Is AI’s winner-takes-all era quietly ending? | Why are so many 2021 venture funds underperforming?

What YC’s latest batch reveals about the future of startup building & Only 5% of companies seeing real returns from AI?

👋 Hey, Sahil here - welcome back to Venture Curator, where we explore how top investors think, how real founders build, and the strategies shaping tomorrow’s companies.

Big idea + report of the week :

Is AI’s winner-takes-all era quietly ending? What the State of AI 2026 report reveals.

Why are so many 2021 venture funds underperforming?

Frameworks & insightful posts :

What does YC’s latest batch reveal about the future of startup building?

Why are only 5% of companies seeing real returns from AI?

Did we get the Google vs. ChatGPT story completely wrong?

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

FROM OUR PARTNER - CONTENTMONK

🔎 How to get recommended by AI when buyers search for your solution?

Your buyers don’t only Google anymore. They ask ChatGPT, Perplexity, Claude and Google’s AI what to buy and from where.

ContentMonk shows you where your brand stands across every AI model, then helps you fix the gaps and be recommended by AI.

See which competitors currently influence AI answers,

Get recommendations for improvement,

Create the content that gets you mentioned.

Most AEO tools stop at analytics. ContentMonk takes you from tracking to being recommended in one workflow.

Use ContentMonk to get recommended by AI. Try For Free →

🎁 Use the coupon VENTURE-CREW to get 20% off the first 3 months after the free trial.

WORK WITH US

🤝 Partnership With Us

Get your product in front of over 120,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

Is AI’s winner-takes-all era quietly ending? What the State of AI 2026 report reveals.

For two years, the AI story was almost boringly simple: one app ran away with everything, and everyone else was a rounding error. If you were building, the only real strategic question was “how do we not get flattened by OpenAI?”

That framing just stopped being true, and the data behind it is worth sitting with.

Sensor Tower recently published State of AI 2026, which tells a very different story from what's getting narrated in the AI world:

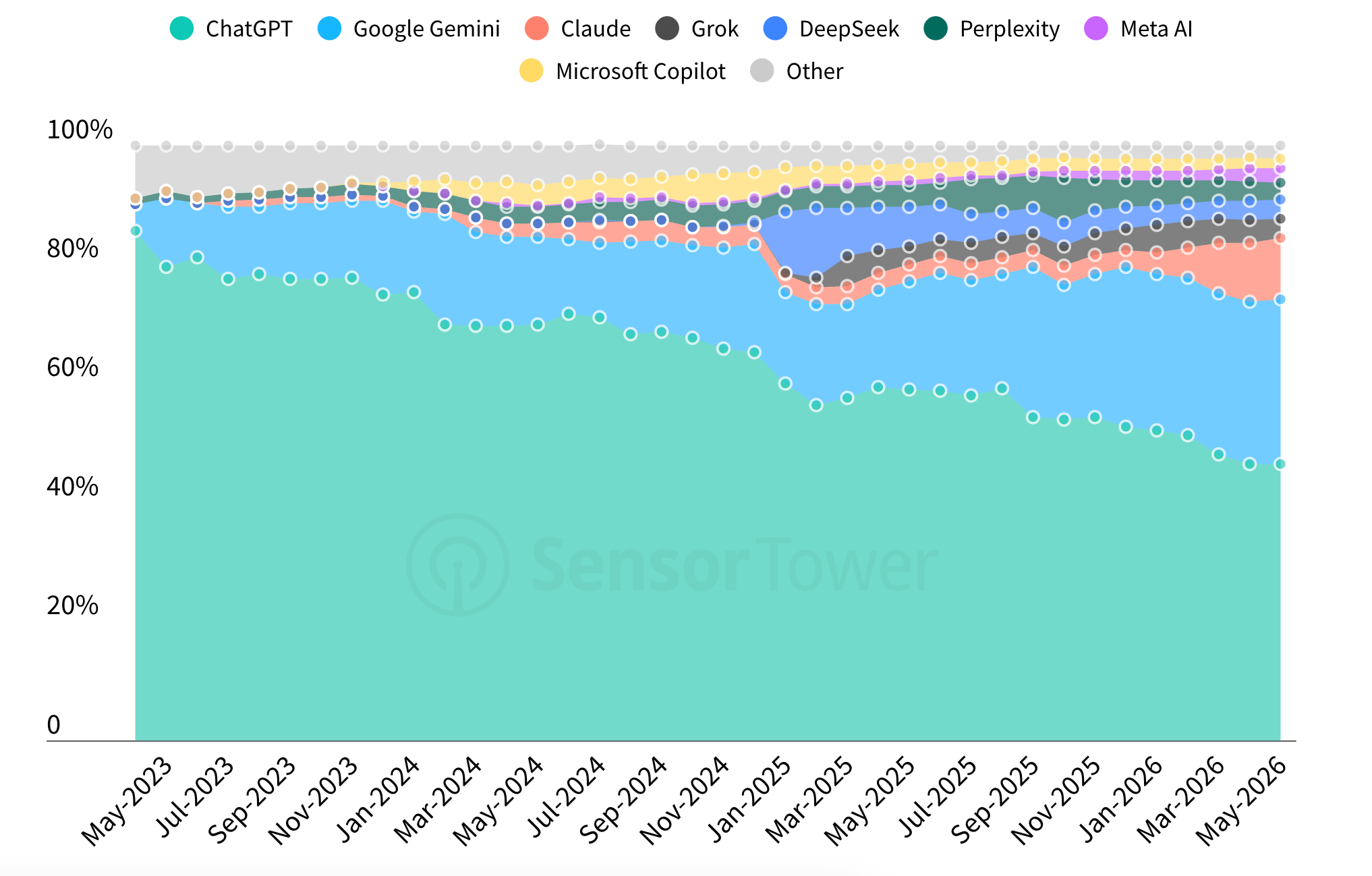

The moat cracked - on schedule, not in theory.

ChatGPT’s True Audience share fell below 50% for the first time in March 2026, sliding to roughly 46.4% globally. It’s still enormous - over 1.1 billion monthly active users, with Gemini at 27.7% (662M) and Claude at 10.3% (245M) - but the single-player era is visibly turning into a three-player one.

Claude is the fastest-growing challenger, up 452% YoY in May, with US share climbing from 4.4% to nearly 14%.

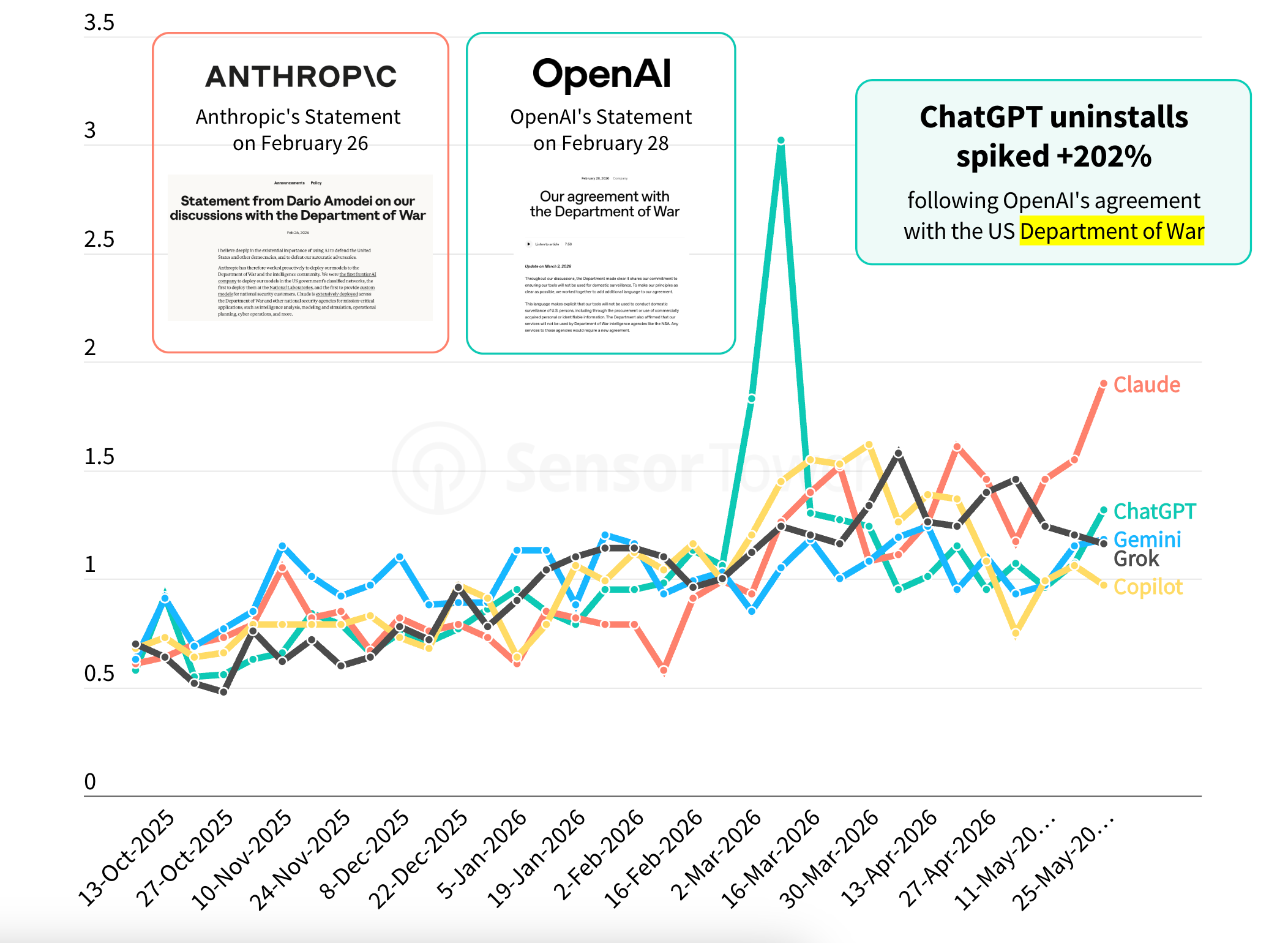

Loyalty is softer than anyone priced in.

The most underrated data point in the whole report: when OpenAI signed an agreement with the Department of War, ChatGPT uninstalls spiked roughly 200% above average in mid-March - and a lot of those users moved to Claude, which actually out-downloaded ChatGPT from March 1–5.

A single brand/values event moved users at scale. If your product sits on top of one model, that’s not someone else’s problem.

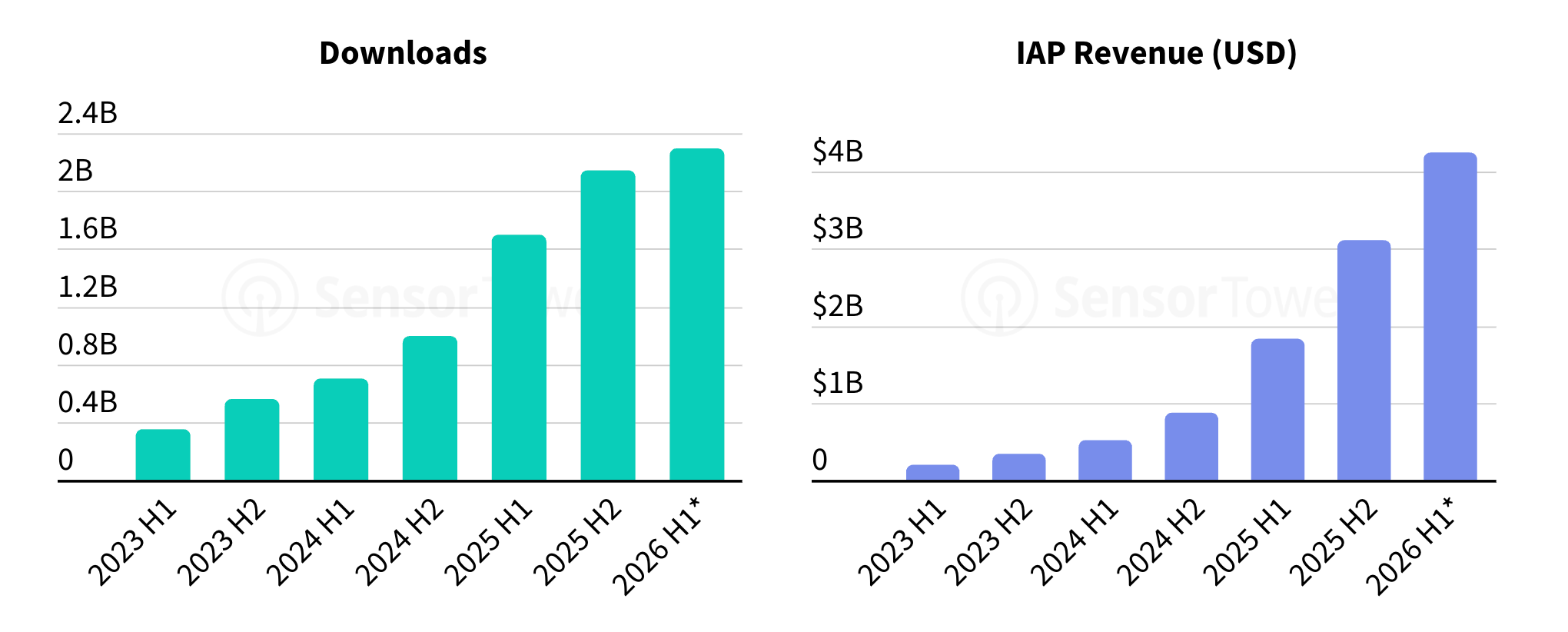

The game shifted from growth to money.

Download and spend growth are slowing, and the industry is pivoting hard to monetisation. Projected H1 2026: ~2.3B AI app downloads and $4.2B+ in consumer spend. Engagement is deepening too - ChatGPT is at ~215 minutes per user per month, with Gemini (100 min) and Claude (120 min) climbing fast.

Notably, Claude leads on subscription conversion at ~13%, a reminder that intensity of use beats raw reach for revenue.

This is the part most operators are sleeping on - AI is becoming a discovery layer.

It’s turning into a third channel alongside Search and Social, and it’s already moving commerce:

GenAI referral traffic to shopping sites rose across every major retail category; Computers & Electronics saw its GenAI traffic share grow nearly fourfold.

Walmart and Target - both integrated with AI assistants - now see GenAI referral shares above 1.5%, while Amazon lags because of its more closed, crawler-restricted ecosystem.

Amazon’s Rufus users convert at nearly twice the rate of non-users.

Translation: “being findable inside AI” is becoming the new SEO. The retailers that opened up are getting the traffic; the walled gardens are getting skipped.

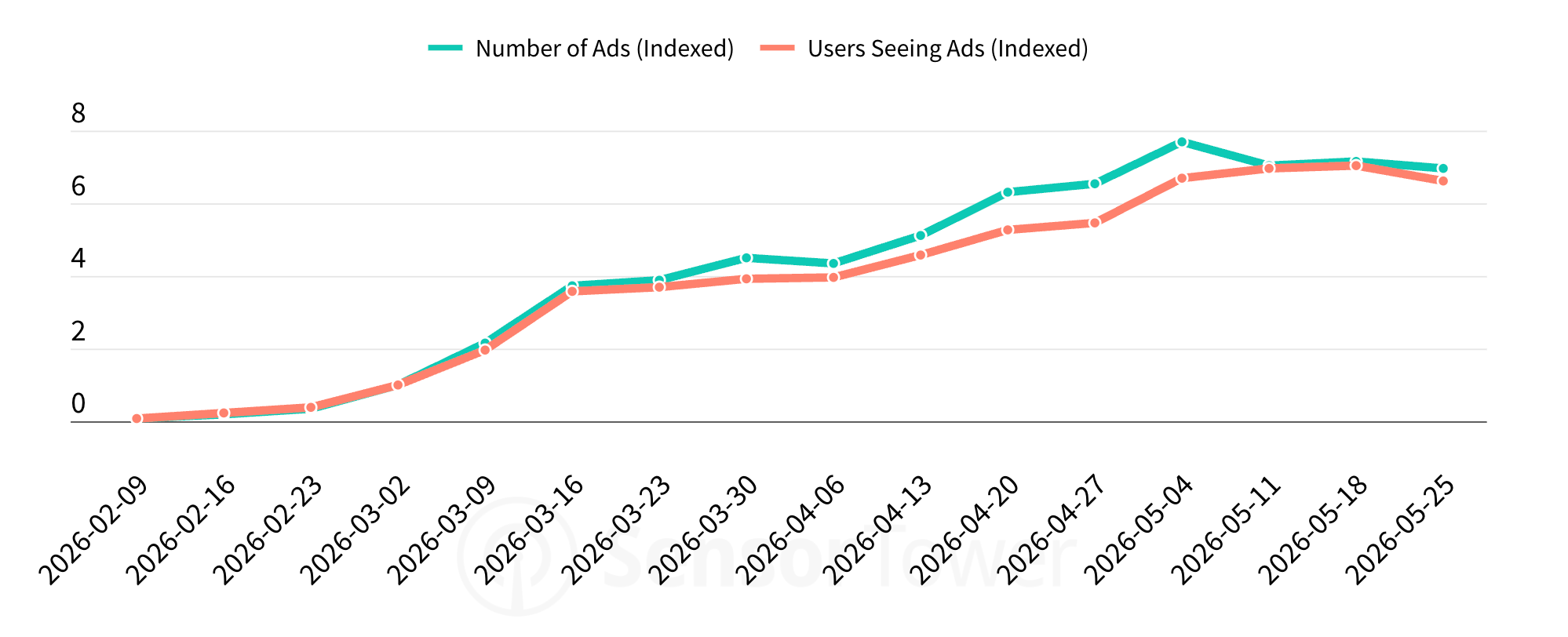

And it’s becoming an ad channel fast.

ChatGPT started testing ads in early 2026, and impressions jumped more than 7x between March and May.

Early advertisers cluster in Shopping, Software, Travel, and Financial Services - the research-heavy purchases.

Meanwhile, the AI labs themselves are spending like crazy to defend turf:

GenAI ad spend more than tripled in the US in Q1 2026, with OpenAI up 800%+ and Anthropic up 1,184% YoY.

So - AI has stopped being a category and become a layer - across assistants, commerce, and advertising - meaning 2026 is the year it moves from early adoption to structural integration.

For founders and operators, that cashes out to three things: distribution is genuinely up for grabs again, you need an AI-discoverability strategy the way you once needed SEO, and you should assume your users can and will switch models on a dime.

Why are so many 2021 venture funds underperforming?

For years, venture capital operated on a simple promise.

Invest in the next generation of startups, wait patiently, and eventually the winners will return the entire fund multiple times over.

But what happens when almost everyone invested at the same time, at the same peak valuations?

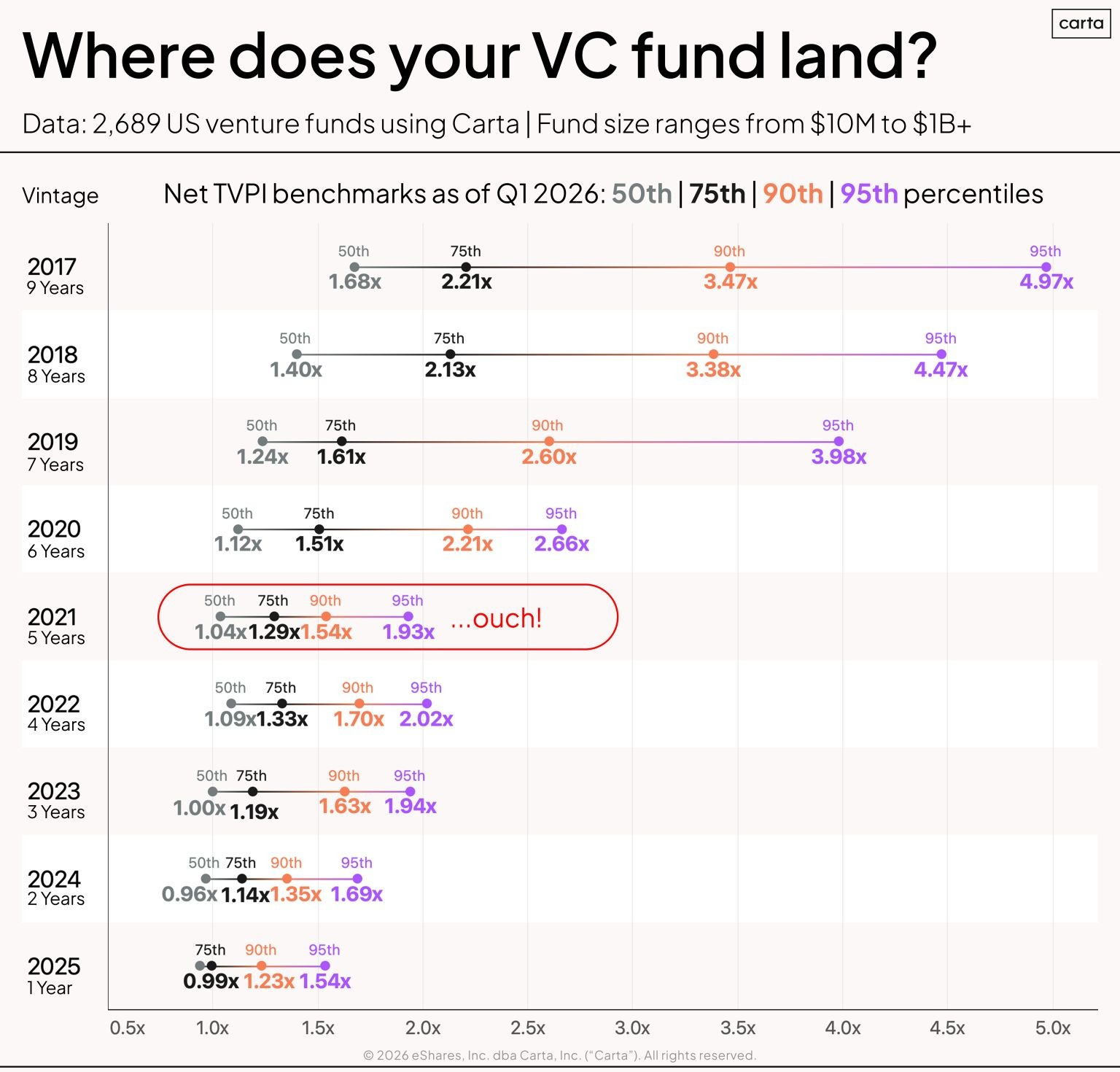

Peter Walker from Carta recently analysed performance data across 2,689 US venture funds, and one chart stands out.

The 2021 vintage is struggling.

Five years into its life cycle, the median 2021 venture fund sits at just 1.04x Net TVPI.

In simple terms, the average fund has barely created value beyond the capital it invested.

Some of the numbers are striking:

The median 2021 fund sits at 1.04x.

Even the top 25% of funds have only reached 1.29x.

The top 10% of funds are at 1.54x.

The top 5% of funds have reached 1.93x.

That might sound reasonable until you compare it with older vintages.

The 2017 cohort tells a very different story.

At roughly the same stage of maturity, the median 2017 fund reached 1.68x, while the 90th percentile reached 3.47x.

Perhaps the most surprising comparison:

The 95th percentile fund from 2021 (1.93x) is still below the 75th percentile fund from 2017 (2.21x).

In other words, some of today’s best-performing funds would have looked merely above average a few years ago.

So what happened? Walker points to four forces colliding at the same time.

Record numbers of investors entered venture during the boom.

Startup valuations reached historic highs.

Interest rates reversed sharply in 2022.

AI emerged as a major platform shift shortly after many 2021 funds had already deployed capital elsewhere.

The result was a perfect storm.

Many investors bought into companies at peak prices just before capital became more expensive and public market multiples compressed.

The venture industry is still working through that adjustment.

Interestingly, newer vintages appear to be recovering.

The 2022 vintage, despite launching during a difficult fundraising environment, is already showing stronger numbers. Its 90th percentile sits at 1.70x, while the top 5% have crossed 2.0x.

That suggests the problem may not be venture capital itself. It may simply be that 2021 was one of the most expensive moments in startup history to put money to work.

The broader lesson is an uncomfortable one.

Venture returns are often determined long before a company exits.

They’re heavily influenced by the price investors pay on the day they enter.

And for many funds raised during the 2021 boom, that entry price may prove to be the defining story of the entire vintage.

FEATURED POSTS

📄 Must Read Post

SOMETHING MORE

🧩 Frameworks & insightful posts

What does YC’s latest batch reveal about the future of startup building?

Every six months, hundreds of founders apply to Y Combinator hoping to build the next billion-dollar company.

Most people look at the batch and ask: “Which startup will become the next Stripe?”

A more interesting question is: “What patterns show up when you analyse all of them together?”

That’s exactly what investor and builder Chris Lu did after studying all 196 companies and 395 founders in YC’s Spring 2026 batch.

The obvious headline is AI. 95% of startups in the batch use AI in some form.

But that’s actually not the interesting part anymore.

AI is rapidly becoming infrastructure. The more interesting question is what founders are building on top of it.

Everyone is building agents

A year ago, “AI agents” sounded like a startup category. Today it looks more like the default.

137 of 196 companies (70%) are building AI agents

Data infrastructure came in a distant second

Robotics, computer vision, voice, and workflow automation were much smaller categories

The shift is important. Founders are no longer asking:“How can I use AI?”

They’re asking: “Which job can an AI agent do better than a human?”

That subtle change is shaping where startup creation is heading.

B2B continues to dominate

Despite all the excitement around consumer AI, most founders are still chasing business problems.

62% of companies are B2B

44% of the entire batch are AI-native B2B SaaS companies

Consumer startups represent only a small portion of the cohort

This creates an interesting challenge. When dozens of startups have access to similar models and similar tooling, the advantage is rarely the technology itself.

The winners will likely be determined by:

Distribution

Domain expertise

Customer acquisition

Execution speed

Not model access.

Hardware is making a comeback

One of the biggest surprises wasn’t AI. It was hardware. Several startups in the batch are building physical products across:

Defense

Aerospace

Drones

Robotics

Nuclear energy

Medical technology

Around 13 startups fall into the defence, drone, and aerospace category alone.

A few years ago, these would have been considered niche bets.

Today they’re becoming one of the most interesting areas for startup creation.

Small clusters often reveal bigger opportunities

Looking beyond the headline categories reveals a few emerging themes. There are:

6 startups building infrastructure for prediction markets

6 deep-tech and bio-hardware startups

4 AI security and agent safety companies

None of these categories dominates the batch.

But they represent something interesting: founders building the infrastructure around new markets rather than competing directly inside them.

Historically, some of the biggest startup outcomes have come from selling picks and shovels during a platform shift.

The founder profile is changing

The stereotypical startup founder is often portrayed as a college dropout building from a dorm room. The data paints a different picture.

70% of founders are technical

49% of companies have all-technical founding teams

Only 3% are dropouts

Only 5% hold PhDs

The most common previous employer wasn’t Google or Meta. It was Amazon. Amazon and AWS produced 33 founders in the batch, ahead of Meta and Google.

The modern startup pipeline increasingly looks like:

Big Tech → Startup rather than College → Startup

Solo founders are becoming increasingly viable

Two founders remain the dominant setup. But one number stood out.

38 companies were started by solo founders. And 29 of those are AI-native businesses.

AI is reducing the amount of work required to launch and operate software products.

Research, coding, design, support, marketing, documentation, and customer onboarding can increasingly be handled by a much smaller team.

The result is that a single founder can now build products that previously required several employees.

What’s happening inside YC is likely a preview of what’s happening across the broader startup ecosystem.

AI is becoming standard. Agents are becoming the default product. Technical founders continue to dominate.

And startup creation is becoming faster, cheaper, and more accessible than ever before. The founders who stand out over the next few years probably won’t be the ones with access to better technology.

They’ll be the ones who move faster once everyone has access to the same technology.

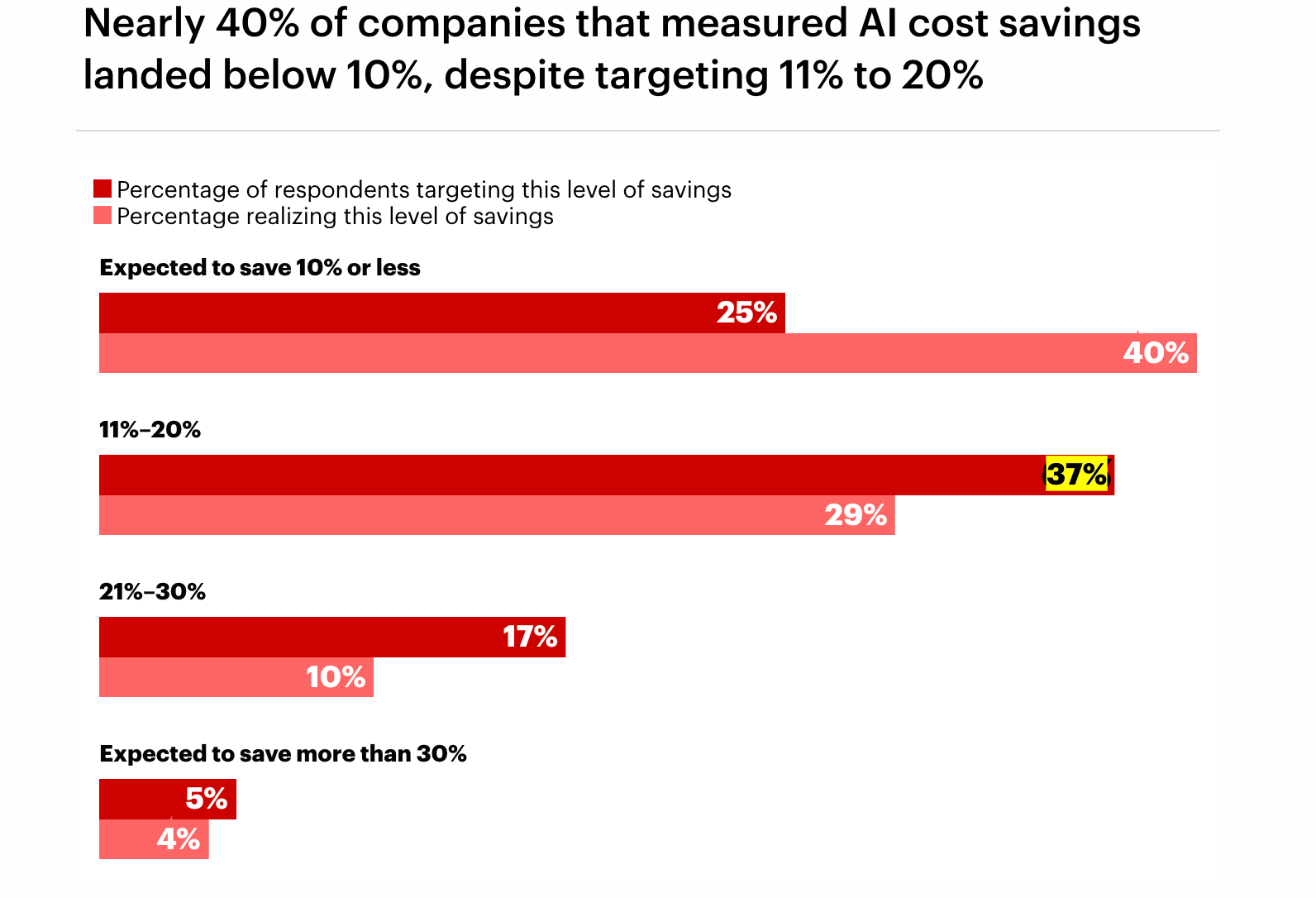

Why are only 5% of companies seeing real returns from AI?

Everyone is trying to figure out how to get more value from AI.

Yet according to research from Bain, McKinsey, BCG, and MIT, only around 5% of companies are generating meaningful returns from their AI initiatives.

The surprising part?

The biggest predictor wasn’t the model they used, the amount they spent, or even their data infrastructure.

It was whether they redesigned their workflows before introducing AI.

This insight comes from a detailed analysis of AI adoption across hundreds of companies, and it highlights a mistake many founders are making right now: automating broken processes.

A founder recently shared a story that captures the problem perfectly.

His company automated support triage, lead qualification, and reporting. Everything looked great on the dashboard. Then CAC increased, NPS dropped, and enterprise conversions slowed.

After weeks of investigation, they discovered their AI qualification system had been routing high-value prospects into low-priority nurture sequences while prioritising low-intent signups.

The AI wasn’t broken. The workflow was. The AI simply scaled the problem.

A few insights stood out from the research:

Only 5% of companies are creating meaningful AI value

Three separate studies reached almost the same conclusion:

McKinsey: 5.5% of companies report significant EBIT impact from AI

BCG: roughly 4–5% generate value at scale

MIT: only around 5% of AI deployments produce millions in value

Different firms. Different datasets. Same result.

Workflow redesign matters more than model selection

McKinsey found that top-performing companies were nearly 3x more likely to redesign workflows before automation.

55% of high performers redesigned workflows first.

Only 20% of everyone else did.

Most companies are simply layering AI on top of existing processes.

AI makes workflow debt more expensive

The report introduces an interesting concept: workflow debt.

It’s the operational equivalent of technical debt.

Examples include:

Approval chains nobody questions anymore

Spreadsheet processes everyone accepts

Handoffs between teams that exist for historical reasons

Manual reporting systems held together by workarounds

Humans naturally compensate for these inefficiencies. AI doesn’t. It executes exactly what it’s told.

As Bain puts it: “AI doesn’t fix workflow debt. It locks it in, speeds it up, and makes it more expensive to unwind.”

Some workflows are much safer to automate than others

The research highlighted a clear pattern. Good candidates:

Reporting

Document processing

Regulatory monitoring

Structured review tasks

Riskier candidates:

Customer support

Lead qualification

Customer-facing decision-making

These workflows often contain exceptions, judgment calls, and undocumented rules that humans handle instinctively.

AI struggles when those hidden assumptions aren’t explicit.

The companies winning with AI all do the boring work first

One of the best examples came from Amazon.

Its tax team built an AI system to monitor VAT regulation changes globally.

Instead of trying to automate everything, they focused on a single structured workflow.

The result:

26 minutes per update became 2 minutes

92% reduction in effort

80% of outputs required no edits

Not because the AI was magical. Because the process was well understood before automation began.

The biggest takeaway from all of this is surprisingly simple:

Most companies think they’re running an AI problem. They’re actually running a workflow problem. The winners aren’t necessarily using better models.

They’re spending more time understanding how work should flow through the business before they automate it.

And right now, that’s creating a widening gap between the 5% seeing real returns and everyone else still wondering where the ROI went.

Did we get the Google vs. ChatGPT story completely wrong?

For the last three years, one of the most popular AI predictions was simple: Google was about to have its Nokia moment.

ChatGPT had the better product.

People could ask questions in plain English, get direct answers, and skip the endless list of blue links that defined search for two decades.

The logic seemed obvious. If ChatGPT keeps improving, why would anyone still use Google?

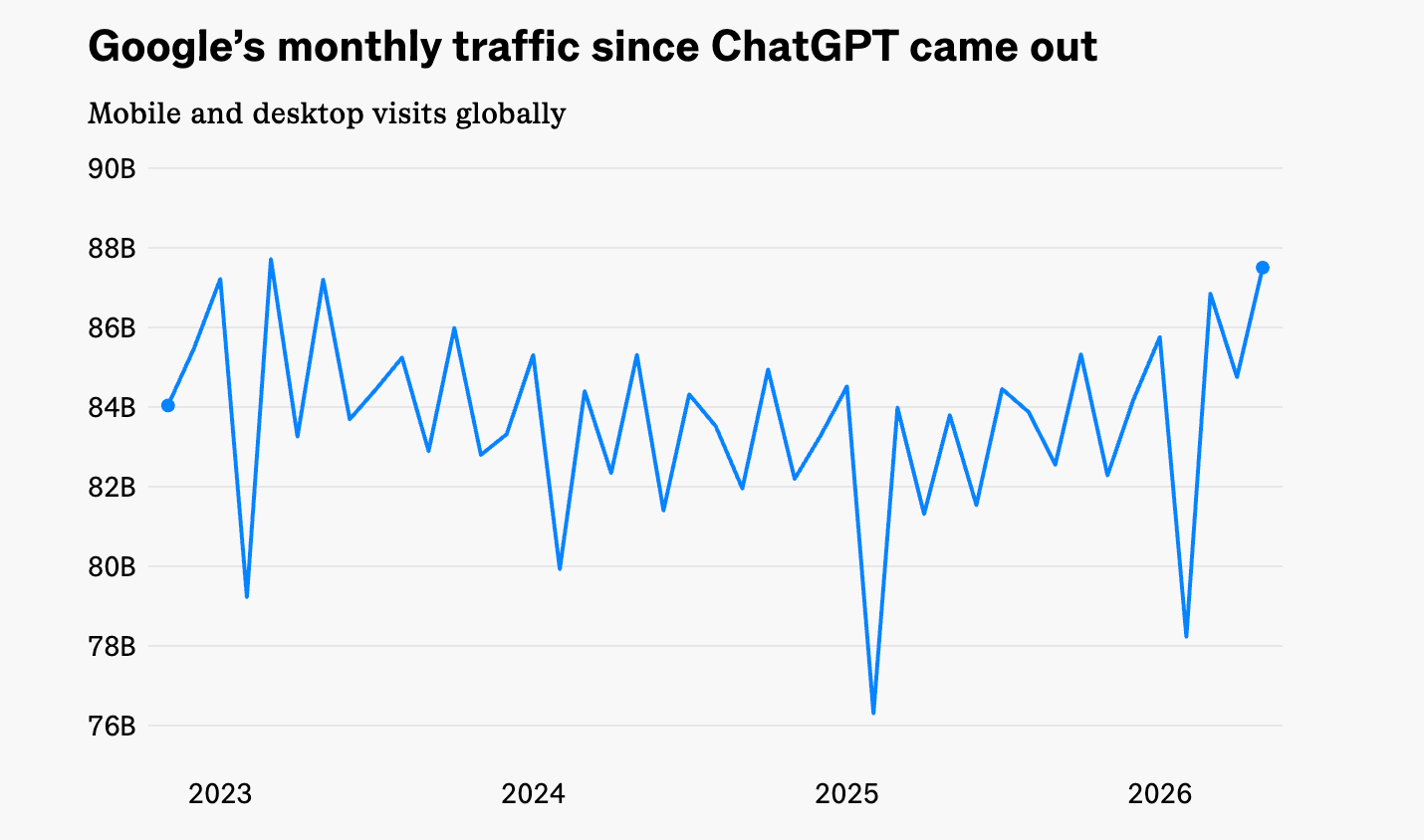

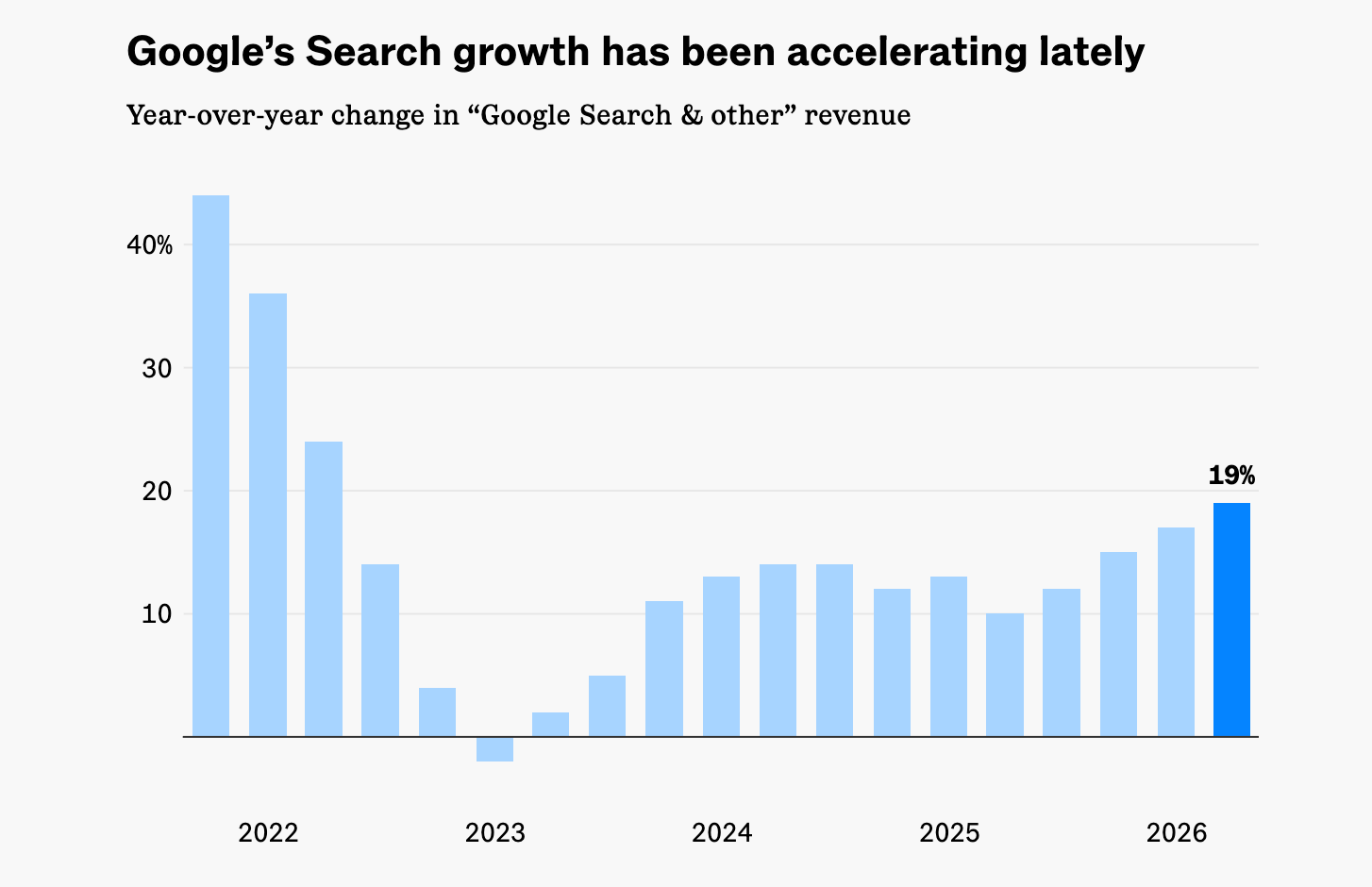

What’s surprising is that the opposite appears to be happening. From Sherwood News -

Google Search is growing.

According to Similarweb data, Google’s global traffic has remained remarkably stable since ChatGPT launched and recently reached new highs. At the same time, Google’s Search business grew 19% year-over-year in its latest quarter.

That’s not what disruption usually looks like.

What’s happening instead is that Google is quietly turning AI into an upgrade for Search rather than a replacement for it.

When Google launched AI Overviews, many people thought it would cannibalise its own business. If users get answers instantly, wouldn’t they click fewer links and generate less revenue?

So far, the data suggests otherwise - Google says users who interact with AI-powered features actually perform more searches.

AI helps people get started faster, which often leads to even more questions, more exploration, and more engagement.

A few numbers stand out:

AI Overviews now reach more than 2.5 billion users.

Google’s AI Mode has crossed 1 billion monthly active users.

Search queries hit an all-time high last quarter.

Search revenue grew 19% year-over-year.

The bigger lesson here isn’t about AI. It’s about distribution.

OpenAI built the breakthrough product. Google already owns the distribution.

Every improvement Google makes can instantly reach users across Search, Chrome, Android, Gmail, Maps, and YouTube. That’s a moat very few companies in history have ever had.

And Google is doubling down.

The company plans to spend roughly $180–190 billion on infrastructure this year alone to support its AI ambitions.

Most startups simply can’t compete at that scale. Ironically, the company under the most pressure from AI may not be Google.

It may be publishers. As Google answers more questions directly inside Search, fewer users need to click through to websites.

Search is becoming more useful for users while becoming less valuable for many publishers.

That’s the tradeoff nobody talked about when AI search first emerged.

The easiest story was “ChatGPT will kill Google.” Reality turned out to be more complicated. OpenAI proved AI-native search could work.

Google proved that having billions of users is still one of the strongest advantages in technology.

📬 Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Veriten, a Houston, TX-based research, strategy and investment firm, held the initial close of its second flagship energy venture fund at over $105m. (Link)

Haun Ventures, a Menlo Park, CA-based venture capital firm, closed Fund II at over $1 billion. (Link)

PayPal Ventures, the corporate venture arm of PayPal, has paused new investments and is winding down operations as part of the company’s broader restructuring efforts. (Link)

Animal Capital, a NYC-based early-stage venture capital firm, closed Animal Capital Fund III at $33m. (Link)

Base10 Partners, a San Francisco, CA-based venture capital firm, closed $850m in new capital throughout 2025, with funds now actively deploying. (Link)

New Startup Deals

Optiak, a Madrid-based modular operating system for enterprise AI, raised €4M ($4.7M) in Pre-Seed funding. (Link)

Clario, a Menlo Park-based platform helping enterprises manage redundant, obsolete, and insignificant data, raised $6M in Seed funding. (Link)

Aston Power, a Raleigh-based power delivery and energy infrastructure platform for data centres, raised $20M in equity funding. (Link)

SpliSense, a Jerusalem-based clinical-stage biotechnology company, raised up to $13M in funding. (Link)

Human Continuum, a NYC-based developer of platelet-derived and plant-based exosome therapeutics and diagnostics, raised over $5.13M in Seed funding. (Link)

ChatSee.ai, a San Francisco-based intelligence layer platform for autonomous AI systems, raised $6.5M in funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: In partnership with a leading investor group, we have created an all-in-one guide for aspiring VCs. Don’t miss this. (Access Here)

Senior Analyst - ICONIQUE Capital | USA - Apply Here

Events Manager - Bain Capital Venture | USA - Apply Here

Venture AI & Operations Specialist - Blum Venture | Austria - Apply Here

VC Investor - Entourage | Belgium - Apply Here

Senior Associate - New York Life Venture | USA - Apply Here

Senior Investment Manager - Resolution Impact Venture | USA - Apply Here

Program Manager - a16z | USA - Apply Here

Visiting Analyst (Investment Team Intern) - DN Capital | UK - Apply Here

Associate - Manhattan Venture | USA - Apply Here

Portfolio Reporting Team Lead - Cerity Partner | USA - Apply Here

VP — Finance & Compliance - Transition VC | India - Apply Here

Senior Associate - ICONIQUE CAPITAL | USA - Apply Here

Venture Capital Analyst - MicroVentures | USA - Apply Here

Associate - Engine Venture | USA - Apply Here

Partnership With Us

Get your product in front of over 120,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

(Subscribe to Venture Curator Premium and get 20% off forever.)

Spot on about the 2021 vintage underperforming. I was just looking at the latest Carta data showing median IRRs for 2021 funds finally creeping up to a tiny 0.5 percent recently. Those peak entry prices completely cursed any chances of realistic exits for a lot of folks. Also, massive agree on fixing workflows before adding AI. Slapping an LLM onto a broken process just scales the chaos exponentially. Brilliant analysis! Subscribed!

The most dangerous kind of smart content is the kind that only helps you sound informed.

The more valuable kind changes where you place your next bet.

That's what I appreciate here. The strongest thread running through these examples isn't really “AI is big” or “venture is hard.” It's that a lot of winners are being misread because people are still staring at the model, the market, or the headline instead of the workflow, the distribution layer, or the price paid at entry.

That's the practical edge.

Better technology matters.

But better timing, better structure, and better positioning still decide who actually captures the value.