What 16,000 companies reveal about AI agent adoption? | AI’s next $1 trillion market (and most founders are missing it).

Anthropic guide on building AI agents as a non-technical founder & VC Jobs.

The Next-Gen Drug Targeting a $560B Disease…

Osteoarthritis affects 500+ million people with no way to stop it*. Current treatments just mask the pain of degrading joints. Curing this $560 billion disease means winning one of medicine’s biggest opportunities.

Cytonics aims to do just that.

They may have discovered what soon could be osteoarthritis’ first potential cure. They successfully cleared Phase 1 clinical trials with a perfect safety profile*.

Now, they’re gearing up for the next phase on a version engineered for mass production.

Become an early-stage Cytonics investor before the opportunity ends later this month.

This is a paid advertisement for Cytonics Regulation CF offering. Please read the offering circular at https://invest.cytonics.com/

Forward-looking statements are subject to risks and uncertainties. There is no guarantee of performance. Past performance does not predict future results. All investments involve risk, including loss of principal.

*Source: The Lancet Rheumatology

*Phase 1 clinical trials are designed primarily to assess safety and tolerability and do not establish efficacy. Clinical trial results are preliminary, and there can be no assurance that future trials will be successful or that any product candidate will receive regulatory approval.

This Week at a glance -

Big idea + report of the week :

AI agent reality check: What 16,000 companies reveal about AI agent adoption?

The $212.9B venture paradox: Why most founders still can’t raise.

Why are U.S. companies quietly switching to Chinese AI models?

Frameworks & insightful posts :

The Task Economy: AI’s next $1 trillion market (And most founders are missing it).

How to build AI agents as a non-technical founder (Anthropic’s guide).

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

WORK WITH US

🤝 Partnership With Us

Get your product in front of over 125,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

START WITH

🧠 Big idea + report of the week

AI agent reality check: What 16,000 companies reveal about AI agent adoption?

Autonomous AI agents are one of the biggest technology trends of 2026, promising to handle complex workflows with minimal human involvement. But while adoption is accelerating, most companies are still trying to figure out how to deploy them successfully.

A new report by FirstPageSage combining data from 30+ industry studies and 16,000+ businesses offers one of the clearest snapshots yet of where agentic AI stands today.

Adoption is growing, but deployment remains early

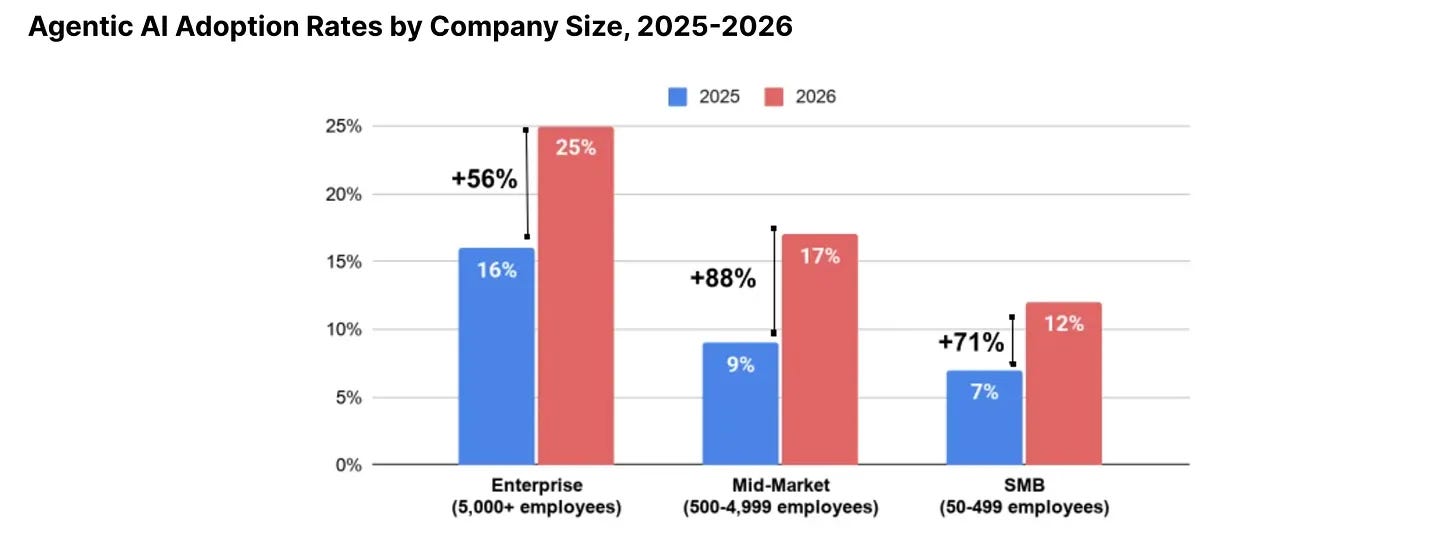

Enterprise companies lead adoption with 25% already using agentic AI in some form, while mid-market and SMBs are catching up quickly.

However, across every company size, the vast majority of deployments remain in the experimentation stage. Only 11% of enterprises, 6% of mid-market firms, and 2% of SMBs have deployed AI agents at scale.

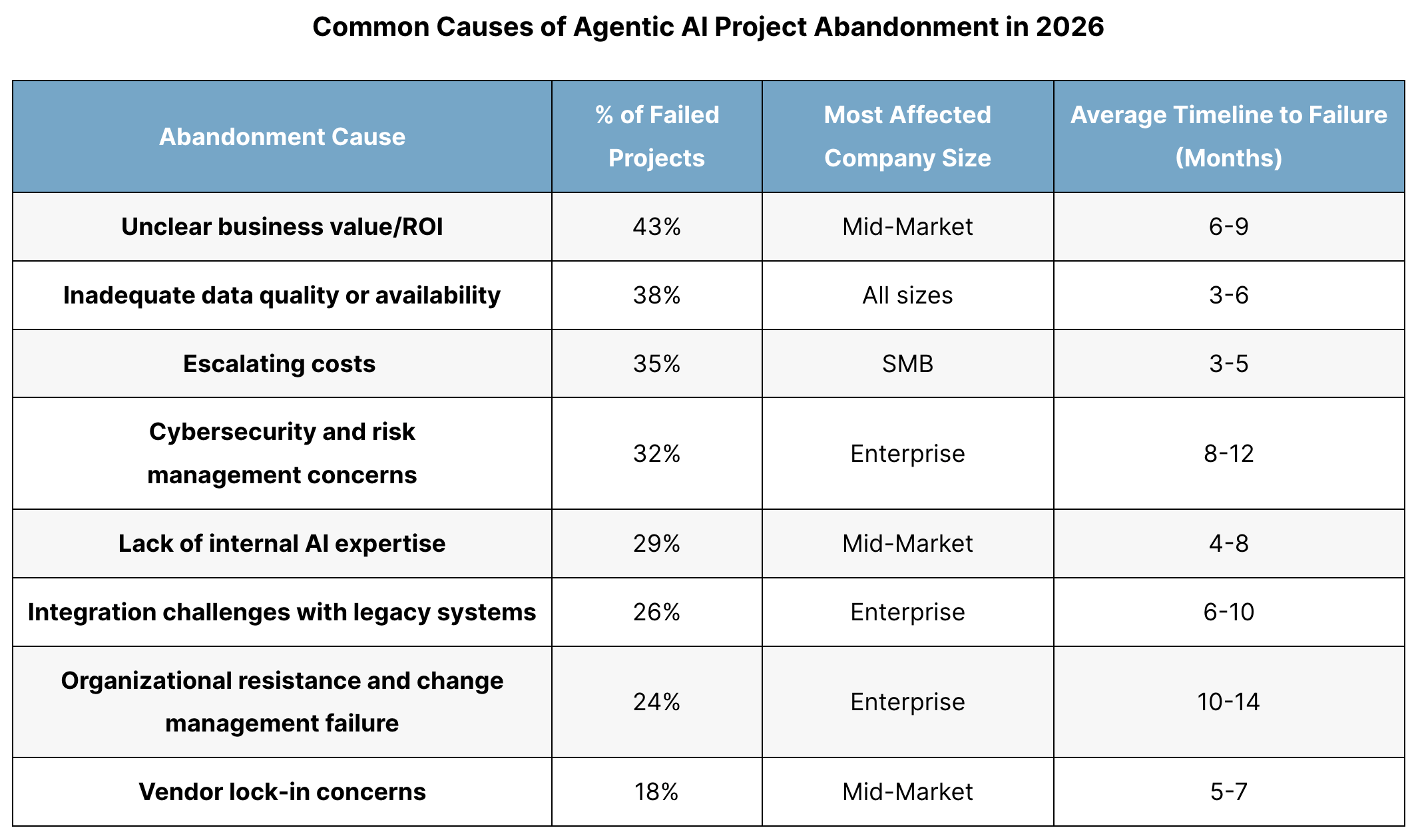

The biggest challenge isn’t the AI - it’s the business.

The leading reasons projects fail are unclear ROI (43%), poor data quality (38%), rising implementation costs (35%), cybersecurity concerns (32%) and a lack of internal AI expertise (29%).

The report suggests that many companies begin AI projects before building the data infrastructure and processes needed to support them.

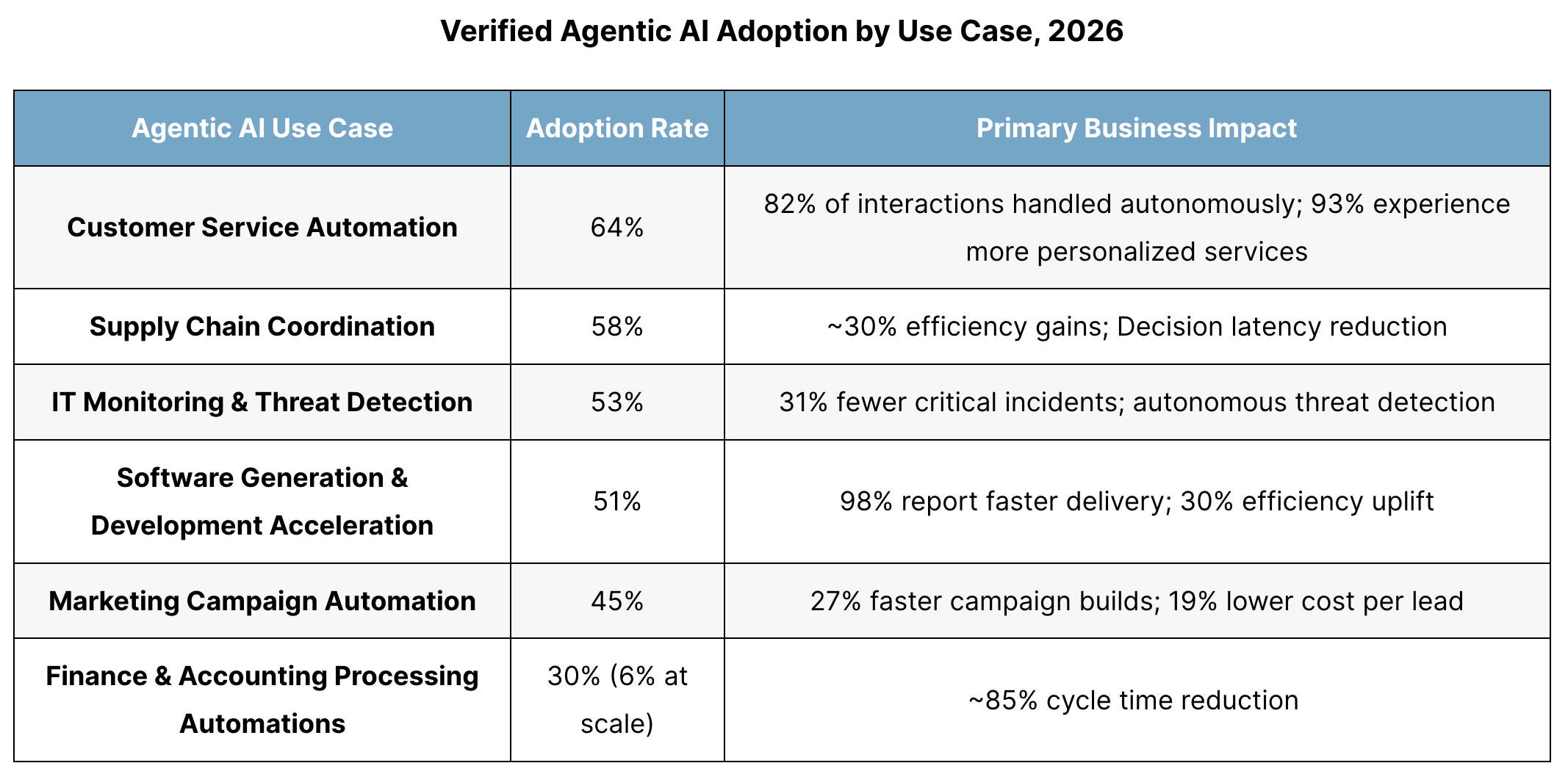

Customer service is leading real-world adoption.

Around 64% of enterprise and mid-market deployments focus on customer support, followed by supply chain coordination (58%), IT operations (53%) and software development (51%).

Highly regulated functions like finance remain much earlier in adoption due to governance and compliance requirements.

The bigger opportunity may not be building another AI agent, but helping businesses successfully deploy them.

Companies increasingly need better data infrastructure, integration tools, governance software, monitoring platforms and implementation services before AI agents can deliver measurable business value.

As adoption moves beyond experimentation, the businesses solving these operational challenges are likely to become just as valuable as the AI models themselves.

The $212.9B venture paradox: Why most founders still can't raise.

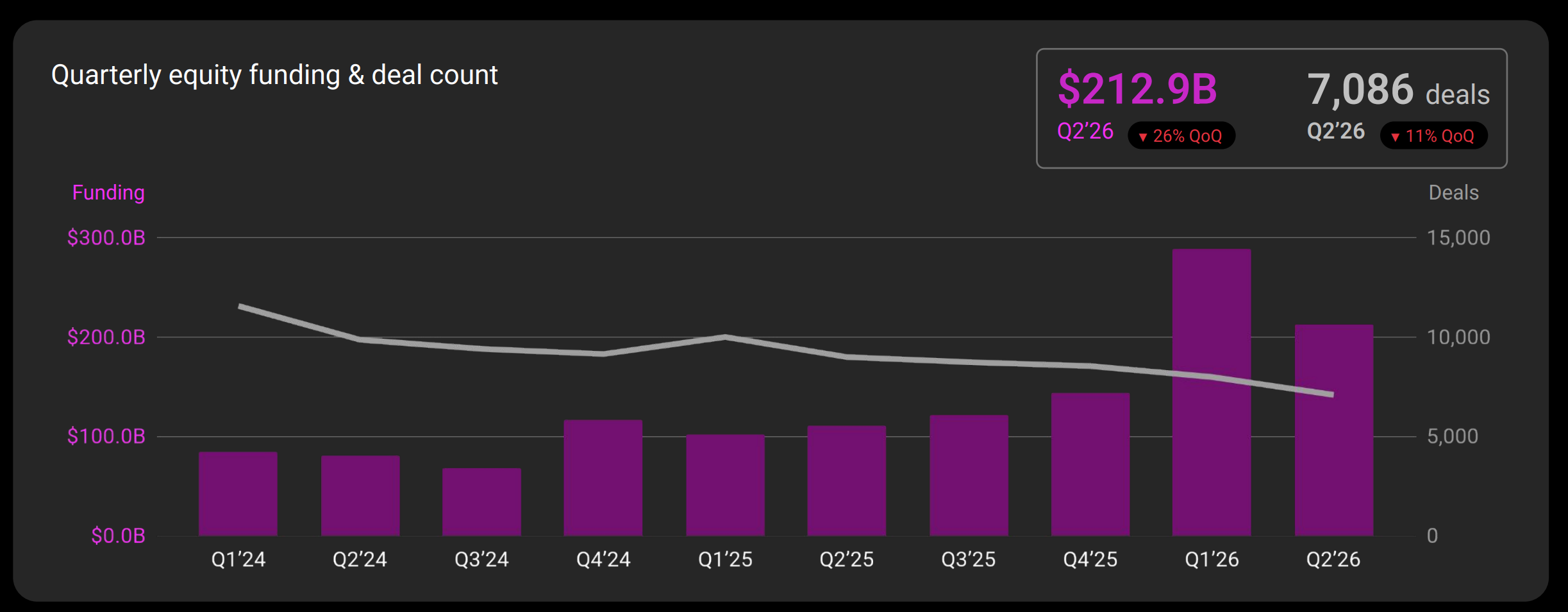

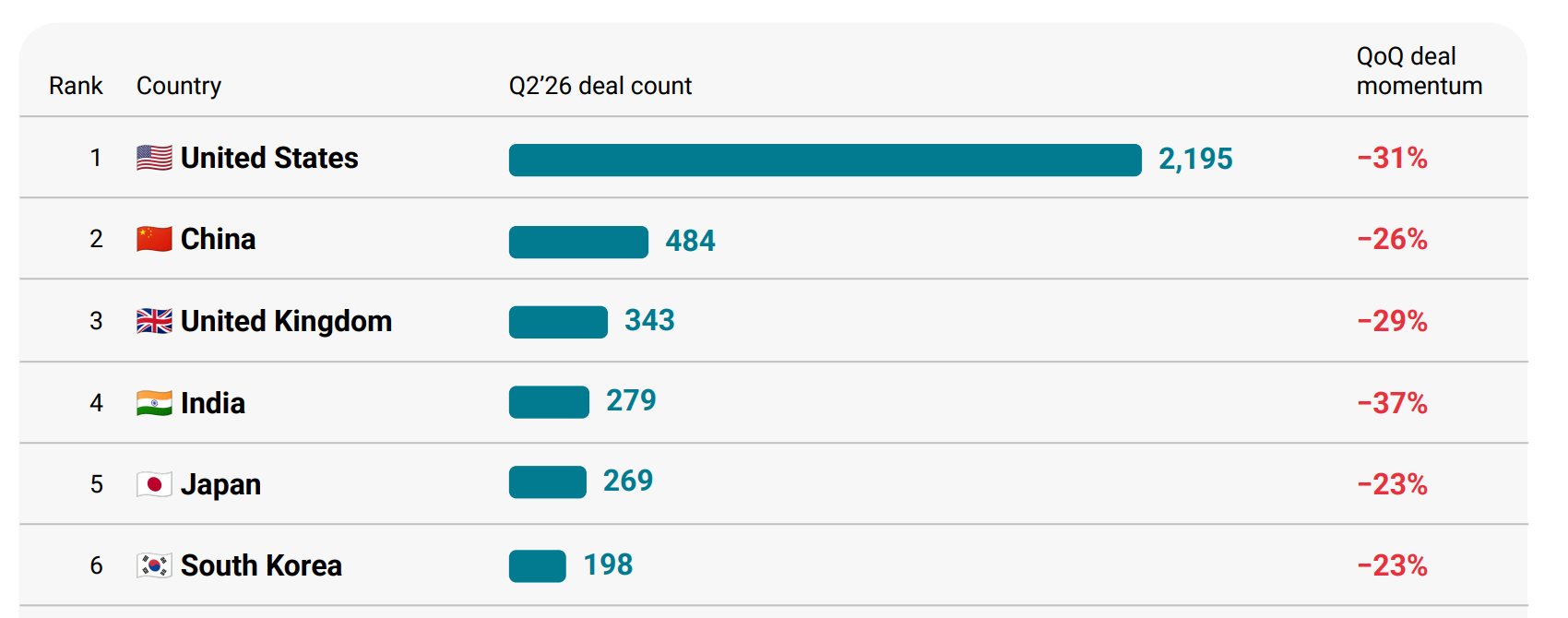

Here’s a strange thing to sit with: investors deployed $212.9B into startups last quarter - the second-highest total in the history of venture capital - and if you asked most founders raising right now, they’d tell you the market feels dead.

Both things are true. And the gap between them is the most important story in venture this year.

Fewer companies got funded last quarter than at any point in the past decade. New unicorns collapsed from 83 to 26 - the lowest since Q4 2024. Exits fell for the second straight quarter.

Deal count dropped double digits in every major market on earth: US down 31%, India down 37%, Germany down 33%.

Record money. Shrinking market. The money isn’t spreading - it’s stacking.

That’s the picture from CB Insights’ State of Venture Q2’26 report, released this week, and the mechanics underneath are worth understanding precisely:

263 mega-rounds ($100M+) captured 81% of all funding. Anthropic alone accounted for more than a third of it - closing three separate rounds this quarter: $50B, $10B, and $5B

Add Project Prometheus ($12B) and DeepSeek ($7.5B), and five deals absorbed what used to be an entire quarter of global venture activity

Total deal count: 7,086 - a decade low

For two straight quarters, one or two companies have carried the headline number, which makes total funding a weak proxy for the actual market.

The unicorn stat is the one to sit with.

OpenAI and Anthropic pulled in nearly $187B combined in the first half of 2026 - capital that, in any prior cycle, would have been spread across hundreds of new billion-dollar companies. Instead, unicorn formation cratered to 26, and 17 of those were AI companies. If you’re building anything else, the path to a $1B mark has rarely been narrower.

One quiet bright spot: median deal size rose 5% to $4.2M. Fewer companies are getting funded, but the ones that do are getting slightly more. Investors haven’t left - they’ve consolidated conviction.

What this means if you’re raising:

Benchmark your raise against the deal-count line, not the funding line.

A decade low in deals means fewer term sheets in circulation than at any point since 2016 - plan for more parallel conversations and longer timelines, because “the market is hot” only describes a market you’re probably not in.

Watch where deal count is actually clustering. The most active categories this quarter weren’t LLMs - they were industrial humanoid robots (20 deals) and robot foundation models (15 deals). Physical AI is where net-new investor attention is forming, and deal count is a cleaner read on appetite than funding totals right now.

And know who’s still writing checks: a16z led the quarter with 47 deals, General Catalyst right behind at 46 - with Hillhouse and Accel newly entering the top five. In a market this concentrated, the active-investor list is more useful than any funding chart.

Why are U.S. companies quietly switching to Chinese AI models?

For the past two years, the AI race has largely been dominated by OpenAI, Anthropic and Google. But as businesses scale AI across their products, many are running into an unexpected problem: cost.

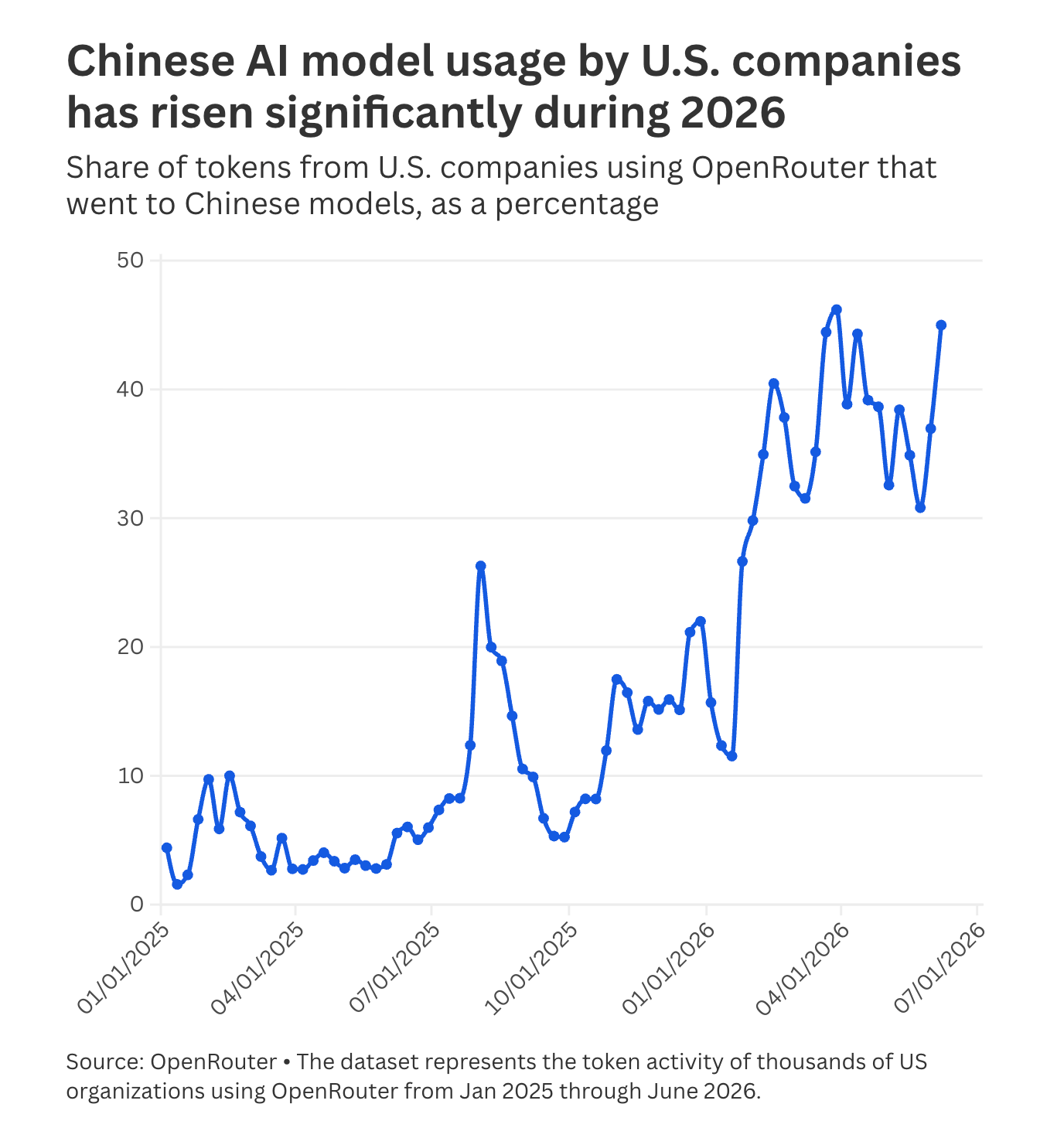

A new CNBC report, based on data from OpenRouter and conversations with AI companies, shows that U.S. businesses are increasingly turning to Chinese AI models because they offer similar performance at a much lower price.

Adoption has surged in 2026.

The share of tokens from U.S. companies routed to Chinese AI models through OpenRouter has climbed from an average of 11% over the previous year to more than 30% every week since February, peaking at 46%.

Models from companies like DeepSeek, Z.ai and Alibaba’s Qwen are gaining traction across enterprise AI workloads.

Price is becoming the deciding factor.

Chinese open-source and open-weight models are estimated to be 60-90% cheaper than leading proprietary models from OpenAI and Anthropic.

AI startup Lindy recently shifted all of its AI traffic from Claude to DeepSeek, expecting to save millions of dollars while also improving performance on several workloads.

The performance gap continues to narrow.

Analysts estimate that the latest Chinese models are now only six to nine months behind the best U.S. frontier models.

For many business tasks, that gap is small enough that companies increasingly choose the lower-cost alternative, especially for internal tools, AI agents and customer-facing applications.

As AI becomes part of everyday software, model selection is becoming an economic decision as much as a technical one. For founders building AI products, this creates an opportunity to lower infrastructure costs by intelligently routing workloads across multiple models instead of relying on a single provider.

Companies that optimise for both performance and cost are likely to gain a meaningful advantage as AI usage continues to scale.

FEATURED POSTS

📄 Must Read Post

The Hidden VC Scorecard That Decides Your Next Round.

Every fund sorts its portfolio into three buckets and five observable signals reveal which one you're in, months before you raise.

What should founders never automate with AI? The signal vs. repetition framework.

The framework for deciding what to automate, what to keep human, and why 95% of AI projects fail to deliver ROI.

SOMETHING MORE

🧩 Frameworks & insightful posts

The Task Economy: AI's next $1 trillion market (And most founders are missing it).

Whenever OpenAI, Anthropic, or Google talk about AI growth, they usually highlight one number: tokens (the small pieces of text AI reads and generates whenever you use ChatGPT, Claude, or Gemini).

The logic is simple. The more tokens AI processes, the more people are using AI and the more revenue AI companies generate.

That’s why investors closely track token growth as one of the biggest indicators of the industry’s expansion.

But Everett Randle (General Partner at Benchmark) argues the next trillion-dollar AI category won’t be tokens.

It’ll be tasks. The companies that own the best data for training AI may end up owning the biggest competitive advantage.

Tokens measure AI usage. Tasks improve AI.

Think of it this way.

Tokens tell us how much AI is being used.

Tasks determine how much AI gets better.

Early AI models improved by training on the public internet. That approach is now hitting limits.

The next generation of improvements will come from expert-generated tasks that teach models how real professionals work.

For example, if you want an AI to become a great lawyer, it’s not enough for it to read legal textbooks.

It needs thousands of real-world exercises:

Reviewing contracts.

Drafting legal arguments.

Working inside legal software.

Having experienced lawyers score and correct every response.

Every completed task becomes training data that improves future models.

Why task demand is exploding

The same forces that increased token usage are now increasing demand for tasks.

Every major AI breakthrough requires dramatically more high-quality training work.

Better reasoning models → more complex expert tasks.

AI agents → more real-world workflows to practice.

Industry-specific AI → legal, healthcare, finance, engineering, and scientific datasets.

Enterprise AI → companies creating proprietary data instead of relying on public models.

As AI becomes capable of handling longer and more sophisticated work, the amount and quality of training data required grows exponentially.

Data is becoming the real moat

For years, companies believed the model itself was the competitive advantage. That assumption is changing.

If every company can access frontier models, then the differentiator becomes the proprietary data used to improve them.

The businesses that build unique datasets, evaluation systems, and expert workflows will likely outperform competitors using the same foundation models.

The numbers are already moving fast

The market is growing much faster than most people realise. Some notable signals include:

OpenAI and Anthropic are reportedly increasing spending on expert-generated training data by roughly 10x year over year.

Many AI application companies expect $100M+ annual spending on data generation and evaluations.

Mercor, which connects experts to AI training work, reportedly doubled from $1B to $2B ARR in just four months.

Expert hours on Mercor’s platform have surged from just 2,000 hours in early 2024 to more than 2.5 million hours by mid-2026, showing how quickly demand for specialised human expertise is accelerating.

Why founders should pay attention

Most founders think about AI in terms of choosing the best model. The bigger opportunity may be asking a different question:

What unique data can only our company create?

Every customer interaction, workflow, approval process, expert review, and business decision can become proprietary training data that improves your AI faster than competitors relying on off-the-shelf models.

The next AI race may not be won by whoever has the smartest model.

It may be won by whoever owns the richest collection of expert tasks that continually make those models smarter.

How to build AI agents as a non-technical founder (Anthropic’s guide).

Most founders use AI every day, but they’re still using it like a search engine. They open ChatGPT or Claude, explain their business again, describe the task again, paste the same context again, and repeat the whole process the next day.

Recently, Anthropic shared a practical guide showing that the real opportunity isn’t just chatting with AI - it’s building simple AI agents that already understand your work, your business, and your goals.

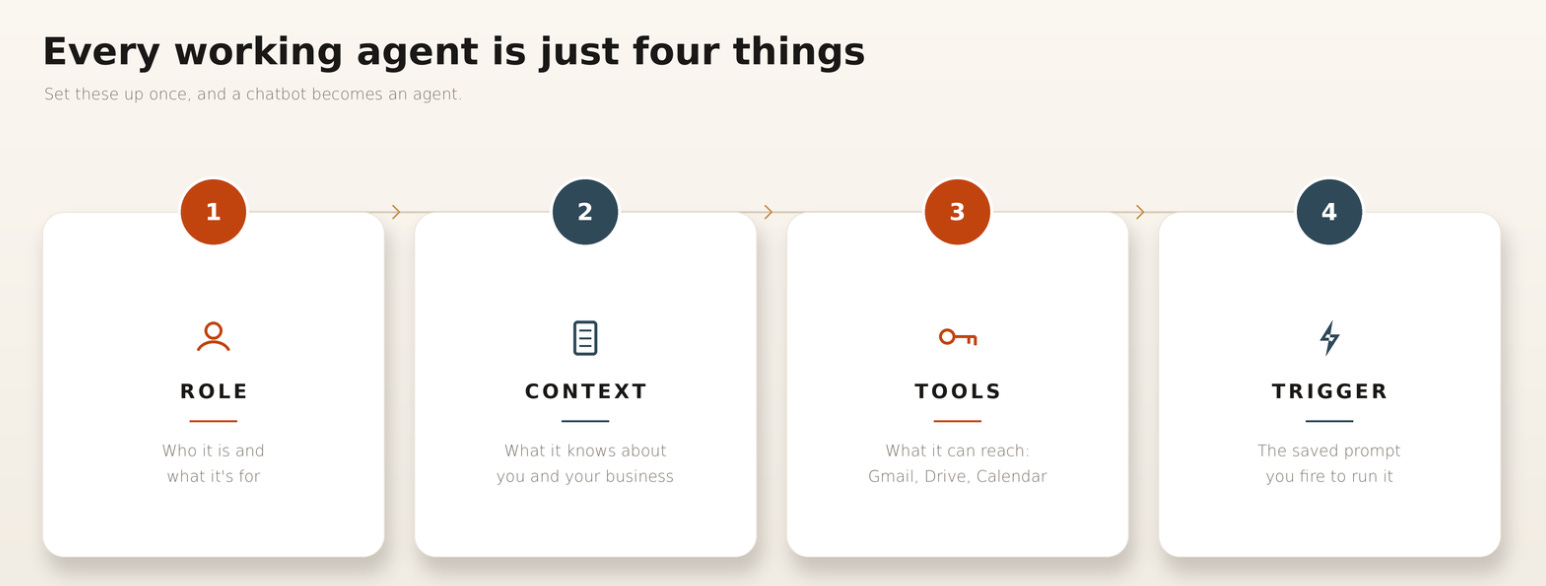

The biggest misconception is that AI agents require coding. They don’t. For most founders, an agent is simply an AI assistant you’ve configured once so it remembers your context and performs a specific job whenever you ask.

Instead of starting from scratch every conversation, you create a workspace with four simple ingredients:

Role: Tell the AI what job it has (executive assistant, sales researcher, customer support, etc.).

Context: Give it information about you, your business, customers, and how you like to work.

Tools: Connect services like Gmail, Google Drive, Calendar, or documents so it can access real information.

Trigger: Create repeatable instructions like “Prepare today’s meeting brief” or “Draft support replies.”

Once these are in place, the AI stops behaving like a chatbot and starts behaving like an assistant that already knows your business.

Some of the highest-impact agents founders can build include:

A personal assistant that summarises your inbox, prepares meeting briefs, drafts emails, and prioritises your day.

A sales research agent that studies prospects before meetings and prepares customised talking points.

A customer support assistant that drafts replies using your documentation while following company policies.

A content repurposing agent that converts one long article into LinkedIn posts, tweets, newsletters, or emails in your writing style.

One insight stood out: most people think the AI is the problem when the real problem is poor setup.

If an agent produces generic answers, it’s usually because it wasn’t given enough context, examples, or clear instructions. Small improvements to its instructions make every future response better, turning it into a system that improves over time instead of starting from zero every conversation.

The guide also recommends creating multiple specialised agents instead of one giant assistant. A dedicated sales agent, content agent, and operations agent are easier to improve because each has a single responsibility.

The takeaway is simple: you don’t need autonomous AI running your entire company to save meaningful time. Start by building one agent for the task you repeat most often - whether that’s email, meeting preparation, customer support, or content creation. Get that one working well before expanding.

Over time, you’ll build a small team of AI assistants that quietly handle repetitive work, giving you back hours every week while letting you focus on decisions only a founder can make.

📬 Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

NEWS RECAP

🗞️ This week in startups & VC

New In VC

Paradigm, a U.S.-based venture capital firm founded by Matt Huang and Fred Ehrsam, raised $1.2 billion for its latest fund. (Link)

Vermilion Cliffs Ventures, a U.S.-based venture firm founded by solo GP Ashley Smith, raised $25 million for its second fund. (Link)

Chemistry Ventures, a U.S.-based early-stage venture firm founded by Mark Goldberg, Ethan Kurzweil, and Kristina Shen, is raising $500 million for its second fund. (Link)

Omni Ventures, a San Jose, CA-based Manufacturing Tech VC firm, closed Fund I, at $33m. (Link)

B Capital, a global multi-stage investment firm, closed B Capital Ascent Fund III, L.P., at $500m. (Link)

Magnify Ventures, a Los Angeles, CA-based early-stage venture capital firm focused on transforming the care economy, announced the closing of Fund II, at $46.6m. (Link)

New Startup Deals

AIsa, a San Francisco, CA-based provider of a transaction network for the AI agent economy, raised an undisclosed Seed funding round. (Link)

Handspring Health, a NYC-based virtual mental health company, raised $19M in Seed funding. (Link)

Norm AI, a NYC-based company building agentic legal AI, raised $120M in funding at a $1.2B valuation. (Link)

Agave, a San Francisco, CA-based AI platform for construction financials, raised $15M in Series A funding. (Link)

Acti, a Singapore-based developer of an AI-native agentic smartphone keyboard platform, raised $5.3M in Seed funding. (Link)

geoSurge, a London, UK-based AI company helping brands inside generative AI systems, raised $12M in Seed funding. (Link)

TODAY’S JOB OPPORTUNITIES

💼 Venture capital & startup jobs

All-In-One VC Interview Preparation Guide: In partnership with a leading investor group, we have created an all-in-one guide for aspiring VCs. Don’t miss this. (Access Here)

Head of fund accounting - Stepstone Group | USA - Apply Here

Associate or Senior Associate - Bessemer Partner | USA - Apply Here

VC Fellow - V11 | Remote - Apply Here

Portfolio & Ecosystem Analyst Intern - Motion Venture | Singapore - Apply Here

Investor - Superseed | UK - Apply Here

Principal - ICMG Group | India - Apply Here

Ventures Analyst/ Associate - plug and Play tech center | USA - Apply Here

Associate - Primary VC | USA - Apply Here

Associate, Healthcare (SF based) - B Capital | USA - Apply Here

VP — Finance & Compliance - Transition VC | India - Apply Here

Senior Associate - ICONIQUE CAPITAL | USA - Apply Here

Ventures Associate - Plug and Play Tech Centre | USA - Apply Here

Investment Associate / Analyst - Flashpoint | UK - Apply Here

Hard Tech Investment Associate - Upfront Venture | USA - Apply Here

Associate - Engine Venture | USA - Apply Here

Senior Venture Studio Analyst - Atlantic Health System | USA - Apply Here

Talent Investor - Associate - Entrepreneur First | India - Apply Here

Partnership With Us

Get your product in front of over 125,000+ audience - Our newsletter is read by thousands of tech professionals, founders, investors and managers worldwide. Get in touch today.

Upgrade to Venture Curator Premium

Get access to 150+ premium archive posts, 100+ startup & VC resources, investor databases, fundraising templates, and exclusive startup research - all in one place.

(Subscribe to Venture Curator Premium and get 20% off forever.)