% reported using CRM tools more frequently.

Why?

Because AI agents are actually creating more data than humans ever did.

Every call transcript, meeting summary, email interaction, and account update now flows automatically into CRM systems. The database becomes richer, even if humans spend less time manually updating it.

That creates an important distinction:

The system of record remains valuable. The system of intelligence becomes even more valuable.

Historically, enterprise software created value by helping people store information.

The next generation of software may create value by helping people decide what to do with that information.

That’s why a growing number of AI-native GTM startups aren’t trying to replace Salesforce. They’re building orchestration layers above it.

These systems pull information from:

CRM platforms

Email

Calendars

Call recordings

Product analytics

Slack

Internal documents

Then combine everything into recommendations, actions, and workflows.

In other words, the AI layer becomes the operating system for revenue teams.

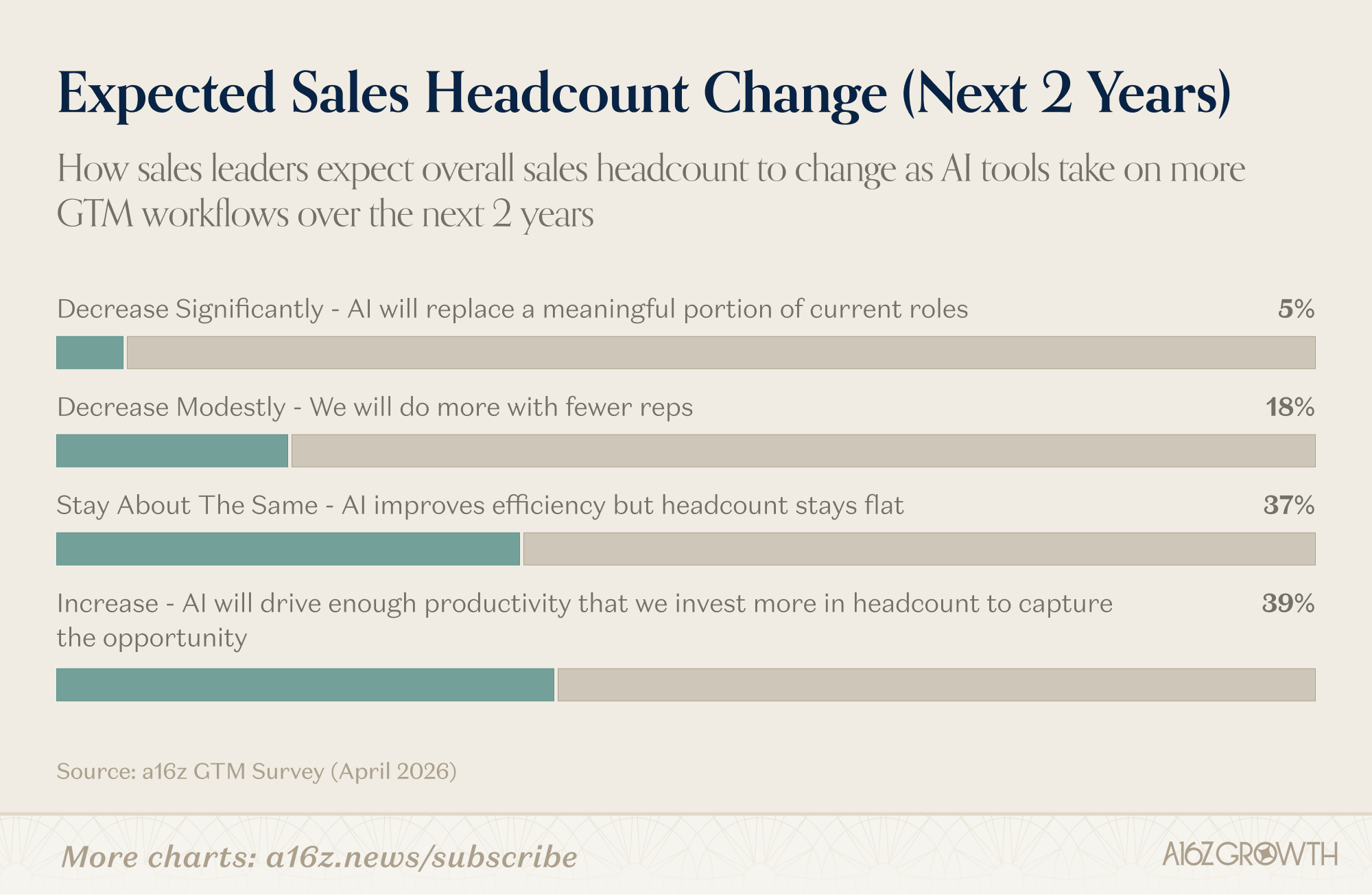

Another surprising takeaway from the survey challenges a common narrative around AI replacing sales jobs.

When asked how sales headcount will change over the next two years:

39% expect headcount to increase.

37% expect it to stay roughly the same.

Only 23% expect reductions.

The reason is simple. If AI helps sales teams become more productive, many companies would rather grow faster than simply cut staff.

This mirrors what happened throughout software history. Better tools often expand markets before they shrink jobs.

So, AI isn’t always destroying existing categories. Sometimes it’s reorganising them.

Salesforce and HubSpot still own some of the most valuable datasets in enterprise software. That advantage isn’t disappearing anytime soon.

But the next generation of billion-dollar companies may not own the database. They may own the intelligence layer sitting on top of it.

And just as the News Feed became more important than the friend graph, the system that tells you what to do next may become more valuable than the system storing the data itself.

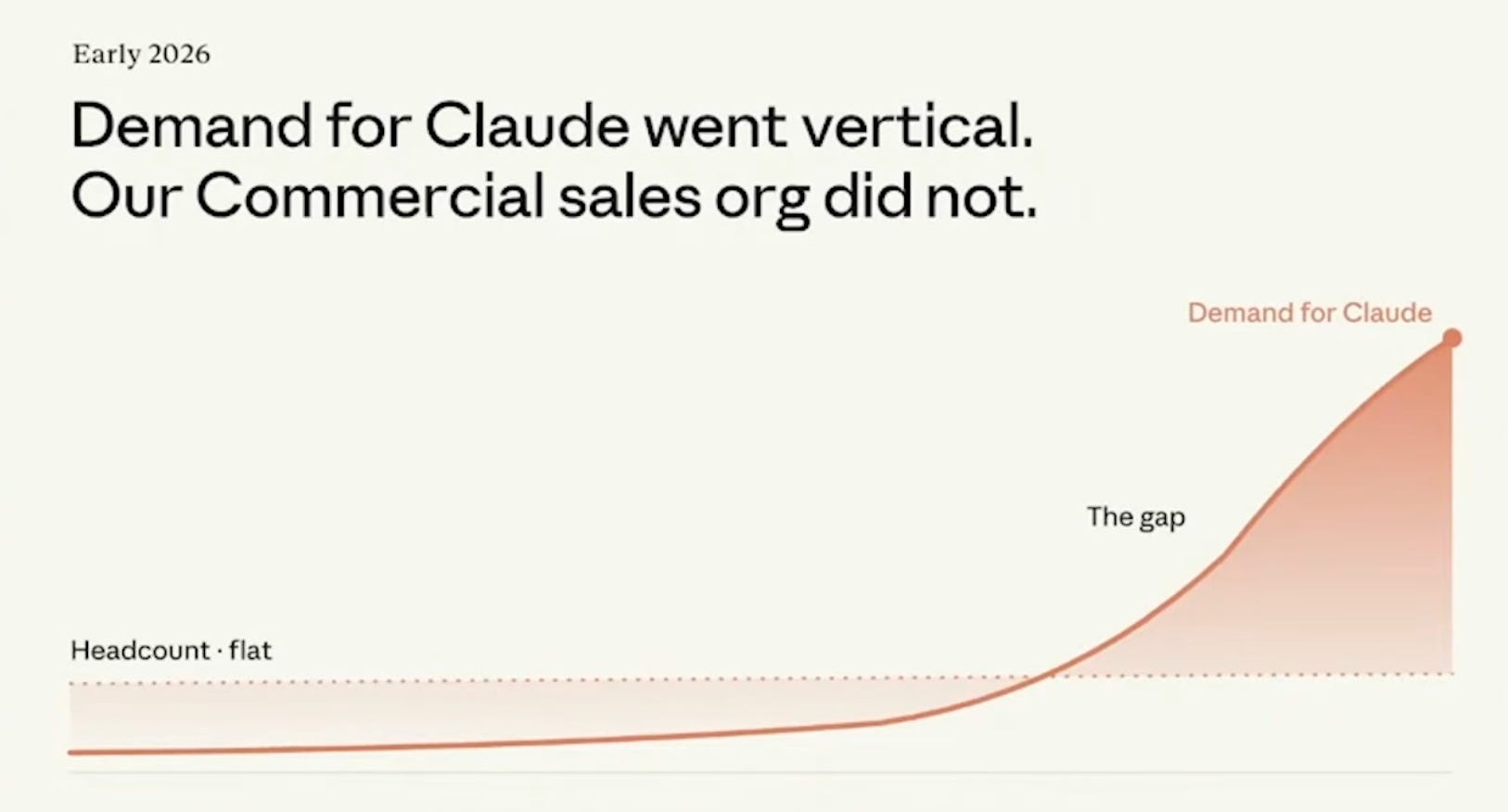

How Anthropic builds its sales organisation?

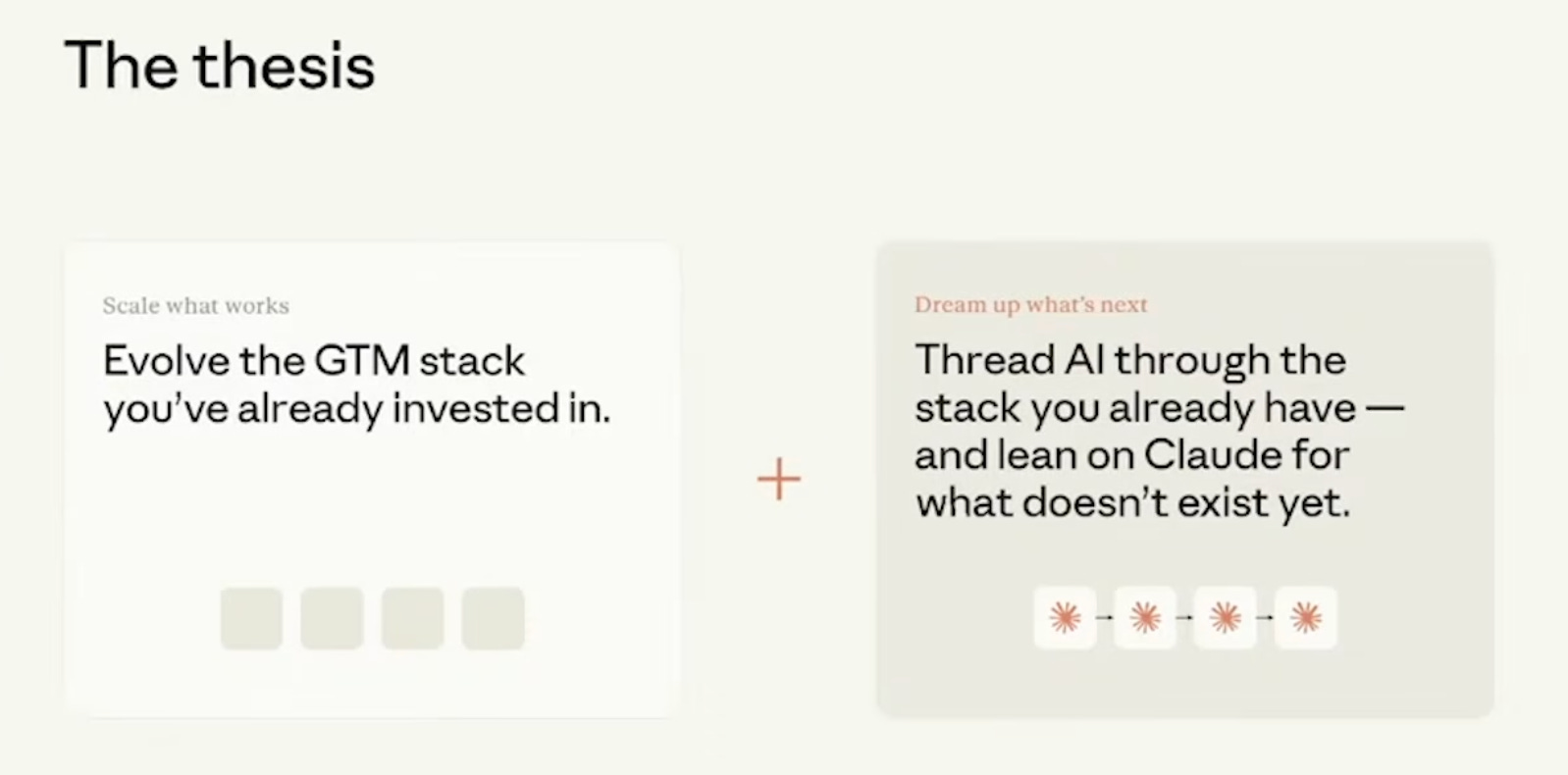

Most companies approach AI adoption the wrong way.

They buy another AI product. Add another dashboard. Create another workflow. And end up with seven disconnected tools instead of six.

Anthropic took the opposite approach.

After demand for Claude exploded following the release of Claude Opus 4.6, the company faced a problem most startups would love to have: more inbound demand than its sales team could handle.

Recently, Jason Lemkin (Founder of SaaStr) shared a YouTube video on this channel -

Instead of hiring hundreds of new reps or ripping out their existing software stack, they rebuilt the sales organisation around one idea:

Make AI the connective tissue between every system that already exists.

The result was remarkable.

54% of Anthropic’s new enterprise customers in 2026 came through a self-serve funnel.

Real enterprise accounts with contracts, invoicing, onboarding, and meaningful annual contract values.

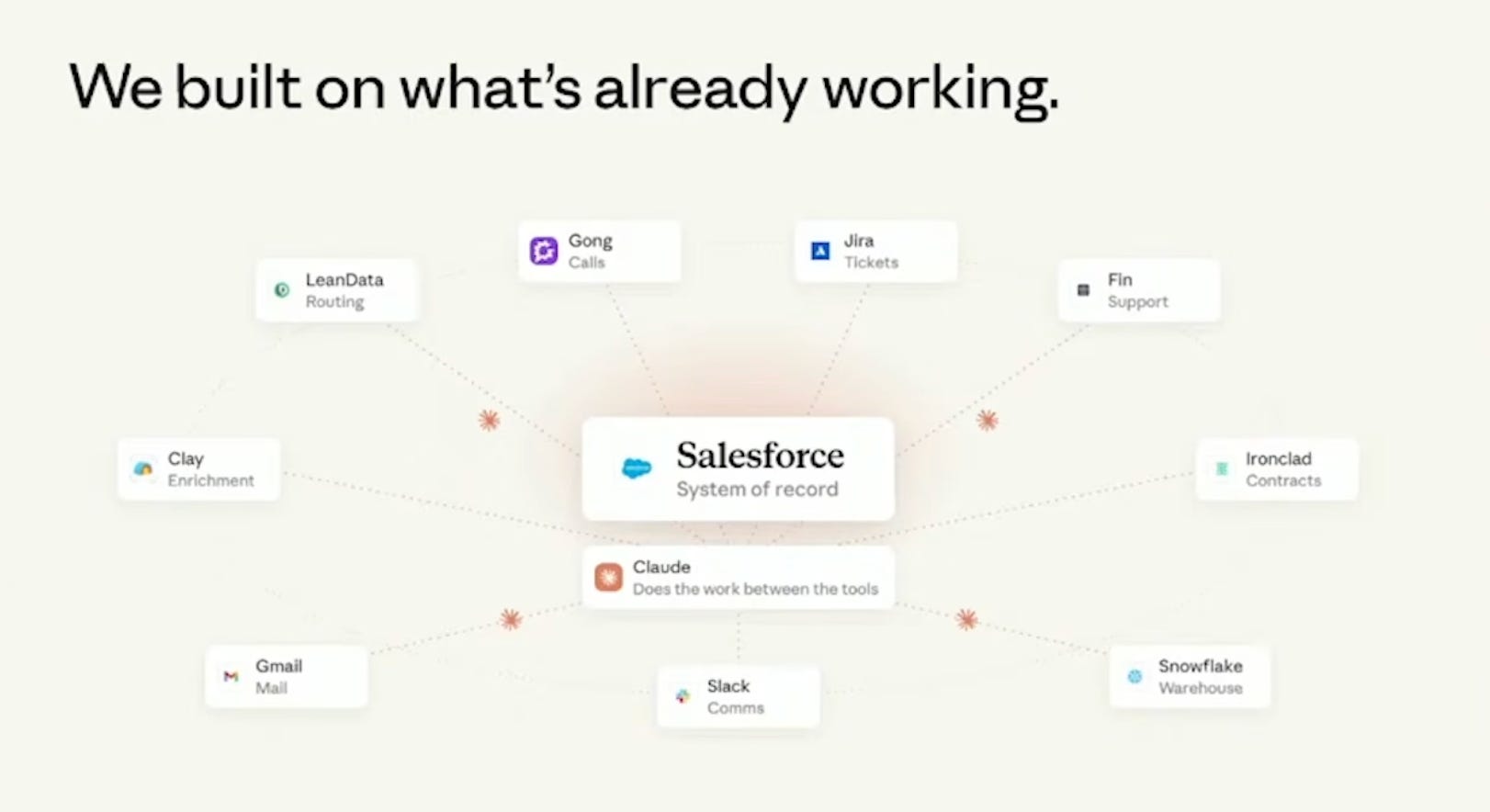

The interesting part is that Anthropic didn’t replace its existing tools.

Their core stack remained:

Salesforce for CRM and opportunity management

Go for call recordings and coaching

Ironclad for contracts

Slack for coordination

LeanData for lead routing

Clay for enrichment and qualification

Claude sits in the middle and connects them all. Think about how most sales reps work today.

A rep jumps between Salesforce, Slack, LinkedIn, email, Gong recordings, company websites, internal documents, pricing pages, and spreadsheets just to prepare for one customer conversation.

The actual selling often takes less time than gathering context. Anthropic’s insight was that AI should eliminate those transitions.

A rep now starts the day with a Claude-generated briefing.

It pulls information from Salesforce, Gmail, Slack, calendars, Gong, customer conversations, and internal documents, then produces a prioritised list of actions:

Which deals need attention

Which customers require follow-up

Which emails matter

Which opportunities are at risk

Instead of opening ten tabs, the rep starts with a single source of truth.

Before a customer call, reps use a “Call Prep” skill.

Rather than spending 30 minutes researching the account, Claude generates a briefing that includes:

Customer history

Stakeholders involved

Previous conversations

Discovery questions

Competitive positioning

Public company information

Five minutes of preparation replaces half an hour of manual work. What’s even more interesting is how Anthropic handled internal operations.

One of the biggest bottlenecks in enterprise sales isn’t selling. It’s getting answers.

Legal approvals.

Security reviews.

Pricing exceptions.

Vendor onboarding.

Contract redlines.

Every sales organisation eventually gets slowed down by support functions that can’t scale as fast as revenue teams.

Anthropic’s solution was simple: Slack became the front door for everything.

An employee submits a request in Slack. Claude reviews it first. If the answer already exists in policy or precedent, Claude resolves it immediately.

If escalation is needed, Claude packages all relevant context and sends it to the appropriate human. Instead of endless email threads, approvals move through a structured workflow.

The broader lesson is that AI’s biggest impact inside enterprises may not be automation.

It may be orchestration.

For years, enterprise software revolved around systems of record. The company that owned the database won.

Now we’re moving toward systems of intelligence. The winner may not be the company storing the data. It may be the company helping employees make decisions using that data.

Anthropic also did something many organisations still haven’t figured out: They turned their best sales reps into software.

The company identified high-performing workflows and packaged them into reusable Claude “Skills.”

Every new rep gets access to:

Morning Briefings

Call Preparation

Customer Follow-Ups

Competitive Intelligence

Custom Asset Creation

Instead of hoping new hires learn from top performers, best practices become part of the system. A new employee effectively starts with years of organisational knowledge already embedded into their workflow.

That’s probably the most important takeaway from this story. Most companies think AI adoption means replacing people.

Anthropic used AI to amplify people. They connected everything together. And that’s a pattern we’re starting to see across modern organisations.

The biggest AI opportunity isn’t creating another tool. It’s eliminating the friction between the tools companies already use.

Now you might be able to connect the previous write-up line - But the next generation of billion-dollar companies may not own the database. They may own the intelligence layer sitting on top of it.

📬 Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Atomus, a Menlo Park, CA-based newly formed venture capital firm, is reportedly raising a $500m fund. (Link)

Transition Ventures, a London, UK and NYC-based early-stage investment firm, closed its second fund at $150m. (Link)

Bridgewest Ventures, an Auckland, New Zealand- and Miami, FL-based venture capital arm of Bridgewest Group, held the first close of Bridgewest Venture Fund I LP, at approximately NZ$60.2m. (Link)

Veriten, a Houston, TX-based research, strategy and investment firm, held the initial close of its second flagship energy venture fund at over $105m. (Link)

New Startup Deals

Saris, a San Francisco-based agentic workflow platform for banks and credit unions, raised $28.8M in Series A funding.(Link)

Rep AI, a NYC-based AI platform for ecommerce brands, raised $6.2M in funding.(Link)

Slamcore, a London-based spatial intelligence software company, raised $14M in funding backed by ROKStar Ventures.(Link)

ClearNote Health, a San Diego-based cancer early detection company, raised $52M in Series D funding.(Link)

Stride, a Vietnam-based clean energy fintech startup, raised $15M in Series B funding. The round was co-led by Lightrock and TRIREC.(Link)

GEEIQ, a London-based analytics platform for games and virtual worlds, raised $6.8M in funding. The round was led by YFM Equity Partners.(Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: With a leading investor group, we have created an all-in-one VC interview preparation guide for aspiring VCs. Don’t miss this. (Access Here)

Finance & Operations Manager - Antler | Singapore - Apply Here

Venture Fellow - Entrepreneur First | France - Apply Here

Investment Team - Antler | Germany - Apply Here

Investor (Senior Associate/Principal) - Square Peg | USA - Apply Here

Senior Analyst - ICONIQUE Capital | USA - Apply Here

Venture AI & Operations Specialist - Blum Venture | Austria - Apply Here

Program Manager - a16z | USA - Apply Here

Associate - Manhattan Venture | USA - Apply Here

VP — Finance & Compliance - Transition VC | India - Apply Here

Senior Associate - ICONIQUE CAPITAL | USA - Apply Here

Venture Capital Analyst - MicroVentures | USA - Apply Here

Investment Associate - Struck Capital | USA - Apply Here

Director - General Atlantic | USA - Apply Here

Investment Associate - Transition | UK - Apply Here

Visiting Engineer - AI Fund | USA - Apply Here

Associate Investor - Sky9capital | USA - Apply Here

🔴 PARTNERSHIP WITH US

Get your product in front of over 120,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

Hi Sahil! Yet another insightful read. Regarding fund size, I would describe it as consensus capital for larger funds. This is because larger fund sizes require larger returns to break even, so managers tend to fund ideas that are in consensus and make them risk-conscious. However, as you correctly pointed out, valuations are rising much faster, so even to maintain a small ownership stake in a winner, emerging managers have to raise more capital. Furthermore, Brain Computer Interfaces (BCIs) can succeed only if they ensure mass-scale adoption. I think, for mass-scale adoption, cost is key, as it ensures accessibility to more people. Costs would fall with scale, and the potential of such technology towards treating diseases such as Parkinson's is huge.